Clinical next-generation sequencing (NGS) has been evolving from a specialized capability to a routine part of clinical decision-making. For NGS suppliers, capturing the next phase of growth will require understanding which lab segments are insourcing and why, what is driving instrument refresh and vendor selection and how sample-to-answer platforms fit into the near-term adoption curve.

L.E.K. Consulting’s U.S. Clinical Diagnostic Lab Survey captures perspectives from 100-plus executives and directors across hospital-based and multispecialty reference labs on near-term NGS testing demand and instrumentation purchasing expectations, to identify key market trends and spending opportunities.

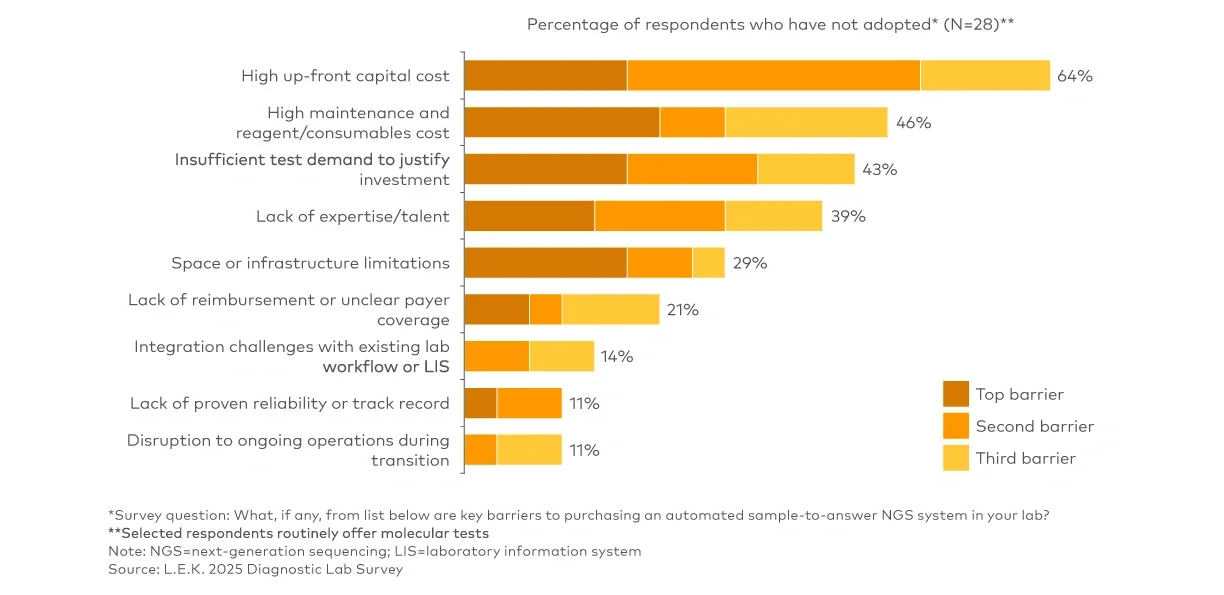

In this edition of Executive Insights, we share key trends in the U.S. clinical NGS market and implications for suppliers.

Key trends

Material growth expected for in-house NGS test volume, with significant new adoption among large community hospital labs

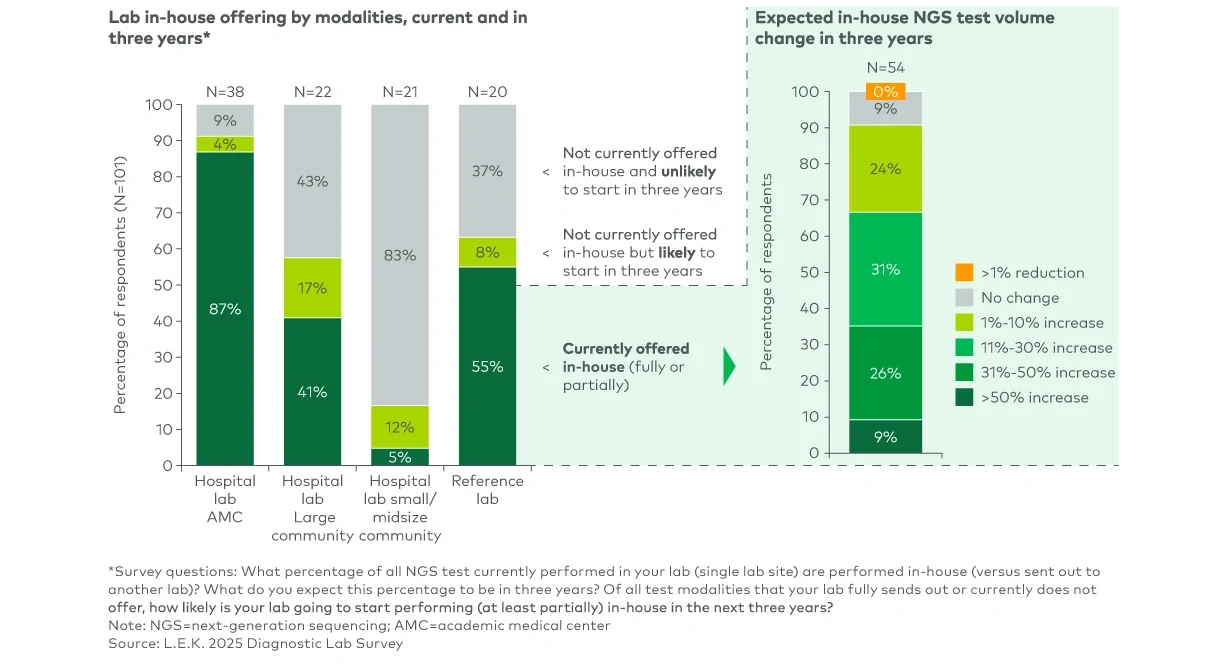

Approximately 90% of academic medical center (AMC) labs and 60% of reference labs surveyed run at least some clinical NGS testing in-house today (see Figure 1). Adoption is meaningfully lower in community hospitals, with around 40% of large community hospital labs and roughly 5% of small community hospital labs offering in-house NGS today.

Among labs that already run NGS in-house, material growth in test volumes is expected, driven primarily by expanding oncology testing and, to a lesser extent, hereditary genetics testing. Nearly two-thirds of labs currently performing NGS in-house anticipate double-digit growth in such testing over the next three years, including approximately 10% that are expecting volume to increase by more than 50% over the period. Additionally, labs with a mix of in-house and send-out volume expect the share of in-house tests to rise from an average of around 50% today to about 70% within three years.

Notably, NGS has the strongest overall growth outlook among all major testing modalities surveyed (see our previous Executive Insights on this topic for cross-modality comparison). This insourcing trend reflects growing confidence among labs that they can successfully operationalize NGS workflows in-house, versus a diminishing role for centralized testing. Specialty and reference labs offering laboratory developed test menus remain integral to the clinical NGS landscape, particularly for more complex assays (e.g., personalized minimal residual disease testing).