After a sustained period of declining consumption, wine brands are reassessing how to engage consumers and stabilize the category. Gen Z is central to that recovery, as the first fully digital-native cohort to enter legal drinking age with distinct expectations around wellness, authenticity and convenience. Importantly, older Gen Z cohorts experienced COVID-19-related disruption during their formative consumption years, while younger cohorts are entering under more normalized conditions.

With the number of Gen Z drinkers projected to grow around 80% over the next five years, brands must sharpen their strategies to attract and retain these consumers. Realizing this opportunity will require navigating a structurally challenging environment.

Structural headwinds are reshaping wine demand

Consumers are increasingly associating alcohol with health risks. A recent Gallup poll suggests that 53% of Americans believe one to two drinks per day is harmful to health, up from 39% in 2023. Broader wellness prioritization, including the growing use of GLP-1 medications, is adding further friction to routine consumption. Since 2019, legal-age drinking incidence has declined by approximately three percentage points, with consumers participating on fewer occasions and with greater intentionality.

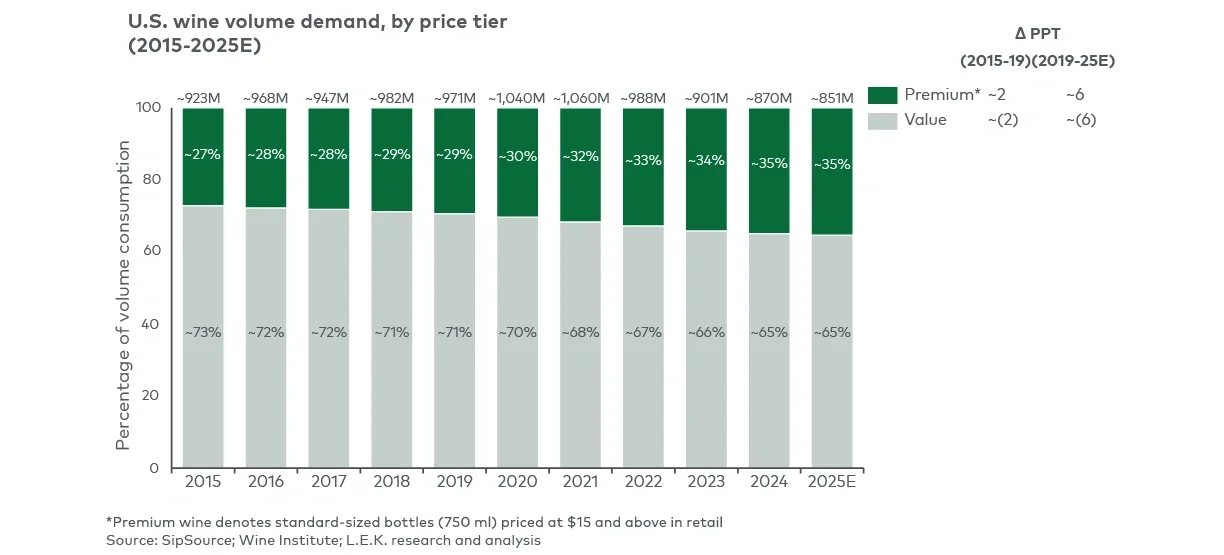

In parallel, wine is losing share of total alcohol consumed. Consumers are gravitating toward formats perceived as simpler and more convenient, including ready-to-drink cocktails, hard seltzers, ciders, hard teas, and low- or zero-ABV options. Spirit and cocktail alternatives are capturing demand through flavor innovation, single-serve convenience, accessible pricing and marketing that reinforces cultural relevance.

Against this backdrop, the wine industry must align with more intentional consumption patterns and must clearly differentiate from substitute categories in the years ahead. While these pressures are real, emerging data suggest the outlook is not uniformly negative.

Recent trends point to reasons for optimism

L.E.K. Consulting’s survey data indicate that Gen Z’s wine participation has increased meaningfully over the past two years, with 60% of legal-age Gen Z respondents reporting higher consumption. This challenges the narrative of permanent abstention among younger consumers. External surveys from IWSR and The Times suggest that monthlong abstinence behaviors such as Dry January may be losing momentum among younger drinkers, reinforcing the view that moderation trends may be stabilizing rather than accelerating. As Gen Z ages into the workforce, marriage and higher income, engagement is likely to move closer to that of older generations.

The divergence within Gen Z underscores the role of COVID-19 disruption during formative consumption years. Among legal-age consumers aged 21 to 24, 65% report higher wine consumption relative to three years ago, compared with 31% of those aged 25 to 29. Older members of the cohort experienced pandemic restrictions during their late teens and early 20s, a critical period for social habit formation and category experimentation.

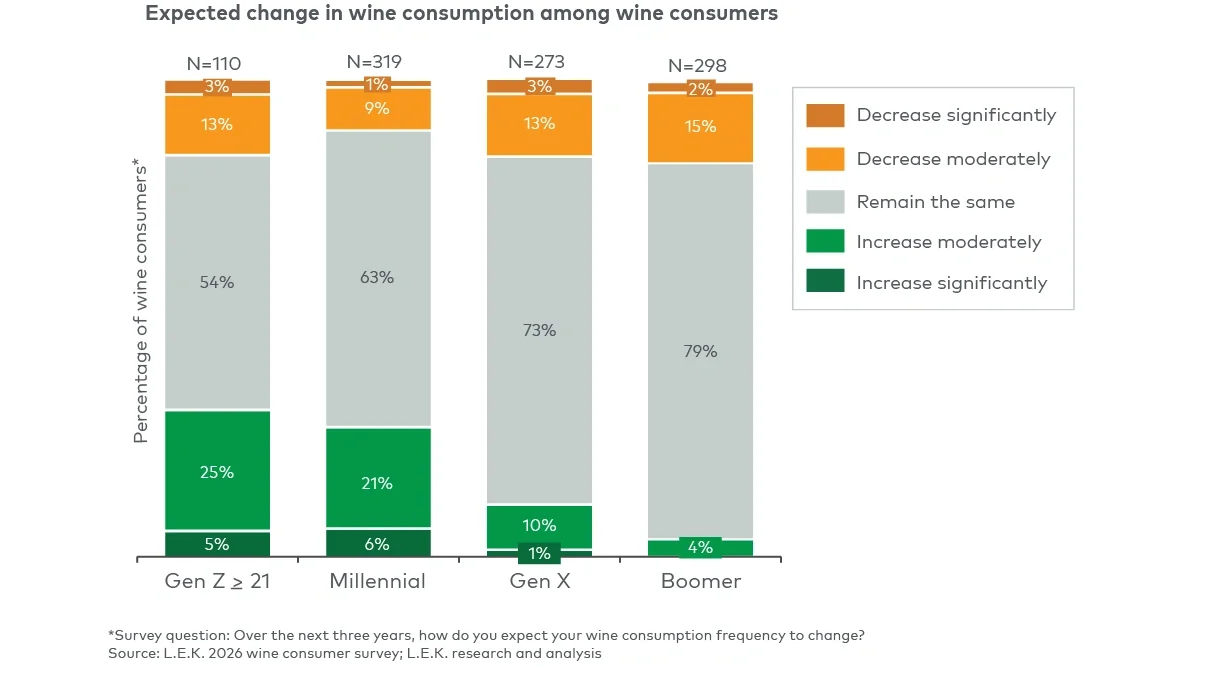

Younger Gen Z consumers, who entered legal drinking age under more normalized conditions, also express stronger forward intent, with a net 27% expecting to increase wine consumption over the next three years, versus 2% among those aged 25 to 29.

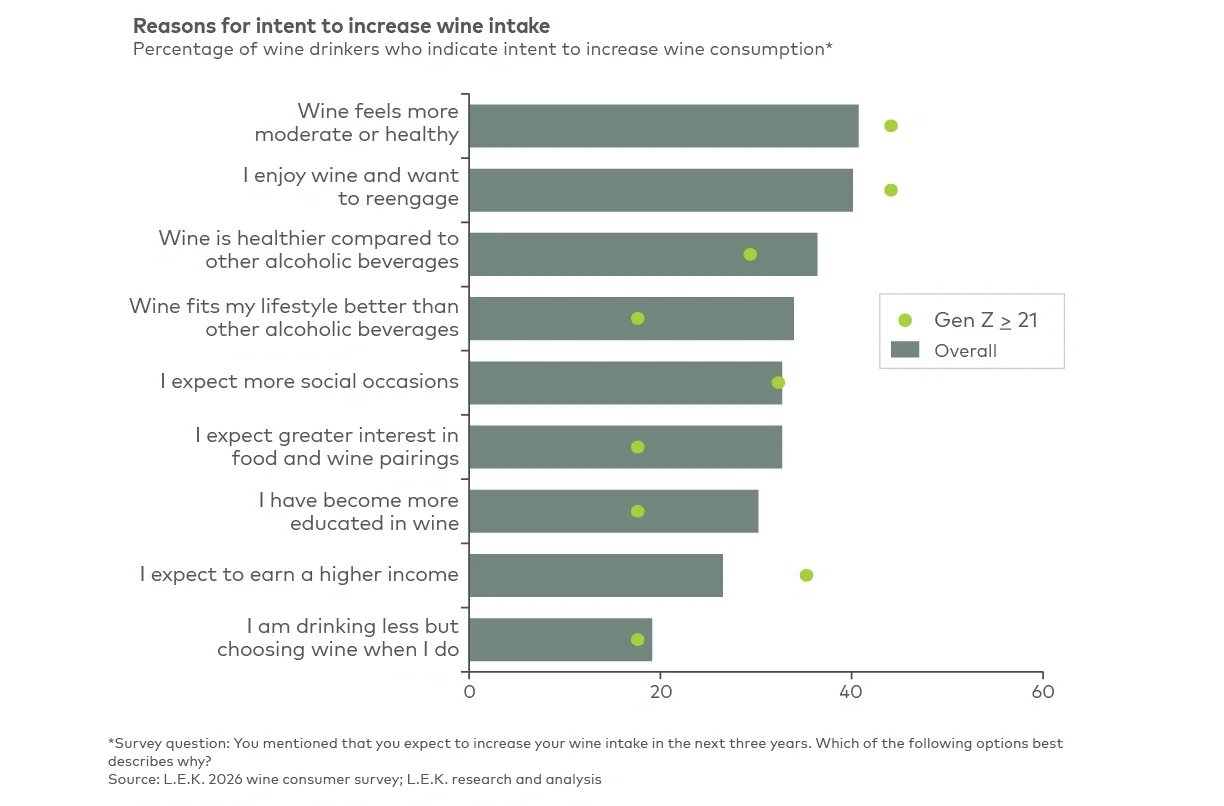

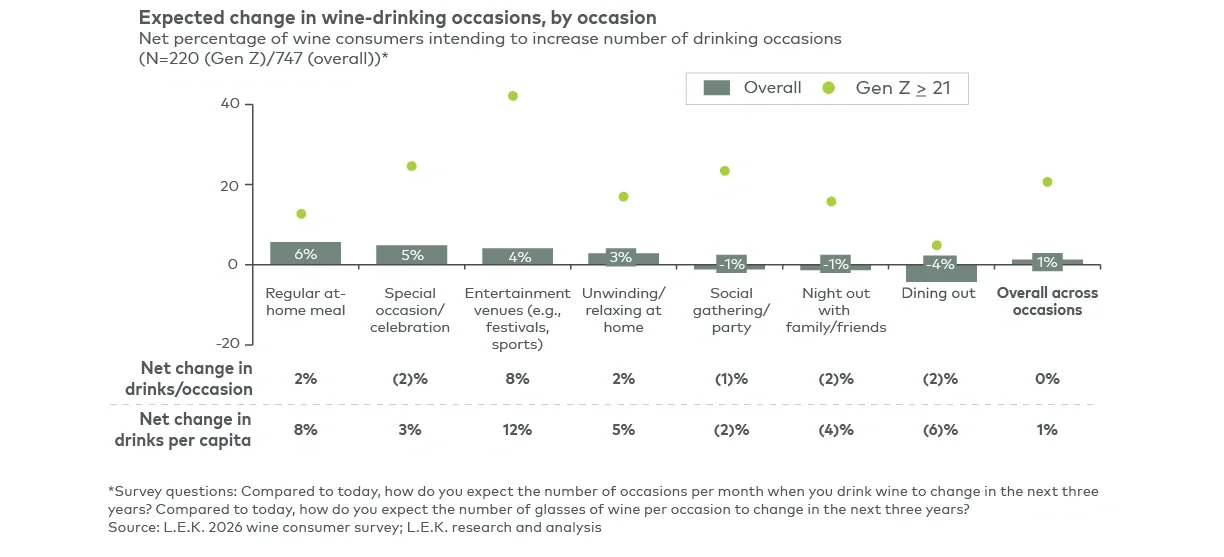

Looking ahead, approximately 30% of Gen Z wine drinkers expect to increase their consumption, citing primary drivers like wine’s perceived natural and healthier profile relative to other alcohol categories, overall enjoyment, and strong fit with social occasions (see Figure 1a).