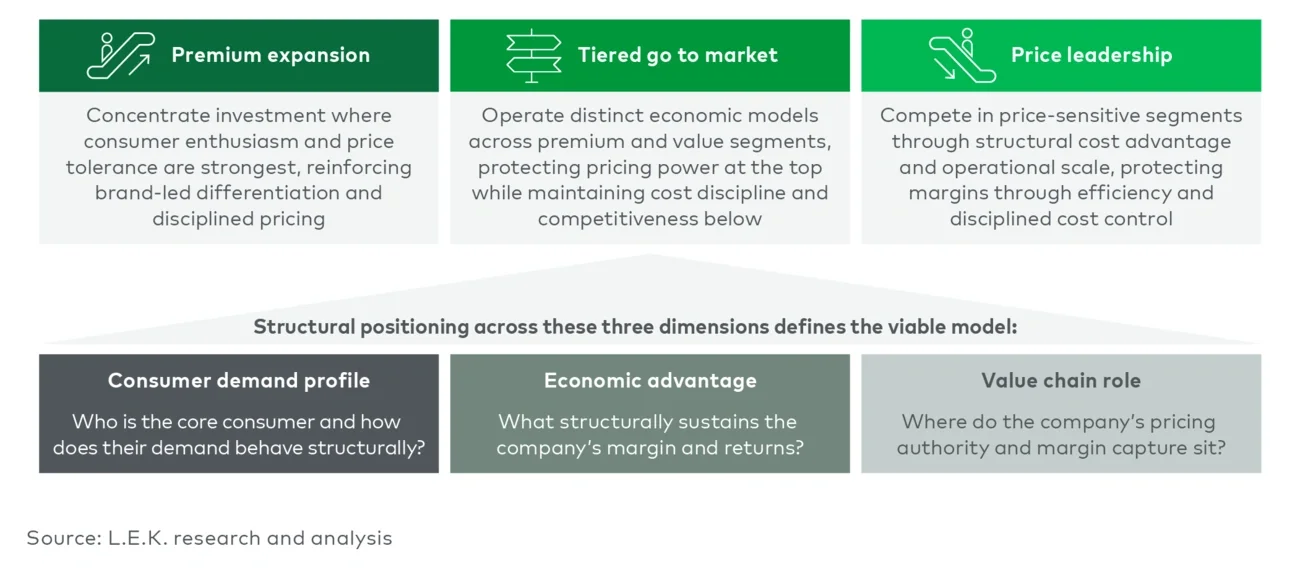

The first is premium concentration. Businesses anchored in higher-income, high-engagement segments can direct investment toward differentiation and brand reinforcement, protect pricing authority and prioritize the cohorts that drive disproportionate margin. Luxury brands, players differentiating via performance and experience-led categories often exemplify this model. Success depends on credible willingness to pay and effective pricing management.

The second is structural cost leadership. Where affordability and trade-offs dominate decision-making, advantage can come from scale, sourcing and operating efficiency. Off-price retailers, value grocers and scaled private-label players illustrate this path. Profitability relies on sustaining lower unit costs better than competitors do, not on stretching pricing power beyond what demand will support.

The third is disciplined tiered segmentation. Companies that operate across income cohorts must run premium and value propositions as distinct economic models, with clear price architecture and guardrails to prevent margin leakage. Global consumer brands with “good-better-best” portfolios or differentiated channel strategies often pursue this approach. The ability to segment without eroding overall returns becomes the central capability.

What becomes increasingly difficult to sustain is a broad middle-market position without a clear source of advantage. In a prior era, serving the average consumer was a viable strategy. Today, that same positioning risks being pulled in both directions — premium without sufficient willingness to pay or value without sufficient cost advantage.

This challenge is amplified by personalization. As consumers are increasingly targeted with tailored messaging, pricing and assortment, expectations rise for relevance at a more individual level. Companies attempting to serve multiple segments without clear separation often find their propositions blurred, making it harder to win decisively with any cohort.

In a K-shaped economy, strategic ambiguity carries a growing penalty.

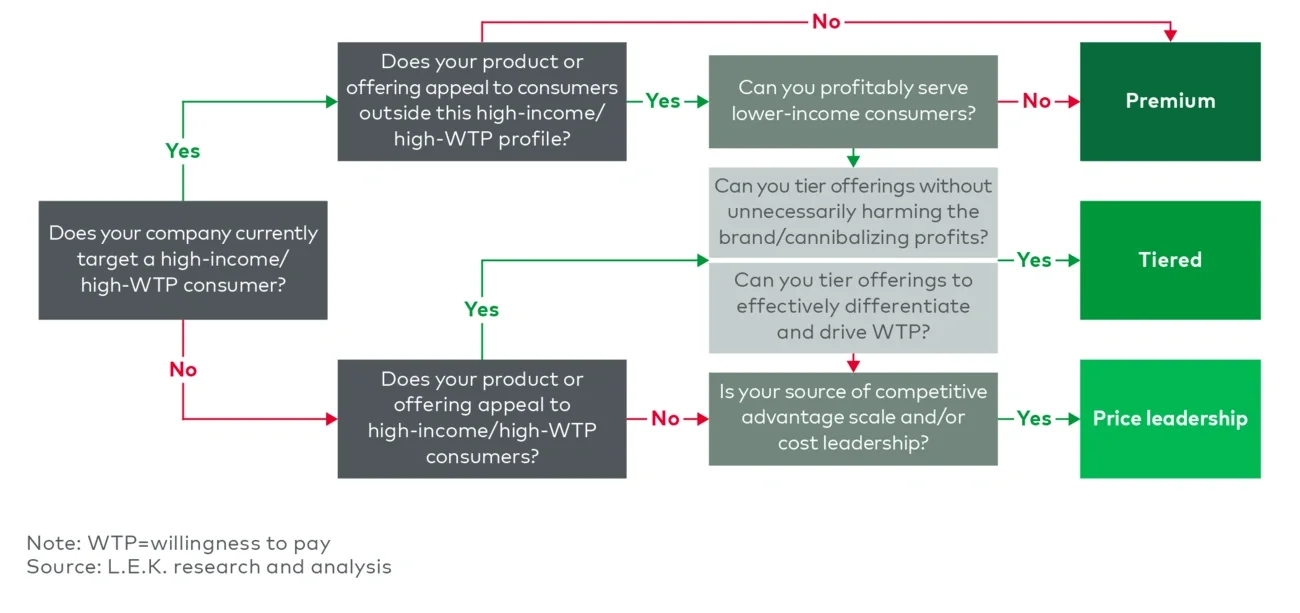

Determining the right strategic path

In a bifurcated economy, strategic direction should follow structural position. Whether tiered segmentation or price leadership is viable depends on three interrelated factors: the composition and behavior of the core consumer base, the source and durability of economic advantage, and where pricing authority and margin capture reside within the value chain (see Figure 5).

- Consumer demand profile: Start with the primary consumers by income cohort and category engagement. A business anchored in affluent, high-engagement consumers operates within a different economic envelope than one serving a broad, price-sensitive base.

What fundamentally drives purchase decisions matters just as much. Are purchases rooted in identity and brand differentiation or in functional need and affordability? How resilient is demand when prices rise or economic pressure intensifies? Trade-down patterns, switching behavior and mix shifts often reveal the true structural position of the model. Economic advantage: The next lens is the source of profitability. Are margins driven by pricing power or by structural cost advantage enabled by scale and efficiency? Durability is critical. Where does the company earn disproportionate profits across segments, stock-keeping units or channels, and how exposed are those pools to mix shifts or competitive pressure?

Premium expansion requires defensible willingness to pay. Price leadership requires enduring cost superiority. Tiered models require the ability to sustain distinct economics across segments without eroding overall returns.

Value chain role: Finally, the company’s position in the value chain shapes what is feasible. Does it control pricing and customer relationships, or is margin subject to retailer, platform or supplier pressure? Can it manage distinct tiers without leakage across channels or segments?

Taken together, these structural dimensions narrow the field of viable choices. In a persistent K-shaped economy, sustained performance depends on aligning strategy with how demand behaves, how margins are generated and where value is captured.