Lastly, the insurer should consider sources of value, including strategic, product, sales and distribution, and capability areas. These can diverge and converge over time. Partnerships designed to prioritize one source of value may grow into others as organizations intertwine. This increases the need to be holistic, forward-looking and flexible when defining agreements.

Balancing benefits and risks

The benefits of strategic partnerships should align with company imperatives and aim to improve one or more of the following:

- Growth: How does the partnership help to address new customers and markets, improve the customer proposition or create value?

- Market positioning: Can the alliance help differentiate the insurer from competitors, improve brand reputation or create a competitive advantage? Can this advantage be sustained, or is it easily replicated?

- Customer experience and affinity: Can this partnership fill product and service gaps and elevate the customer experience? Remember, it’s not just about the insurer’s success but also about providing easily accessible, customer-centric solutions that anticipate and address their needs.

- Operational efficiency: Can the partnership quickly improve the insurer’s ability to make data-driven decisions, streamline internal processes and promote operational efficiency (e.g., underwriting and claims processing)?

Strategic partnerships can introduce risks that insurance companies must manage carefully. When priorities, timelines or strategies diverge, misaligned goals can derail success. What’s more, the growing need for data sharing requires a strong third-party risk management and compliance program to reduce operational and financial risks. Without stakeholder trust and transparency, partnerships will fail.

Culture and technological incompatibility can also derail partnership success. Insurers may be hesitant to partner or lack the digital maturity of potential partners (e.g., insurtechs and third-party administrators). To mitigate this, ongoing communication and shared understanding are key.

Monetizing partnerships will be challenging without carefully considering revenue models and timelines. Partnership plans need to balance different cost elements and revenue expectations. Unaddressed power imbalances between partners can quickly sour a partnership.

In the era of personalization, data sharing is critical. This can blur the lines of end customer ownership, particularly with distribution partners. Clear boundaries must be set to avoid conflict.

The partnership should also be scalable. A partner may be able to accommodate the transaction volume and customer types today, but can they enable future growth and innovation?

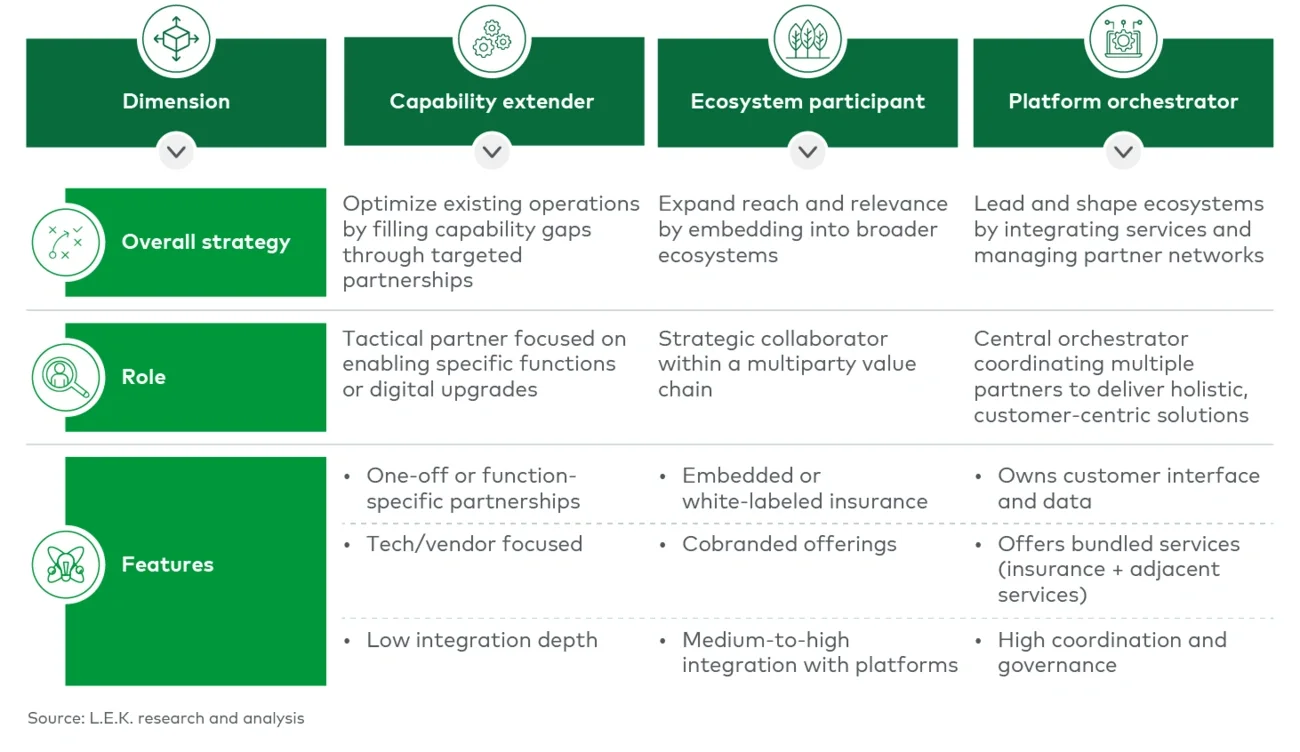

To thrive in today’s fast-evolving ecosystem, insurers must move beyond the traditional “build, buy, partner” to “partner, build, buy.” As stand-alone entities, they can no longer deliver innovative products and services fast enough.

Companies that fail to embrace partnerships will see competitors steal market share and customers and risk irrelevancy. Any partnership should deliver joint partner value and be customer focused.

When goals clash, partnerships crash: Lessons from failed insurance alliances

Strategic misalignment can undermine success. Below are two recent examples of insurance partnerships that failed for this reason:

- In 2016, AIG launched a joint venture with Hamilton Insurance and data science firm Two Sigma to modernize small commercial insurance. The goal was to simplify the broker experience through data-driven underwriting and a streamlined digital platform. However, the venture soon faced challenges: The complexity and variability of small commercial insurance across industries and states made automation and scale difficult. Strategic misalignment among partners, shifting priorities within AIG, and growing competition from insurtechs further hindered progress. Ultimately, the platform was acquired by cyber insurer Coalition in 2021.

- Google attempted to enter the U.S. auto insurance market through its Google Compare Platform. Though the program had earlier success in the U.K., efforts in the U.S. fell flat. The initiative struggled with limited carrier participation, regulatory complexity, channel conflict and low conversion rates. Most important, it underestimated the difficulty of commoditizing insurance in a trust-based, highly regulated environment. It’s a cautionary tale for tech companies aiming to disrupt the sector without deep industry integration.

The building blocks of partnership success

Partnerships take work. Some bring instant success while others fall short. Objectives, key results and key performance indicators are critical to fostering success. Defining them early ensures both sides have a clear roadmap to track progress and pivot when necessary. Open and frequent communication is critical, and a proper feedback loop enables the partnership to improve processes and optimize value.

Insurers should understand that not all partnerships are created equal and that short-term wins may not translate into long-term success. Consulting firms like L.E.K. bring a fresh, impartial view to partner evaluations and help design frameworks and governance models that amplify partnership impact. They know what works, what doesn’t and the red flags to watch for. Rather than chasing quick fixes, advisors help you build a strategy for enduring profitability and success.

Strategic partnerships are a significant weapon in the race to innovate and compete. It’s time for the insurance industry to evolve and innovate. Customers expect a great experience, and insurers must reengineer operating models and build alliances to meet the needs of today and beyond. This future state will allow insurers to increase efficiency and prevent revenue leakage by playing in their new ecosystem lane.

So, why L.E.K.?

At L.E.K., our Financial Services practice is built for the moments that define the future of your business, not just maintain the present. We work with leaders navigating disruption, transformation and growth — helping them move with clarity and conviction in high-stakes situations. Our teams are senior-leaded and deeply engaged, bringing a sharp understanding of both strategic and financial realities.

What sets us apart is how we show up: We don’t rely on frameworks. We co-create tailored strategies with our clients and bring a best-in-breed mindset to every engagement — drawing on external expertise when it’s in the client’s best interest.

Whether you’re rethinking a business model, targeting new markets or positioning for long-term value, we’re here to help you lead with focus, agility and impact.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC