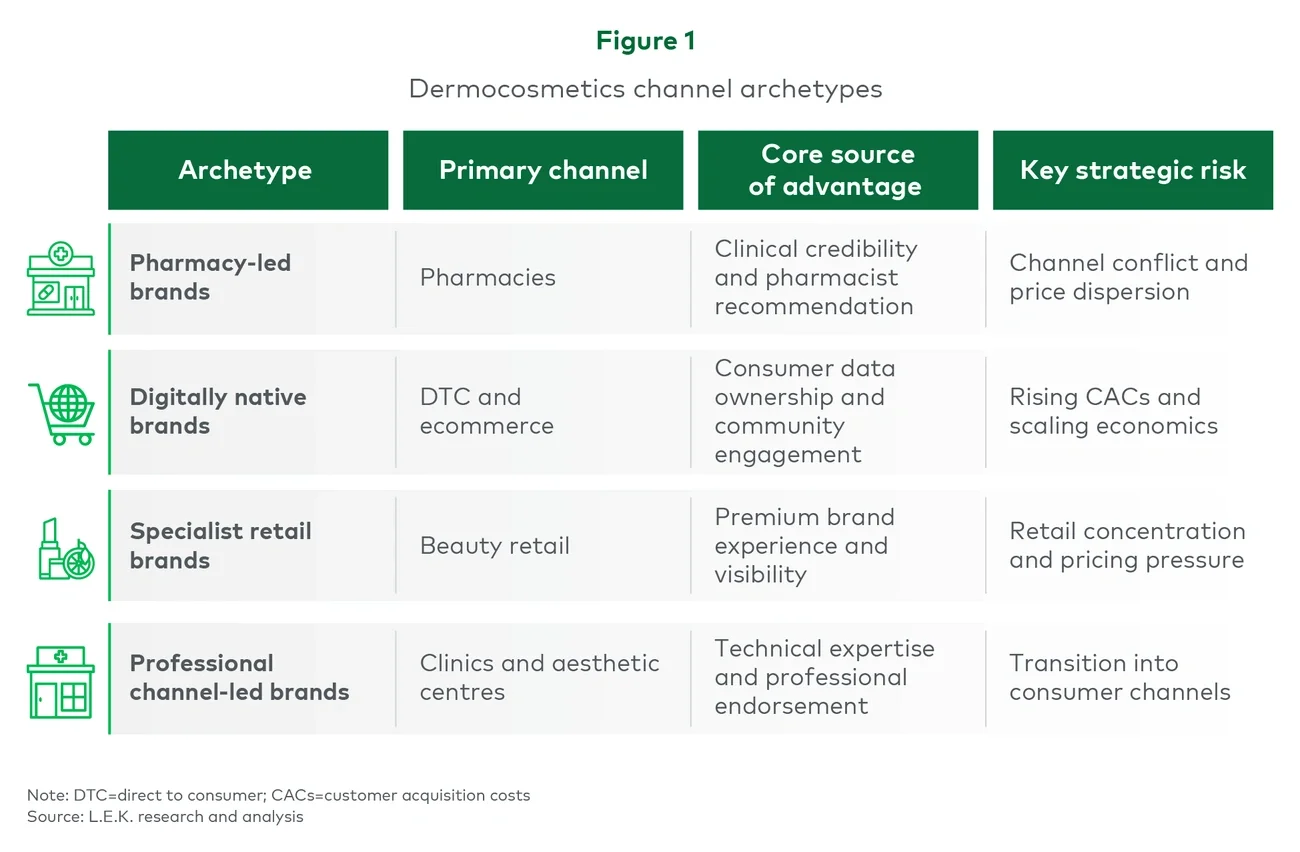

Pharmacy-led brands: Strong equity built on trust and execution

Brands such as ISDIN, Cantabria Labs and Sesderma have historically built their position through pharmacies, where recommendations and credibility remain critical drivers of purchases.

Their competitive advantage rests on clinical positioning, dermatologist endorsement and long-term pharmacist relationships supported through training, point-of-sale activation and product education. These factors create meaningful barriers to displacement when executed effectively.

ISDIN demonstrates the strength of this model through disciplined channel management, including differentiated product ranges, limited price dispersion across channels and pharmacy exclusivity periods for selected launches. Cantabria Labs has similarly maintained strong positioning through focused pharmacy execution and dermatologist endorsement.

The risks emerge when channel discipline weakens. Selling identical stock keeping units across pharmacies, retail, marketplaces and direct-to-consumer (DTC) channels without differentiation can create pricing pressure and undermine pharmacist confidence. Brands with significant price dispersion across channels often experience deterioration in recommendation dynamics that can take years to rebuild.

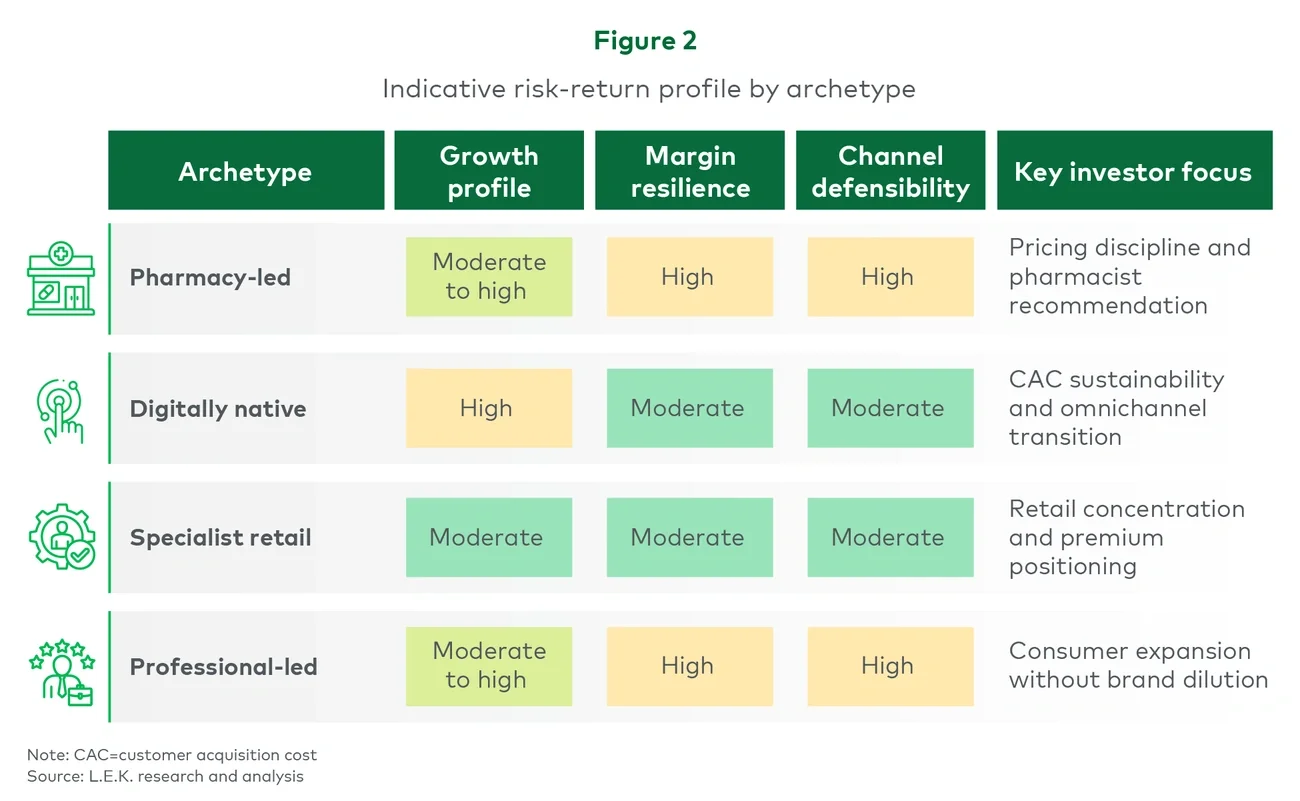

For investors, pharmacy-led brands with strong channel discipline continue to command premium valuations because their scientific authority can support expansion into adjacent channels and geographies. However, brands facing channel conflict and inconsistent commercial execution warrant greater caution.

Digitally native brands: High growth with scalability questions

Digitally native brands such as Freshly, The Niche Beauty Lab, Coconut and Lico built their initial consumer base through social media, DTC channels and digitally led engagement strategies.

Their proposition typically combines ingredient transparency, accessible pricing and strong community engagement. Operationally, these brands often benefit from a sophisticated understanding of customer behaviour, cohort economics and direct consumer engagement.

The investment appeal is clear: rapid growth, consumer data ownership and relatively asset-light infrastructure. However, international experience from the UK and US beauty markets has demonstrated that customer acquisition costs often rise materially as brands scale. Growth models driven initially by organic acquisition can become significantly more challenging once paid acquisition becomes the primary growth engine.

The key strategic question is whether digitally native Spanish brands can transition successfully into broader omnichannel distribution without diluting the positioning that supported early growth. Entering the wrong channel too early can alter consumer perception and compress pricing.

Investors therefore need to assess not only current growth rates but also the sustainability of customer acquisition economics and the credibility of the brand’s broader channel expansion strategy.

Specialist retail brands: Growing opportunity with active management requirements

Brands operating through specialist beauty retail channels such as Druni, Primor, Sephora and El Corte Inglés continue to benefit from increasing consumer interest in premium skincare.

However, the Spanish specialist retail market remains relatively concentrated, with negotiating leverage sitting among a limited number of major accounts. In addition, dermocosmetics penetration within specialist retail remains lower than in more developed European markets.

Despite these constraints, the channel continues to offer an attractive route for brands capable of maintaining a differentiated premium positioning. Several brands have navigated this successfully by preserving a clear consumer proposition while avoiding excessive distribution expansion.

Professional channel-led brands: Clinical authority with expansion potential

Brands such as Mesoestetic, HBA and Germaine de Capuccini originated within clinics and professional treatment environments, where technical expertise and practitioner endorsement underpin brand credibility.

These businesses are increasingly extending across the consumer journey through pre- and post-treatment product ranges, often supported by ecommerce platforms, owned clinics or expansion into adjacent retail channels.

The opportunity is significant, but execution remains critical. Consumer-facing formulations must preserve the efficacy narrative associated with the professional channel, while expansion into pharmacy or specialist retail requires commercial capabilities that many professional-channel businesses historically did not need to develop.

For investors, the central question is whether these brands can broaden their consumer presence without weakening the professional endorsement that originally differentiated them.

These structural differences translate into materially different growth, margin and defensibility profiles across archetypes (see Figure 2).