Each year, L.E.K. Consulting surveys hundreds of hospital and health system executives to capture their financial position and outlook, strategic priorities and near-to-mid-term actions.

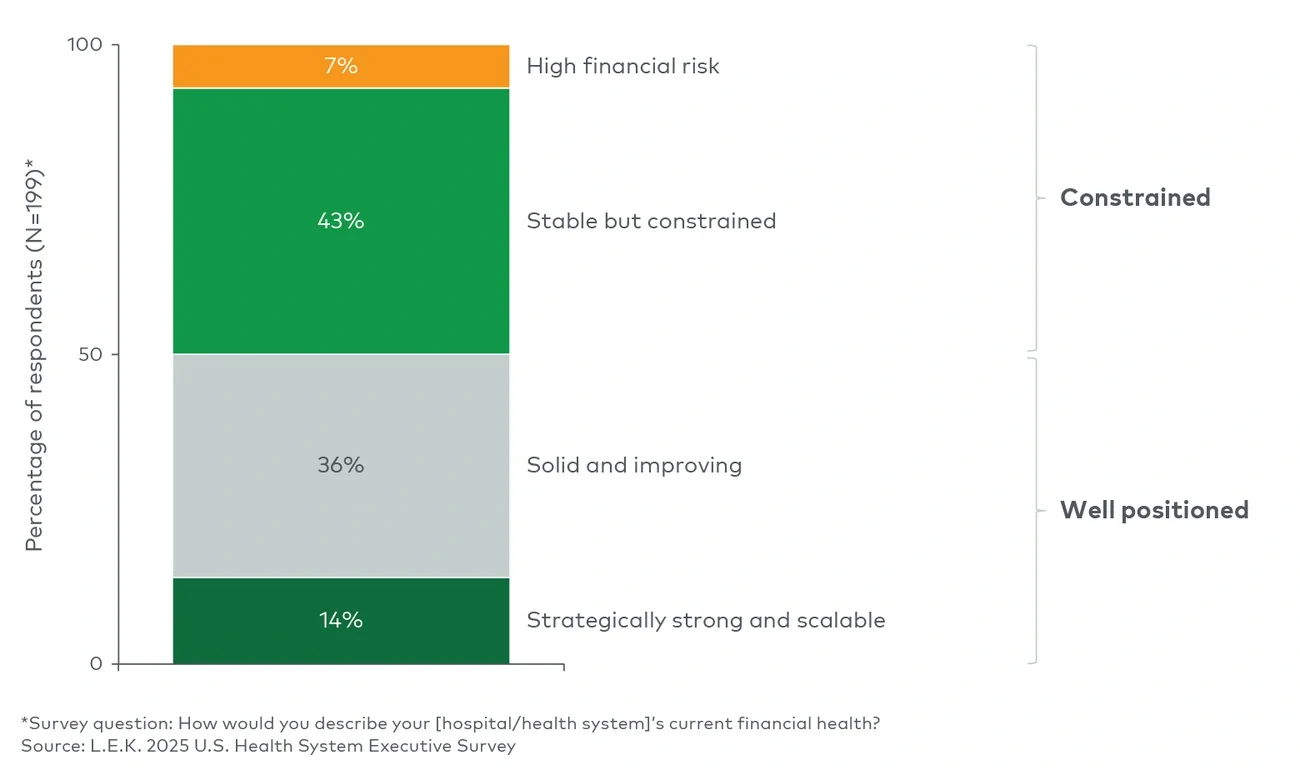

Our 2025 U.S. Health System Executive Survey comes at a time of rising costs, reimbursement headwinds and regulatory uncertainty. Many leaders report financial strain and are prioritizing near-term financial relief. Yet 50% describe their systems as financially strong and are investing in strategies to secure long-term viability.

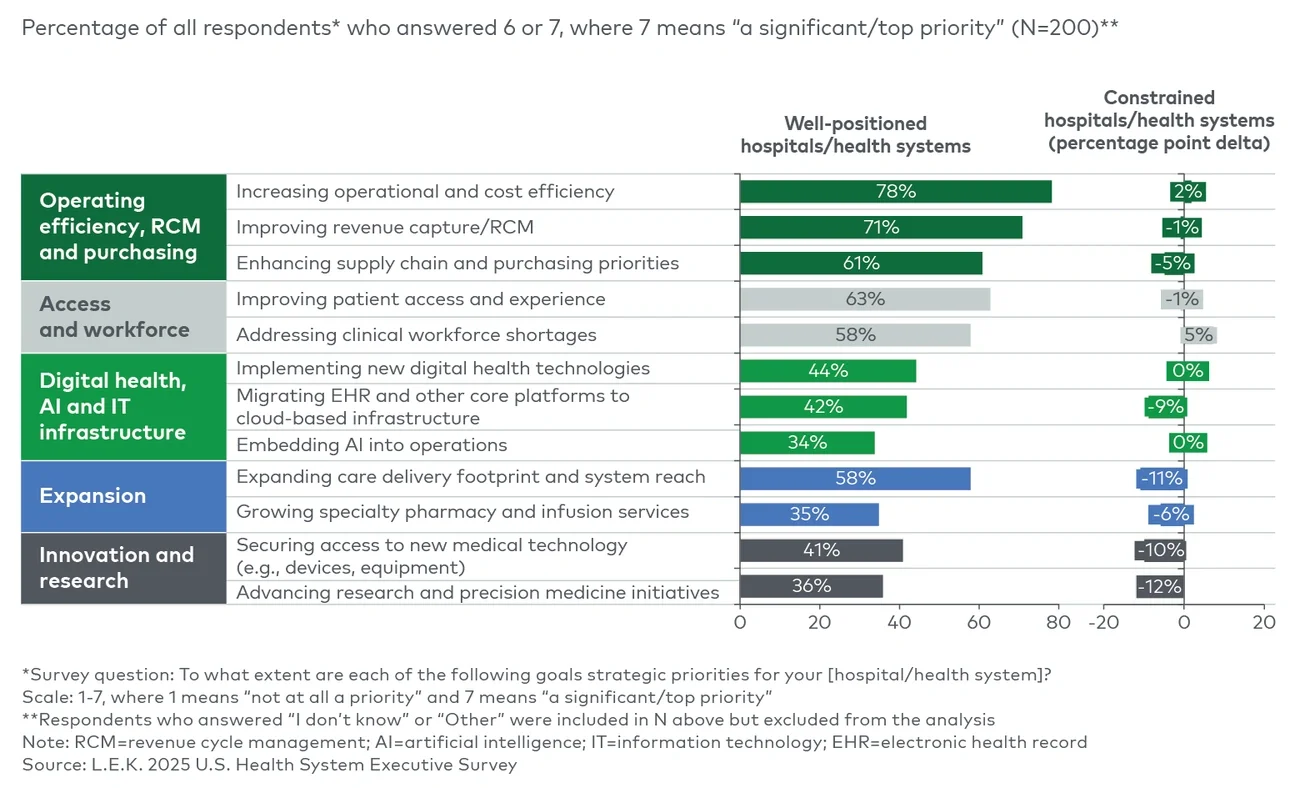

The divide between financially strong and financially constrained systems is widening. In this edition of Executive Insights, we explore the defining characteristics of these two cohorts and how their strategic priorities converge and diverge.

The financial divide

There is a clear divide in the financial health of U.S. hospitals and health systems. Approximately 50% of respondents reported that their organization’s financial position is solid or strong, and around 50% reported that their organization’s financial position is constrained or at high risk (see Figure 1).