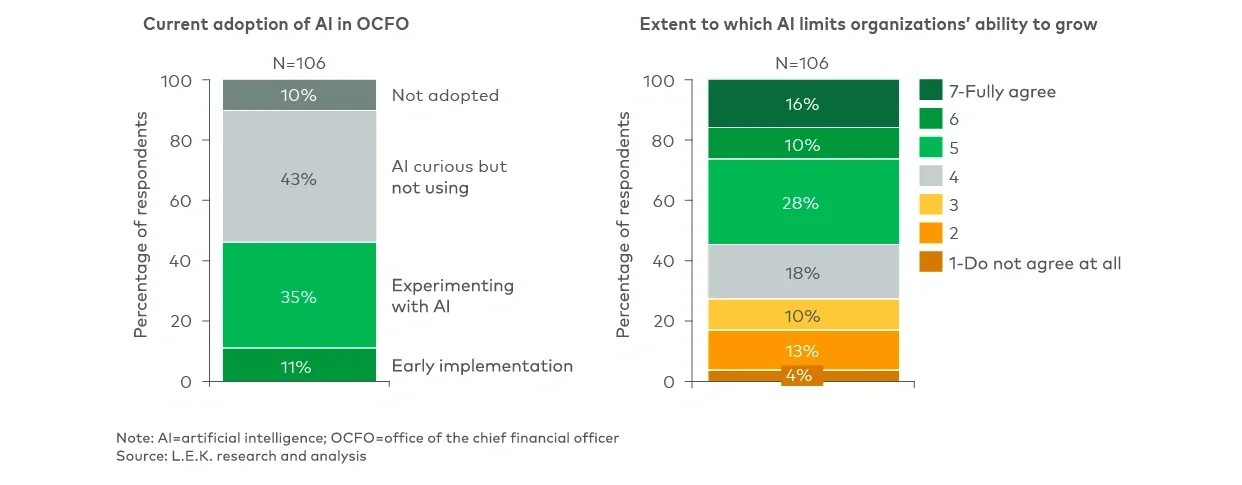

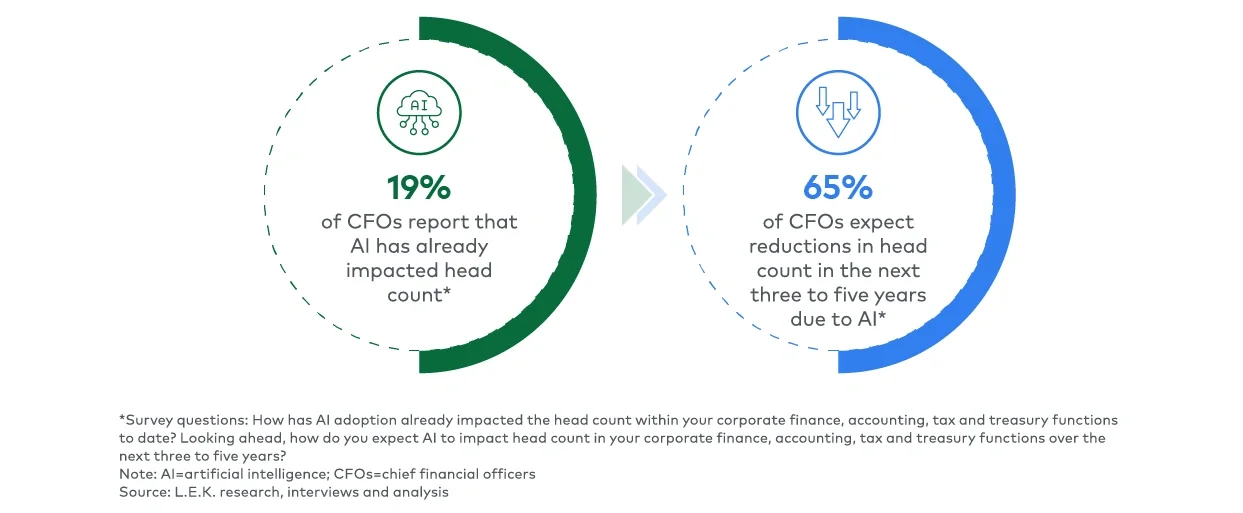

Transactional functions such as invoice processing, journal entry posting, reconciliations and other repeatable, rules-based tasks are seen as the most vulnerable. AI-powered tools are already proving capable of executing these activities faster, more accurately and at a lower cost than traditional human-led processes. As adoption scales, many CFOs anticipate downsizing or redeploying staff who are currently focused on these operational areas.

“... I think in three to five years, finance teams will be smaller and smarter. Repetitive work will be owned by AI, while people focus on complexity and strategy ...”

— CFO, multinational packaging manufacturer

At the same time, demand is expected to grow for more strategic, analytical and decision-support roles — in particular, talent that can help interpret AI outputs, apply financial judgment and collaborate cross-functionally with business partners in other departments and organizations. These roles will be less about processing information and more about extracting insights and shaping forward-looking decisions in line with the continued evolution of the OCFO to more strategic functions.

“... Anything that’s considered manual or time-consuming, where you’re having to input data in a traditional data entry format, AI is going to replace and speed up the process ...”

— CFO, real estate firm

For CFOs, this creates both an opportunity and a challenge: To redesign team structures, invest in new skills and ensure that technology and talent evolve in tandem to meet the needs of the modern finance function.

Embedded AI > stand-alone AI

The overwhelming majority of CFOs express a strong preference for AI capabilities that are embedded within broader finance or ERP platforms rather than delivered as stand-alone tools. This preference is rooted in practical realities that finance leaders face today:

- Ease of adoption: Embedded AI features typically require less effort to implement, configure and integrate with existing workflows. Because they’re native to systems already in use, embedded capabilities deliver faster time to value with fewer IT dependencies. For many CFOs, this approach feels less like adopting a new tool and more like a version upgrade of systems they’ve already invested significant time and effort into building. It preserves familiar workflows and interfaces, which is especially important for a group that tends to be risk-averse and highly attuned to operational disruption. In contrast, stand-alone AI tools often come with steep onboarding curves, data integration challenges and greater change management overhead, making them often feel like a wholesale restart rather than an evolution.

- Data consistency and integrity: Platforms with integrated AI features provide a single source of truth across functions, enabling AI to operate on consistent, up-to-date data. This is critical for CFOs aiming to maintain accuracy and trust in their reporting, forecasting and analysis. Siloed tools can create gaps, redundancies or inconsistencies that undermine the reliability and trust in AI-driven insights.

- Vendor rationalization: Most CFOs are actively looking to reduce, not expand, the number of vendors they manage. Platform consolidation helps simplify vendor relationships, reduce licensing complexity and improve accountability for performance and support.

This strong preference for embedded AI reflects a broader trend toward platform consolidation across the OCFO. In fact, roughly 56% of survey respondents report that they prefer platform solutions, while over ~31% prefer best-in-class point solutions (about 13% were neutral).

“... We’re already seeing convergence in tools offered; some vendors are adding capabilities to become more of a platform because they know CFOs want fewer systems and tighter integrations ...”

— CFO, energy software and analytics company

Strategic implications for solutions providers and investors

The implications are clear: While AI adoption is still in its early stages in the OCFO, demand is growing and expectations are rising. For vendors and investors alike, this means:

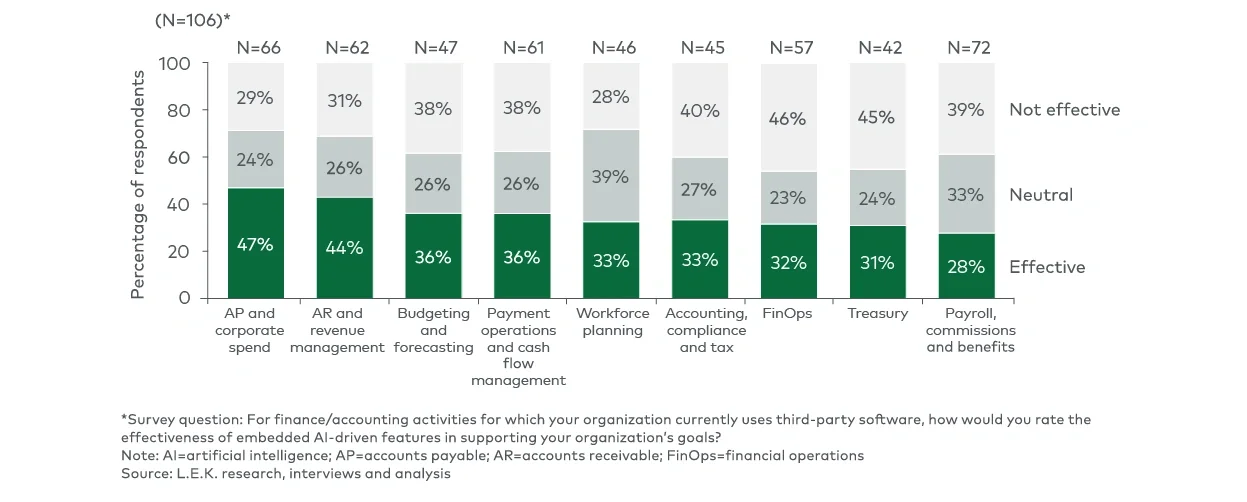

- Focusing on real use cases, not futuristic promises: CFOs need solutions that drive ROI today, particularly for AR/AP, budgeting and forecasting, and cash flow management.

- Prioritizing embedded AI within platforms: Tools that require separate implementation or learning curves will face resistance. Winning solutions will “just work” inside the stack.

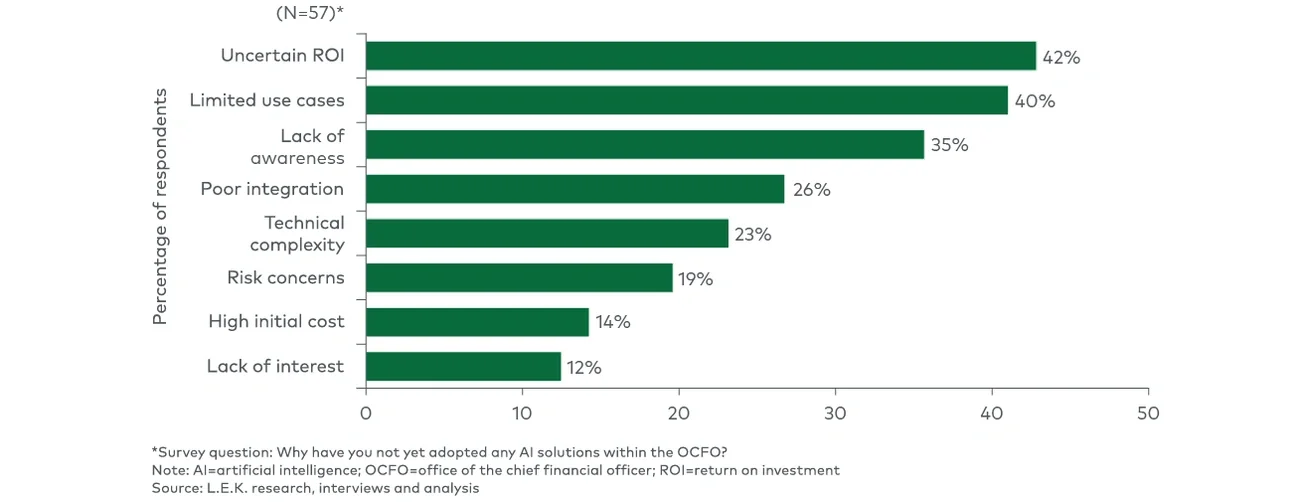

- Supporting education and changing management: Vendors must take the lead in demystifying AI, show real benchmarks and ease finance teams into adoption.

- Being ready to scale: The next wave of AI adoption will likely happen fast, especially once leaders start seeing results from peers.

Strategic implications for CFOs

For CFOs, the question is no longer whether AI will reshape the function — it’s how quickly and where to start. Across early adopters, one clear theme is emerging: The path forward is grounded in practical, operational wins, not sweeping transformation. AP and AR are proving to be fertile ground for early experimentation and are areas where CFOs can quickly realize time savings, improve accuracy and reallocate capacity to higher-value tasks.

CFOs who lean in will need to play the roles of both architects and change agents. Architects, in the sense that AI adoption, whether embedded in ERP systems or enabled through third-party applications, will require thoughtful coordination across finance, IT and the broader organization. And change agents, because success will depend not only on selecting the right tools but also on guiding teams through new workflows, building trust in AI-generated outputs and upskilling talent accordingly.

Most importantly, AI will reshape, not replace, the finance workforce. Transaction-heavy roles are already being automated, with many CFOs reporting a shift toward leaner teams supported by more strategic and analytically focused talent. While head count impacts are expected, the greater challenge may be enabling remaining team members to move up the value chain, from data processors to insight generators.

To prepare, leading CFOs are:

- Investing in finance-specific AI literacy

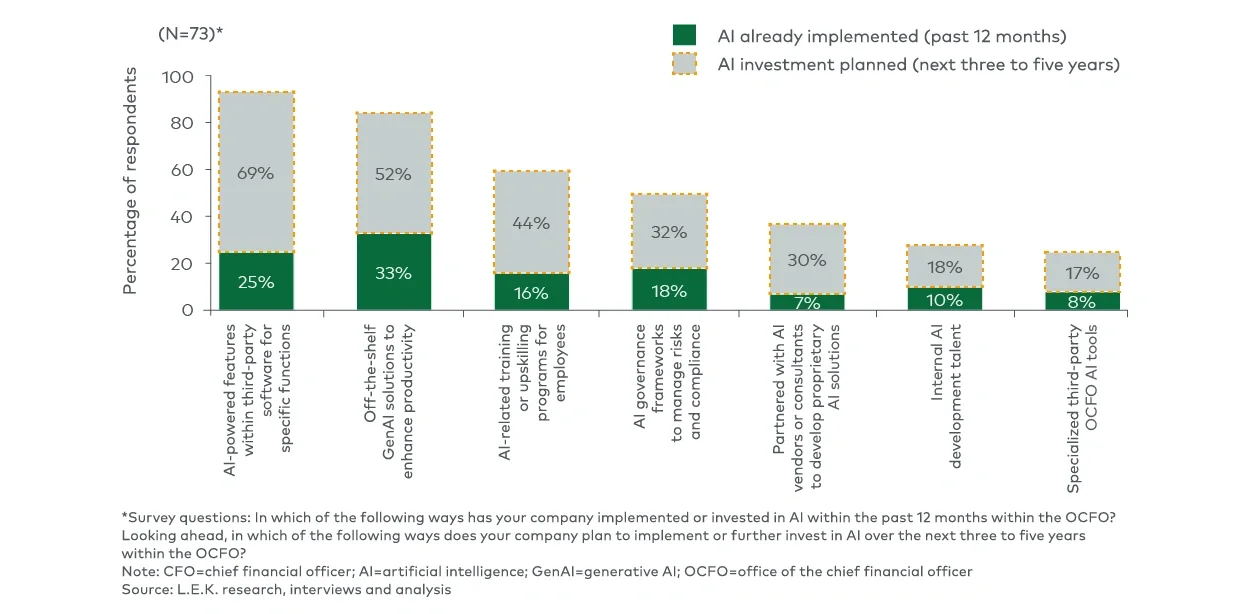

Equipping teams to evaluate and implement AI tools confidently, not just use them passively - Prioritizing embedded AI

Favoring tools already integrated into existing platforms, reducing the friction of adoption and maximizing data fidelity - Rewiring the operating model

Realigning finance organization structures, responsibilities and key performance indicators to reflect a world where AI augments human judgment

For most finance leaders, the real risk is no longer doing too much too soon; it’s standing still. As peer organizations scale successful AI pilots, expectations for productivity, decision-making speed and cost efficiency will shift quickly. CFOs must ensure their teams are not only ready to keep up but positioned to lead.

Conclusion: The AI future is coming, but it’s embedded and practical

AI is no longer a buzzword — it’s a buy signal. But for most CFOs, adoption will come through trusted platforms, practical workflows and measurable results, not just flashy pilots or disconnected tools.

Software providers, platforms, investors and CFOs who align with this pragmatic view by embedding intelligent capabilities into existing OCFO workflows are best positioned to lead this transformation.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consultin