From contract research organisations (CROs) in life sciences to IT managed services firms and logistics providers, B2B outsourced service providers all face a similar challenge: they serve diverse customers with different needs and willingness to pay.

A biotech start-up seeking affordable preclinical testing has very different price expectations from a global pharmaceutical company outsourcing integrated discovery programs. Similarly, in IT managed services, a small regional business looking for basic support has very different requirements from a multinational outsourcing its global infrastructure.

This heterogeneity makes pricing one of the most critical, and most underutilised, levers in outsourced services.

Service providers also have to deal with volatile levels of utilisation and therefore bottlenecks across service lines or geographies, which directly and significantly impact their unit economics, their investment decisions and overall bottom line. Being able to charge a premium when capacity is scarce, or discount to increase utilisation, can materially benefit financial performance.

The prevalence of cost-plus pricing

Today, most outsourced service providers rely on cost-plus pricing, adding a standard margin to the direct cost of service delivery. This approach is straightforward, transparent and often welcomed by procurement functions of customers, as it reduces disputes over fairness and ensures cost recovery.

From an operational standpoint, it provides clarity to account teams, streamlines the quotation process and reduces internal debate. But cost-plus also leaves significant value on the table. It ignores differences in customer willingness to pay, fails to reflect the strategic value or level of differentiation of certain services, and does not typically reflect capacity utilisation considerations.

Adopting alternative approaches to improve yield

Several other pricing models are available. Value-based pricing seeks to set prices in line with the economic value delivered to customers and can significantly enhance revenue capture, especially when the service is clearly linked to outcomes or customer ROI. A more dynamic, capacity-based model can also drive utilisation by flexing prices depending on demand levels and resource availability.

At the same time, competitive pricing realities cannot be ignored. In many outsourced industries, services are only partially differentiated and customers view alternatives as interchangeable. Competitor price corridors often limit pricing freedom, unless the provider has distinctive technology, proprietary data or a brand that customers are willing to pay a premium for.

Principles for a modern pricing framework for outsourced services

To move beyond cost-plus, providers should embed clear principles into a modern pricing framework that can be applied consistently across service lines and customer types. These principles should underpin how price levels are defined, how discounts are managed and how guardrails are enforced:

- Anchor prices on customer value

Pricing must reflect customer willingness to pay, and the strategic importance and value of a project, recognising that different customers value the same service differently. - Reflect project delivery requirements

Complexity, delivery risk and resource intensity should shape price levels, ensuring effort and risk are adequately compensated. - Align pricing with capacity utilisation

When capacity is scarce, prices should maximise yield; when capacity is underutilised, winning new business becomes the priority. - Ensure customer alignment and defensibility

Pricing must be explainable in negotiations and defensible if challenged, balancing fairness with value capture. - Design for usability and adoption

A framework is only effective if commercial teams can apply it consistently; principles must translate into clear, practical tools and rules.

A well-designed pricing framework should create the foundation for profitable, yet fair and defensible, pricing that the sales team can effectively and consistently apply.

Adopting dynamic pricing in B2B outsourced services

Dynamic pricing has significant potential in outsourced services, but in a B2B context it must be carefully deployed to protect — and ideally strengthen — customer relationships. In certain markets (e.g. air travel, hotels or certain e-commerce platforms), customers are used to significant price volatility and will tolerate frequent and often inexplicable changes in prices.

B2B customers value predictability and trust. Dynamic pricing should not involve constant price fluctuations. Instead, it could be structured as discounts off a high initial price point (‘list price’), occasionally through the addition of straightforward, acceptable surcharges to reflect specific, transparent factors (e.g. project urgency).

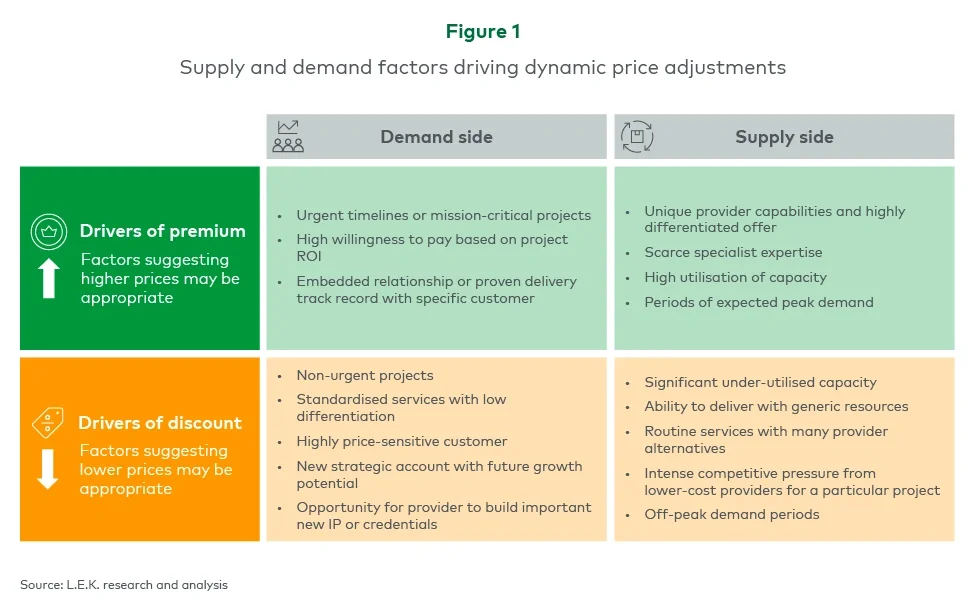

The exhibit below illustrates how supply and demand factors can be codified to guide structured, defensible dynamic pricing decisions (see Figure 1).