Related insights

You might also be interested in these insights.

English

Industrial equipment and technology executives in the U.S. are facing a raft of challenges, from inflation and tariffs to supply chain disruption, demand planning and backlog concerns — all against a backdrop of broader economic uncertainty.

High inflation and ongoing tariff threats have led to increased material costs and pricing in industrial manufacturing. Supply shocks and the prioritization of onshoring combined with the potential of a pro-U.S. manufacturing policy have created a volatile supply-and-demand environment. Accurately forecasting demand levels to capacity has never been more important.

But as L.E.K. Consulting’s survey of executives at 200 U.S. blue chip manufacturing organizations found, their longer-term sentiment on achieving strategic goals remains quite optimistic.

Conducted in March 2025, the latest annual version of the survey was designed to uncover not just how these industry leaders — whose titles include chief commercial officer, head of strategic development, VP of integrated offerings and VP of strategic sales — are addressing the myriad challenges currently facing their organizations, but how, in the midst of those challenges, they are planning for the future.

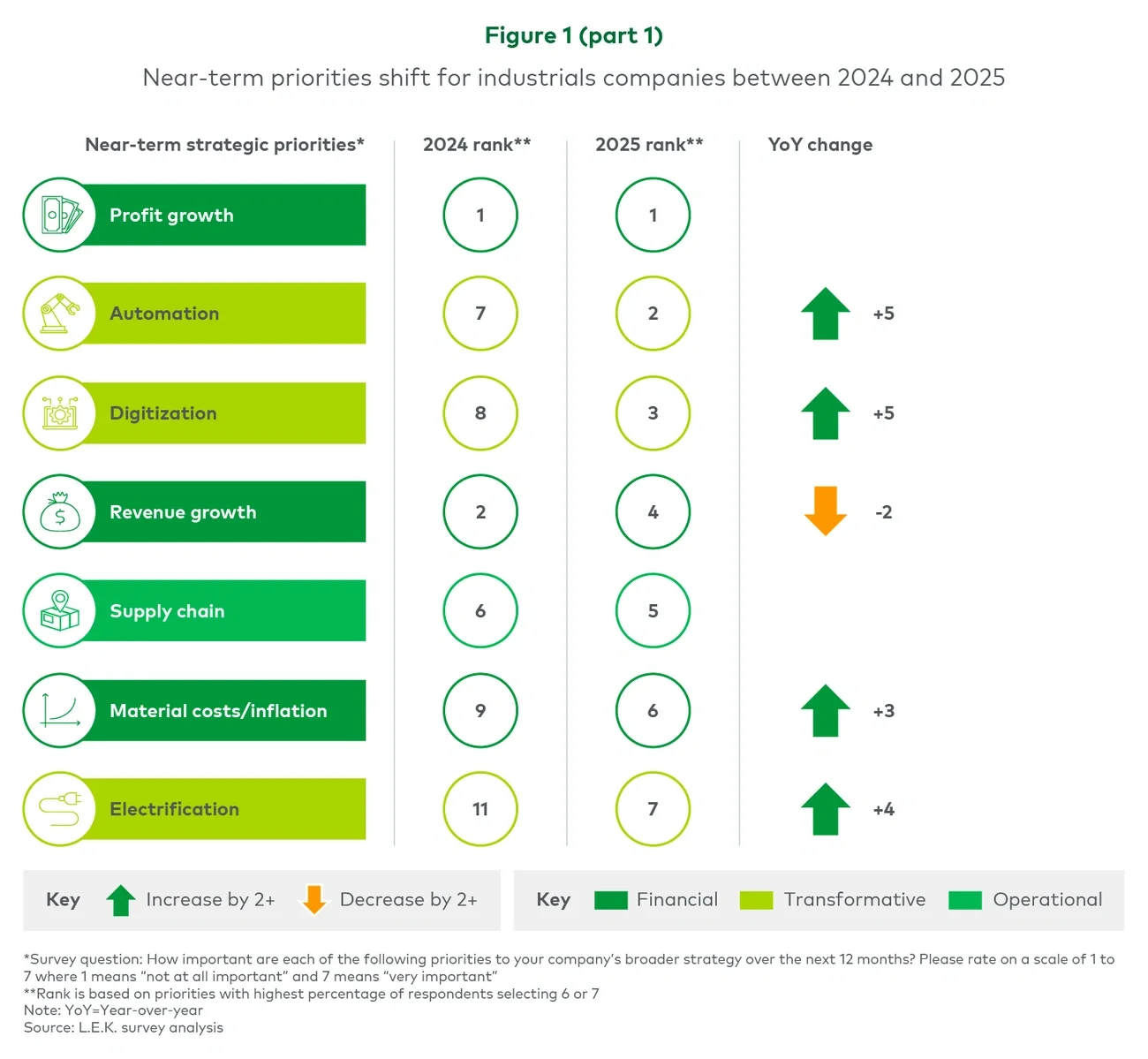

What we found was that while many of the executives’ priorities remain the same as in years past, the relative importance of those priorities has shifted along with their focus.

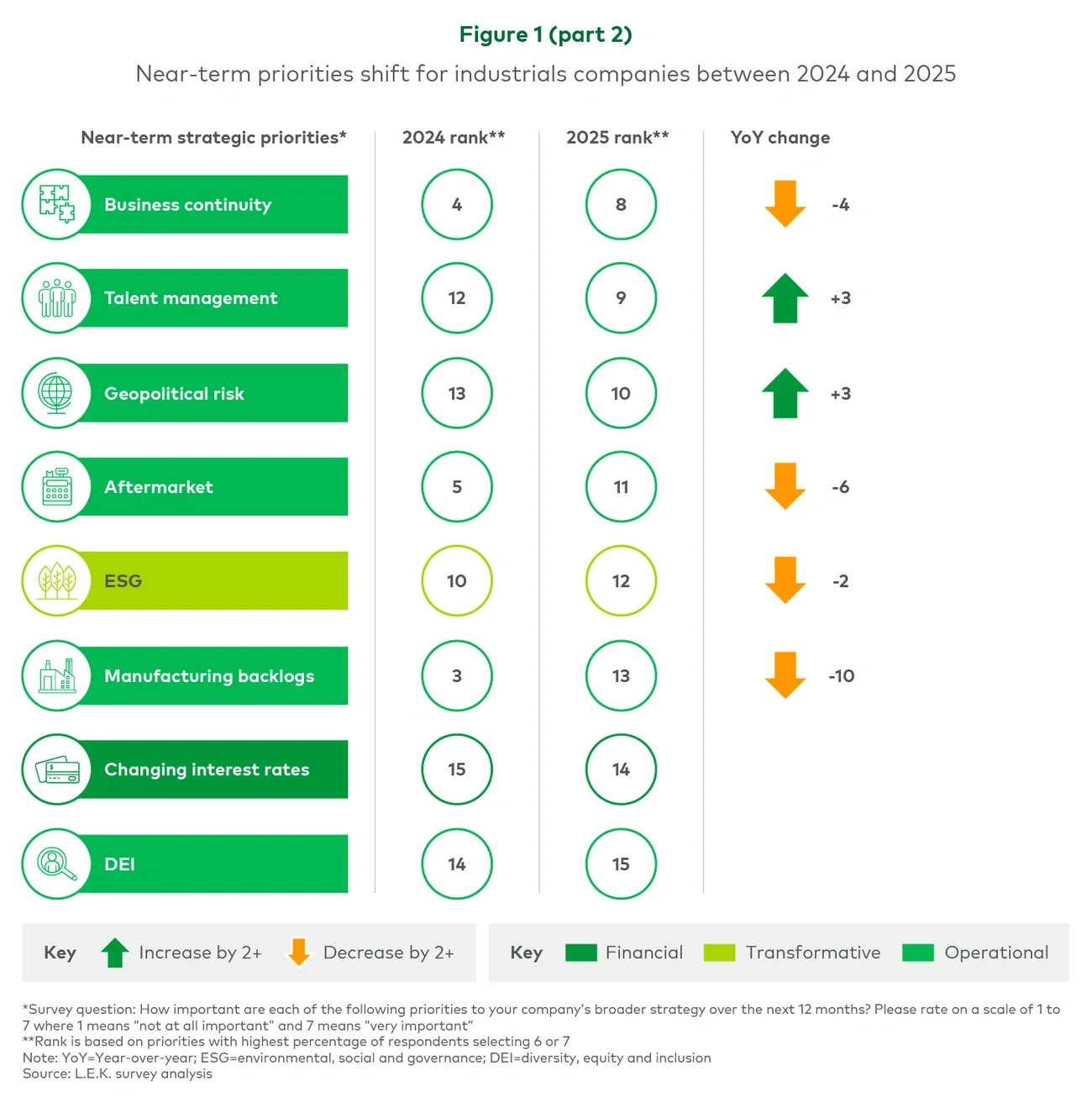

As these leading industrial technology manufacturer decision-makers make clear, profit and efficiency are, once again, their top priorities. Profit growth remains the top near-term priority, with margin-expanding initiatives such as automation and digitization making significant leaps in this year’s top-three list. Meanwhile, manufacturing backlogs, which were a top priority last year, have since largely moved out of focus (see Figure 1, parts 1 and 2).

To achieve their strategic goals, U.S. industrial firms are pursuing profit growth, automation and digitization and are doing so by prioritizing higher-margin products, aiming for eventual transformation to full automation and leveraging technology to improve their organizations’ operations, respectively.

When it comes to developing meaningful tariff/trade war plans, industrial executives are in “wait and see” mode. To be sure, mitigating negative impacts from tariffs and trade controls/sanctions are among their top concerns in the near term. But they’re holding off on putting in place more time-intensive/costly initiatives like relocating manufacturing and shifting supply chains until the longer-term outlook — and any related implications — becomes clearer and are implementing, no-regrets but albeit lower-impact actions instead.

Our survey respondents are most concerned about potential negative impacts from changes to tariffs and export controls, and among potential trade policy changes see tariffs as the most likely to be implemented. Indeed, in the weeks following the deployment of our survey, the Trump administration rolled out sweeping tariffs to many trade partner countries, justifying industrial companies’ concerns.

In the meantime, the most common actions being taken by manufacturing firms to prepare for tariffs are exploring new supplier relationships and reviewing price strategies.

Despite challenges in meeting immediate-term goals, industrial executives remain confident and optimistic in their ability to progress against goals in the medium and longer term and so are putting their focus there.

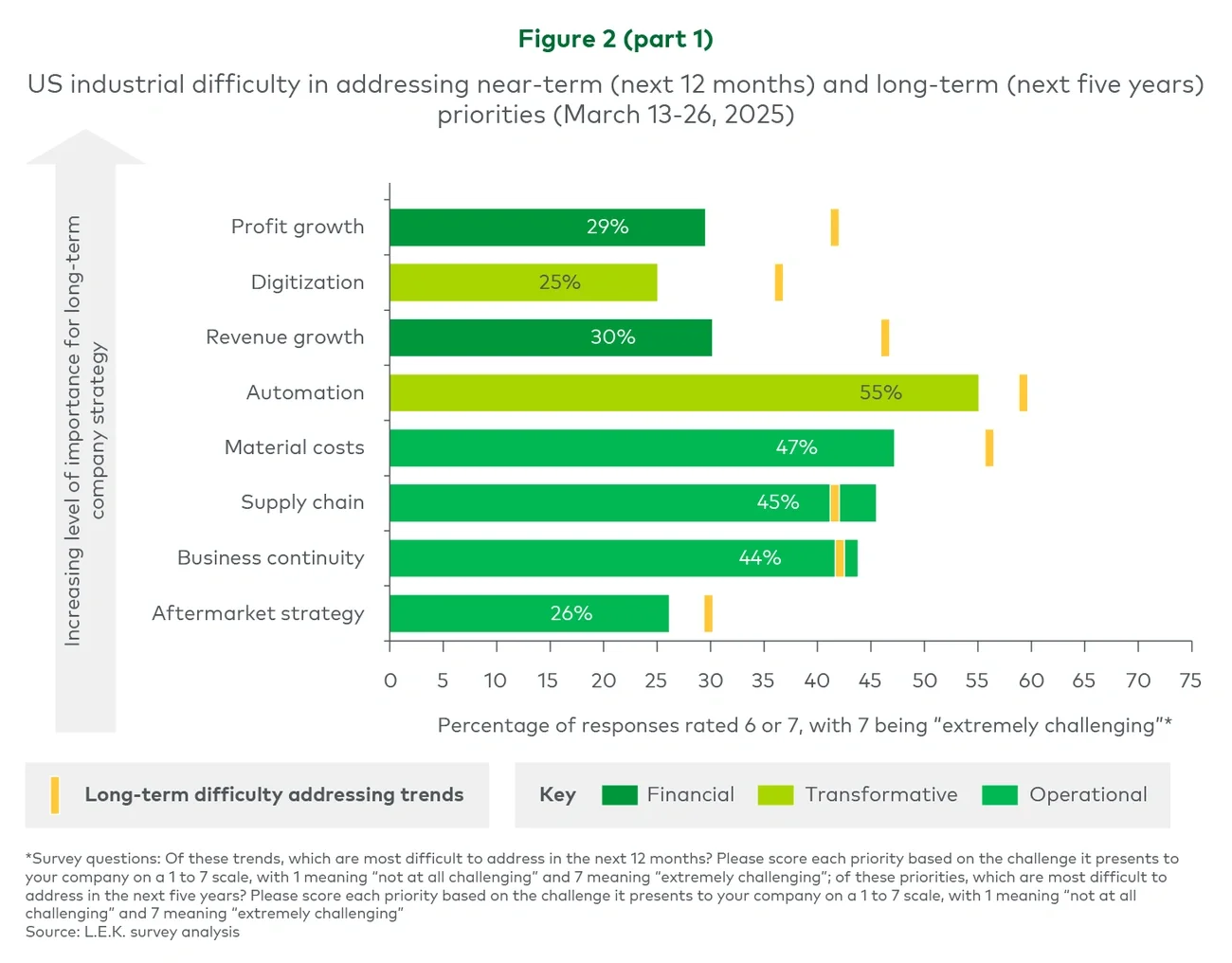

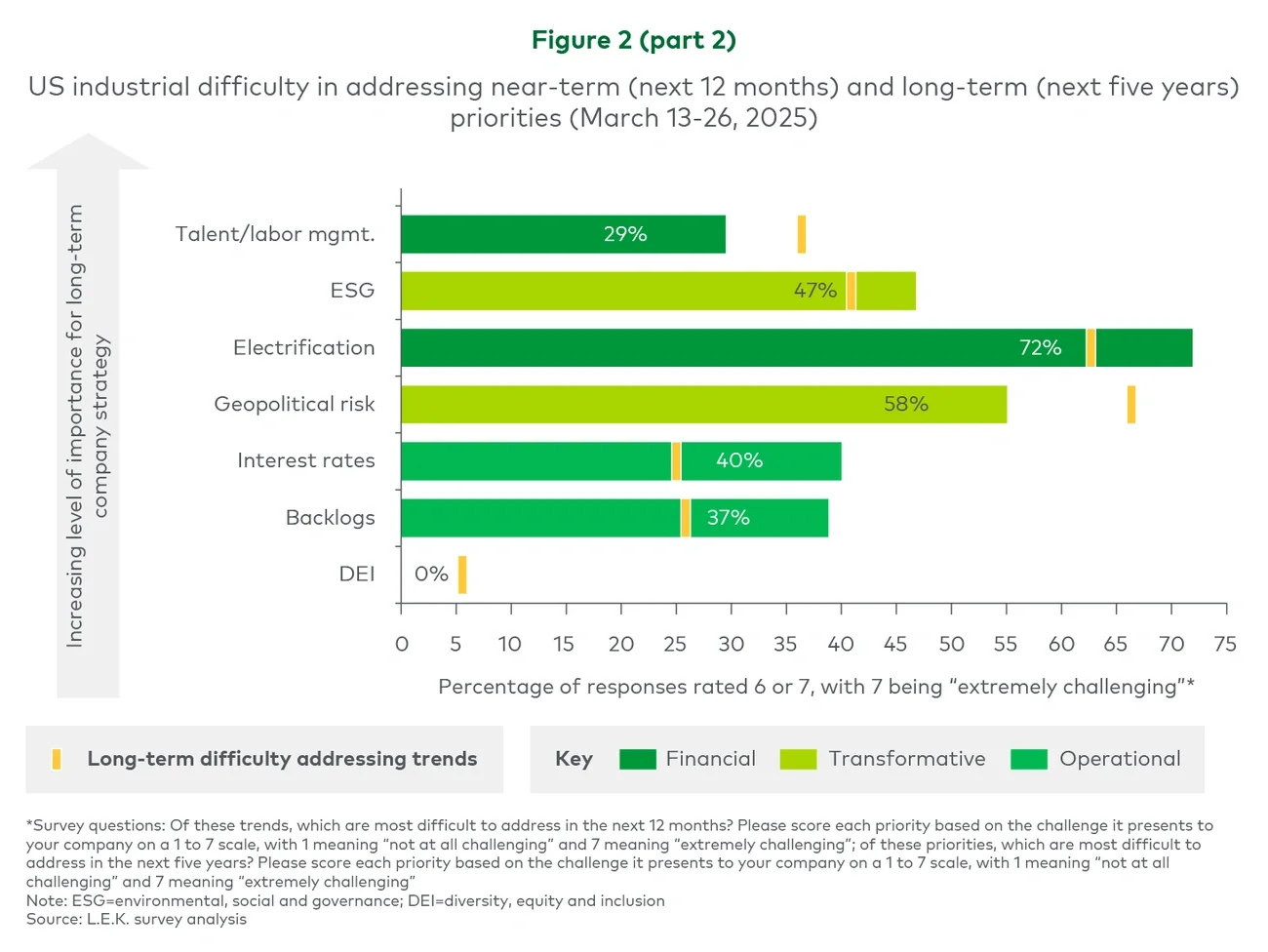

In the short term (i.e., the next 12 months), industrial companies are focusing on financial goals as well as digitization and automation, with other high-priority issues like supply chain and material costs slightly lagging. In the long term (i.e., the next five years), industrial companies have prioritized executing against their profitability and revenue goals.

Meanwhile, when it comes to automation and digitization, a greater proportion of firms appear to still be in the planning phase. Unsurprisingly, given that longer-term priorities often require more-involved planning and nuanced execution, U.S. industrial companies generally view them as more difficult to address (see Figure 2, parts 1 and 2).

Many industrial companies are expanding their use of digital solutions, with enterprise apps, customer data solutions and cybersecurity measures the most widely adopted so far. And the executives we surveyed expect such expansion to continue going forward.

That’s especially true when it comes to the adoption of generative artificial intelligence (AI). Industrial executives recognize the technology’s broad applicability to business functions and processes and plan to advance their implementation of it to increase efficiency. While most companies believe they are realizing significant value from AI, they are likely only utilizing a small-to-moderate proportion of the full functionality.

Digital solutions serve a wide range of business purposes, with some — such as customer data solutions for customer experience — being more tailored to specific initiatives and others serving broader applications. Increasing efficiency is the highest priority for AI usage among current users, while increasing competitiveness and expanding revenue streams rank lower in priority. But these are likely to grow in focus as manufacturing companies become more comfortable with implementing AI and stepping up their use of advanced functionality.

As our latest survey of industrial equipment and technology executives makes clear, financial priorities, particularly profit growth, remain key for executives.

That said, in light of the relative demand softness, revenue growth appears to have been slightly deprioritized in the near term relative to potential efficiency-boosting measures such as automation and digitization.

As one of our survey respondents put it, “As a manufacturing firm, the bottom line is always what you’re evaluated on. Top-line growth is always nice, but in this environment, everyone is really focusing on driving profitability.” Meanwhile, material costs/inflation have also become a more significant focus as executives await clarity on impending tariffs and other potential trade policy changes.

Industrial executives remain optimistic. But they know the ground is shifting beneath them, and until that shifting stops or at least slows down, they’re going to proceed with caution.

Those are the high-level themes that our survey of industrial manufacturing executives reveals. For a more granular picture, be sure to read our deep dives into the areas that those executives have made their top priorities: procurement and the supply chain, services and the aftermarket, pricing, electrification, and technology, notably automation and digitization.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

As B2B buyer behavior evolves, traditional sales and marketing tactics are falling short against increasingly digital, complex decision journeys.

These digital-first strategies are driving measurable gains in lead quality, sales efficiency and customer lifetime value across sectors.

Leading companies are inverting the funnel by targeting high-value accounts early and using personalized, insight-driven digital engagement from the outset.

To stay ahead, companies must align teams, embrace real-time analytics and build agile GTM engines grounded in experimentation and rapid iteration.

Could your sales and marketing strategy be unintentionally compromising revenue growth? Many organizations remain tethered to outdated tactics such as cold-calling, generic email blasts and static lead lists, despite their reduced efficiency. Today’s sophisticated decision-makers prefer personalized digital interactions, often conducting extensive online research and navigating multiple digital touchpoints before contacting sales directly. By holding on to conventional methods, businesses risk missing crucial opportunities and inadvertently sacrifice market share.

In contrast, leading organizations clearly embrace the new digital-first reality. According to L.E.K. Consulting’s research and analysis, 88% of decision-makers revisit vendor websites multiple times before finalizing purchasing decisions, and 53% rely heavily on social media for critical insights. Companies proactively responding to this shift with strategic clarity, precise targeting and personalized digital-first go-to-market (GTM) approaches consistently outperform their competitors — achieving greater lead generation, shorter sales cycles, improved conversion rates and higher overall revenue growth.

Understanding the significant shift in business-to-business (B2B) purchasing behaviors is essential to effectively engaging today’s sophisticated buyers. The modern decision-making process has clearly evolved from historical linear models into one characterized by:

Organizations that are slow to adapt to these evolving dynamics risk immediate revenue loss and diminished long-term market relevance. Clearly recognizing and proactively addressing these three critical realities — more stakeholders, increased touchpoints and heightened complexity — are essential for competitive success.

What sets successful digital-first GTM strategies apart? They begin with strategic clarity, precise audience targeting and the leveraging of real-time insights to foster deeper, more relevant buyer engagement. To accomplish this effectively, successful B2B organizations invert the conventional marketing funnel, prioritizing highly targeted and personalized interactions from the earliest touchpoints in the buyer journey (see Figure 1). This method allows them to engage decision-makers proactively, address specific buyer needs accurately and streamline their purchasing processes.

Companies implementing digital-first GTM strategies report substantial measurable outcomes, including:

These quantifiable successes stem from using advanced analytics, artificial intelligence (AI)-driven personalization and dynamic content strategies. Real-time data enables organizations to anticipate buyer behaviors accurately, respond rapidly and effectively to market changes, and allocate marketing and sales resources more efficiently.

Beyond measurable metrics, digital-first GTM strategies significantly improve organizational alignment, spur innovation and enhance overall operational efficiency. This clarity of purpose and action ensures companies not only achieve immediate revenue growth but also sustain long-term competitive advantages.

To see the tangible, transformative effects digital-first GTM strategies can deliver, consider the following real-world examples of clients that successfully implemented these methods:

These examples underscore how a well-executed digital-first GTM strategy translates directly into measurable business outcomes, enabling companies to capture market leadership and sustain growth.

To fully realize the potential of a digital-first GTM strategy, organizations must undertake deliberate, well-executed actions:

Despite clear digital trends, conventional sales and marketing tactics such as cold-calling, generic outreach and static content continue to struggle. According to our research, approximately 75% of senior decision-makers indicate that traditional static marketing content significantly delays their purchasing decisions.

Additionally, these conventional methods often result in operational inefficiencies, misalignment between the marketing and sales teams, and poor visibility into campaign effectiveness. Ultimately, conventional strategies are ill-equipped to address modern decision-makers’ nuanced, digitally driven decision-making processes, placing organizations at a distinct competitive disadvantage and jeopardizing revenue opportunities.

Recognizing the strategic value of digital-first GTM approaches demands immediate action. To translate this recognition into results, your organization must initiate targeted internal discussions, honestly evaluate current capabilities and promptly address critical gaps.

Though many organizations understand the significance of digital transformation, relatively few execute it effectively. This creates a valuable opportunity for proactive companies ready to lead. Embracing a digital-first GTM strategy today ensures increased market share, improved customer loyalty and sustained revenue growth.

The opportunity is clear, and the moment to act decisively is now — your organization’s long-term success depends on your commitment to digital-first GTM transformation.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

After a decade of localization mandates, China has finally put pen to paper on what ‘local’ means. The Ministry of Finance’s draft Notice for Comments (dated 5 December 2024) sets out three criteria for a ‘local’ product — substantive in-China transformation, a minimum cost percentage of components produced in China, and in-country completion of key components/manufacturing steps for certain products.

While this marks progress towards a national definition of ‘local,’ the granular thresholds, definitions of ‘key components/manufacturing steps’ and enforcement mechanics remain unclear — and cross-agency coordination is still a work in progress. This leads to varied hospital-level interpretation.

Until clarity lands, multinational medtech leaders must scenario-plan footprints, engage regulators early and prepare for more stringent procurement requirements.

Learn more about how L.E.K. can help MNC medtechs navigate China’s localization strategy and translate it into actionable initiatives and competitive advantage by downloading our analysis.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

Loading transcript...

In this latest conversation, Chinmay Jhaveri, Partner at L.E.K Consulting’s Global Education Practice, and Professor Yusra Mouzughi, Provost of the University of Birmingham Dubai, discuss the growth trajectory of the university in the region.

The discussion focuses on the institution’s phased development — from vision and planning through to a state-of-the-art campus and a growing academic impact.

Watch the video to explore how strategic partnerships and a clear commitment to excellence are shaping Birmingham Dubai’s next chapter.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

Clinical trials are growing in complexity and cost, prompting global pharma to seek more efficient markets.

Brazil represents only ~2% of global trials but has strong potential due to its population and infrastructure.

Regulatory improvements and local capabilities could make Brazil a regional hub for clinical research.

Healthcare institutions must act strategically to capture the emerging opportunity in the clinical trial landscape.

Clinical trials are essential for validating the safety, efficacy, and optimal dosing of new drugs, serving as a crucial step in bringing innovative therapies to market. Despite their critical role, clinical trials are inherently complex, lengthy, and resource-intensive processes. On average, developing a new drug takes more than a decade and costs over USD 2 billion per successfully approved medication. Moreover, the success rates from Phase I trials to regulatory approval typically range from only 5% to 15%, highlighting the significant challenges and risks involved in pharmaceutical research and development (R&D).

The global clinical research market currently exceeds USD 70 billion annually and is poised for continued growth. This growth is driven largely by increasing complexity and specialization within drug development. As the availability of straightforward, widely applicable drug targets diminishes, pharmaceutical companies are focusing on breakthrough innovations and advanced therapeutic approaches, such as gene and cell therapies. These cuttingedge therapies often target complex conditions and rare diseases, requiring sophisticated technologies and methodologies. Additionally, the specific and narrow patient populations associated with these advanced treatments make patient recruitment more challenging and extend trial timelines. Heightened regulatory scrutiny and increasingly intricate trial designs further contribute to escalating costs and longer development durations.

As the cost of drug development continues to rise, global pharmaceutical companies are increasingly seeking more cost-efficient markets for clinical trials. Brazilian healthcare institutions are well-positioned to capitalize on this shift by identifying and activating their distinct capabilities to gain relevance in the expanding clinical research industry.

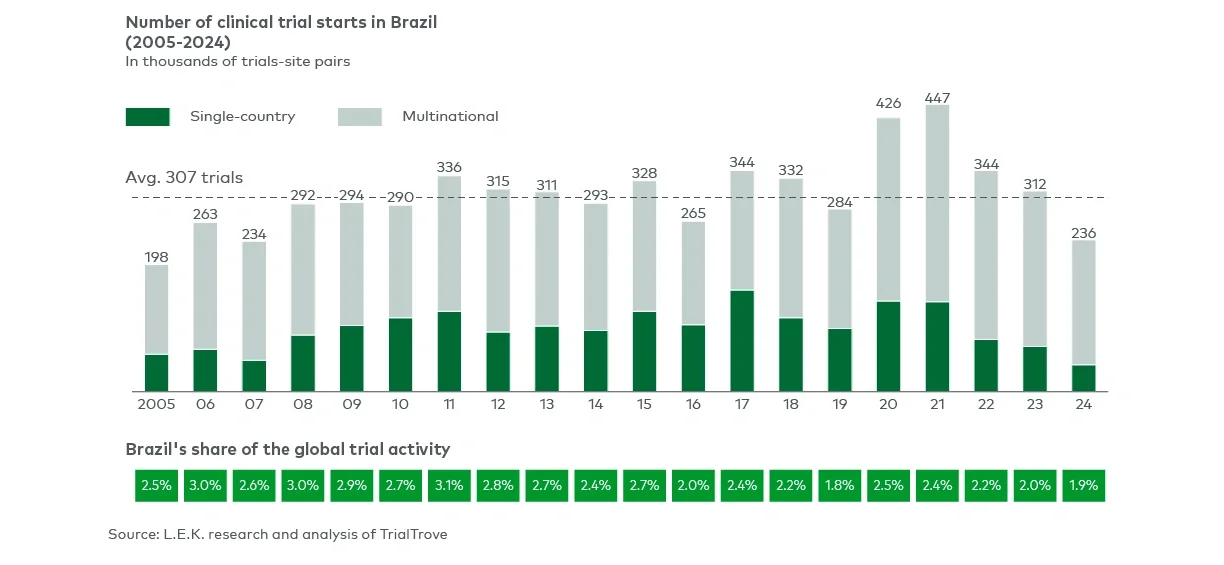

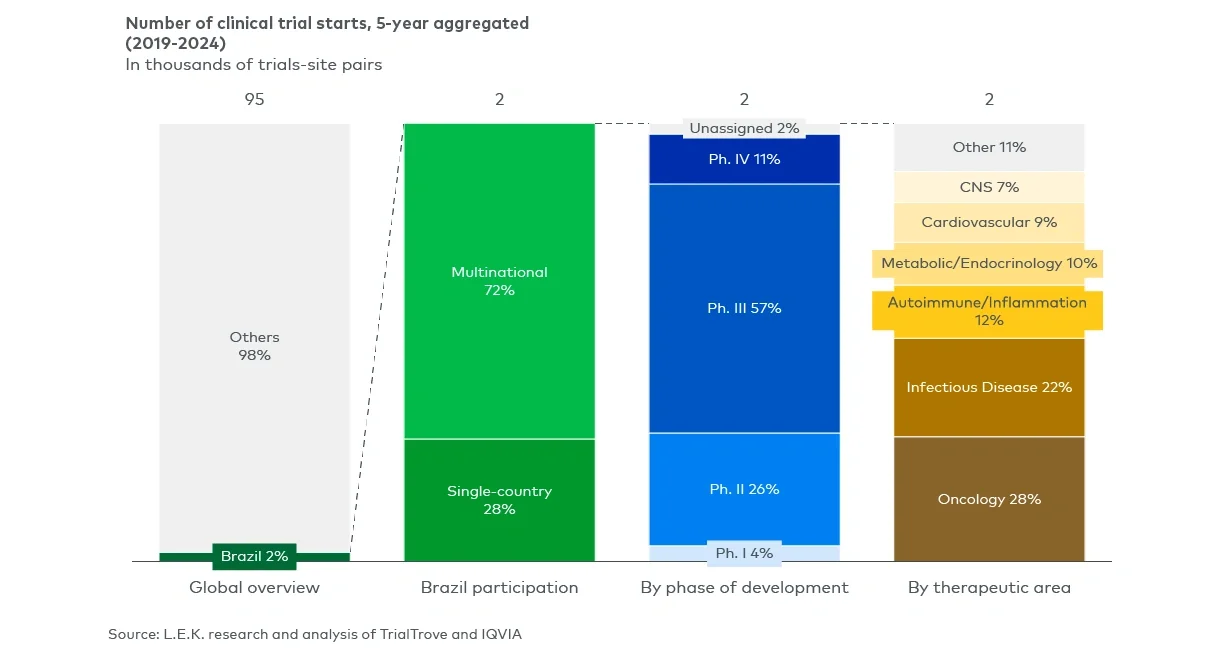

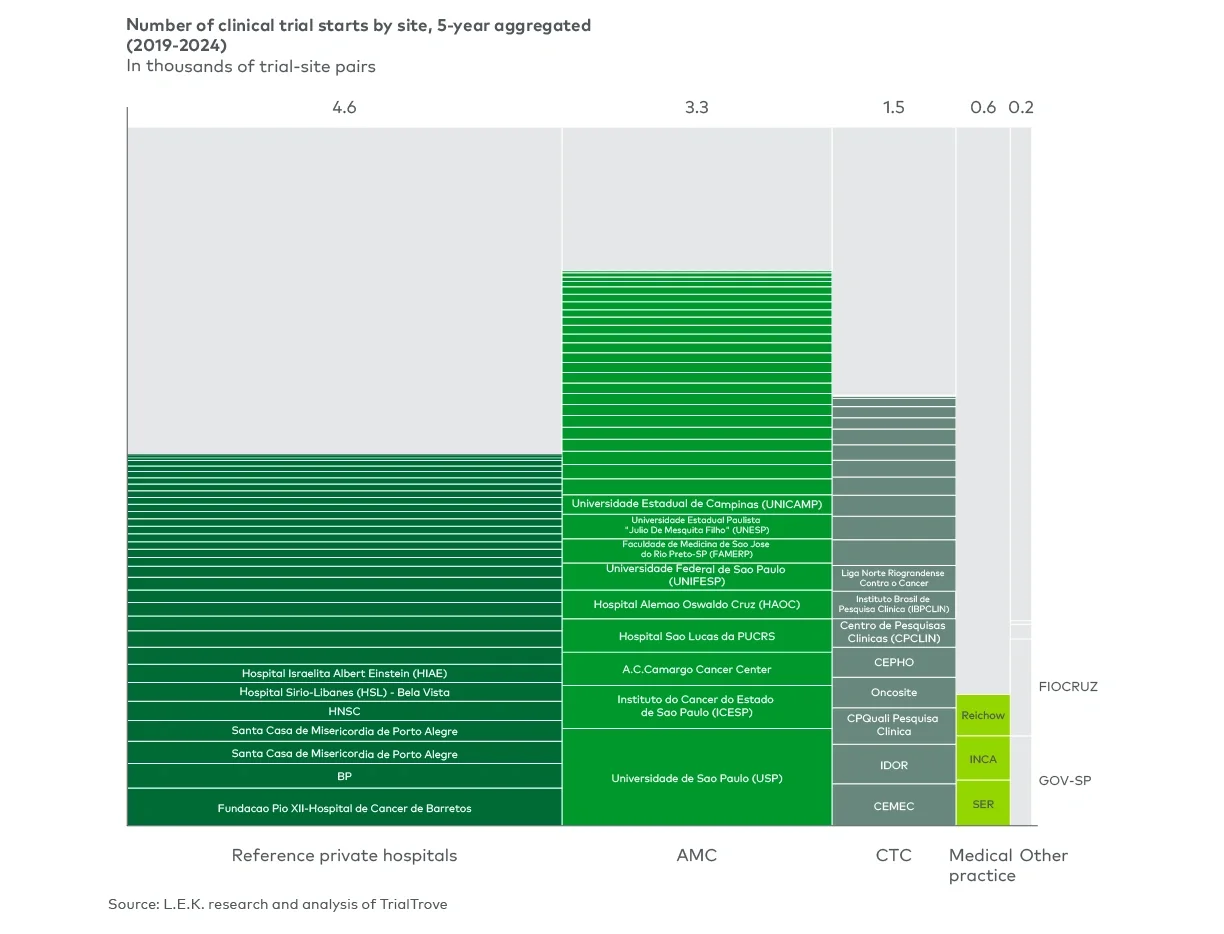

Brazil participates in approximately 300 clinical trials annually, representing only about 2% of global clinical trial activity (Figure 1). Most trials conducted in Brazil are multinational and concentrated in late-stage development phases (Phase III and IV), primarily focusing on therapeutic areas of high relevance such as oncology and infectious diseases (Figure 2).

Figure 1

Clinical trial history in Brazil

Figure 2

Brazil as a destination for clinical trials

Brazil presents unique competitive advantages that position it strongly for increased participation in global clinical trials:

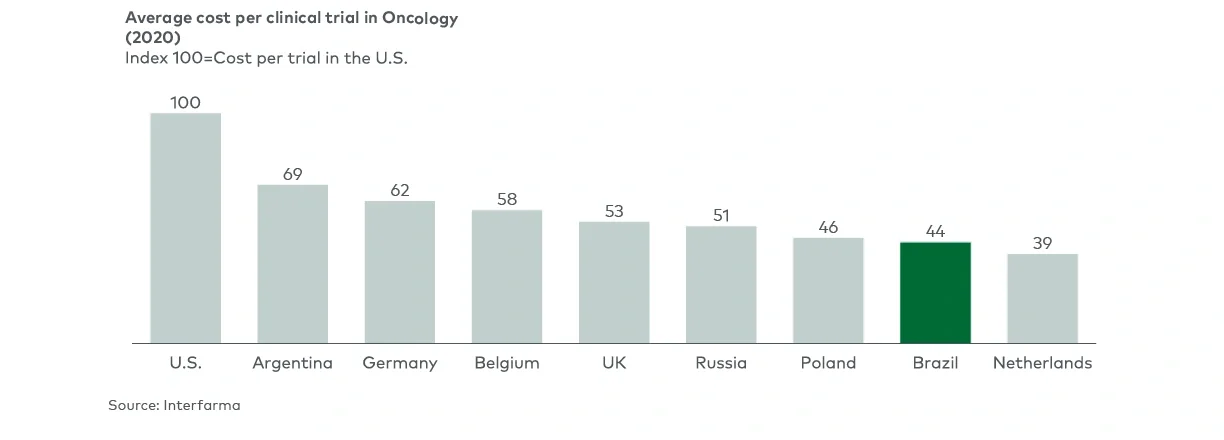

Figure 3

Cost-effectiveness of trial operations in Brazil

As global sponsors increasingly seek cost-effective, high-quality clinical research environments, local healthcare institutions in Brazil are in a strong position to lead. Their proximity to patients, integration within care delivery, and reputation among physicians give them a strategic edge in clinical trial execution. Yet, to fully capture this opportunity, institutions must evolve from passive research participants to proactive research enablers.

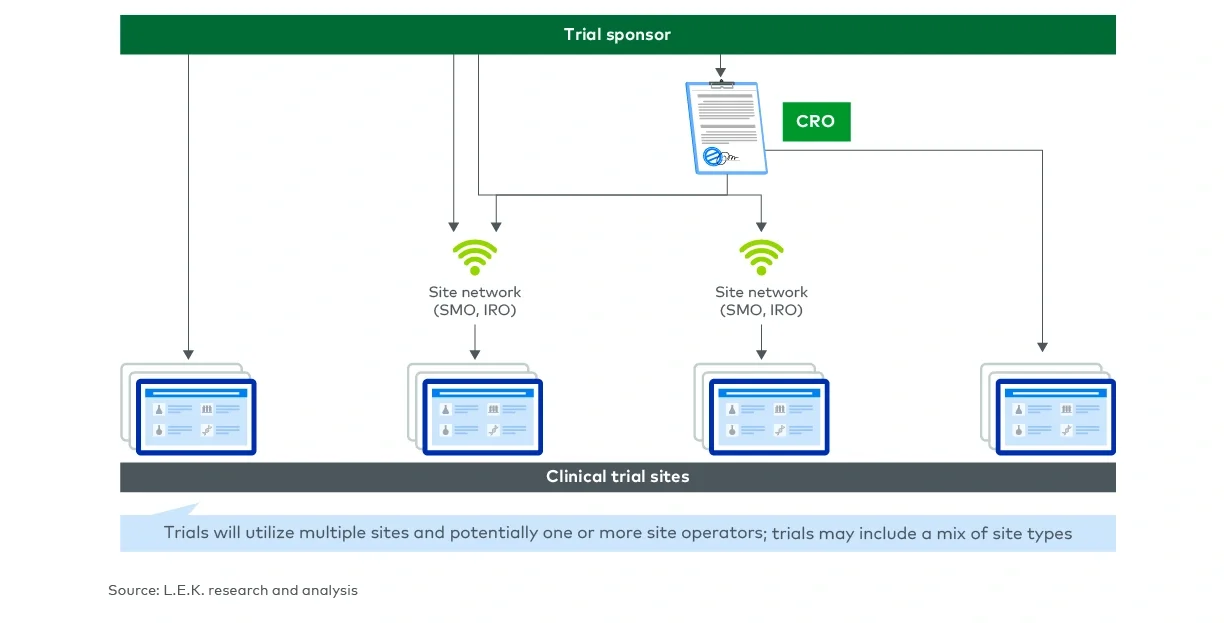

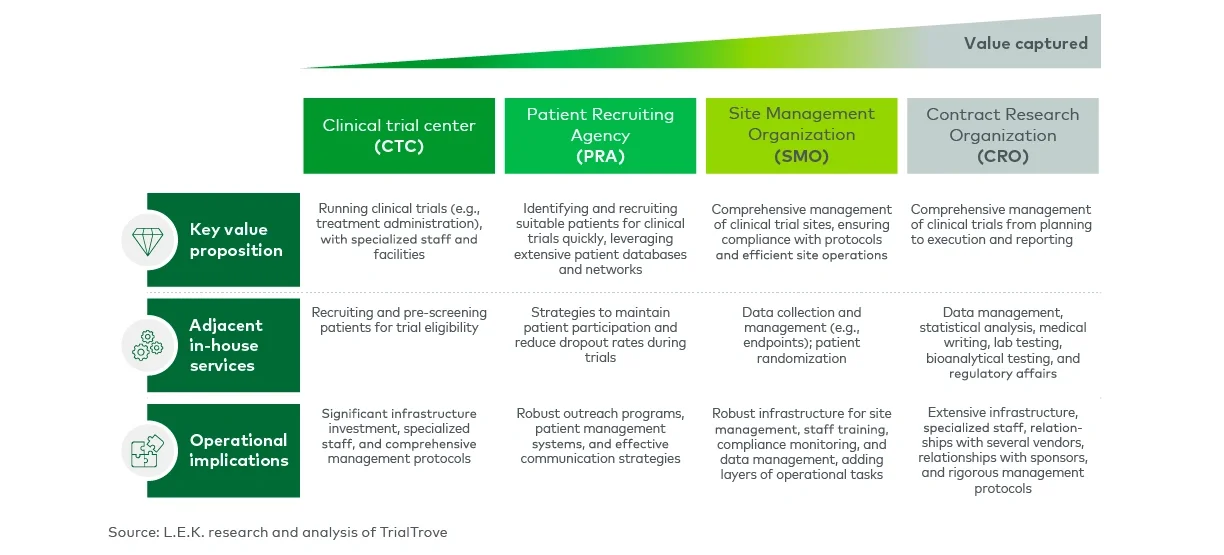

Clinical trial activities are often performed by a range of players (Figure 4). Trial sponsors oversee the overall trial and may handle high-level functions such as regulatory submissions and site selection, but often outsource day-to-day management to CROs, who typically manage the operations, ensuring compliance, and conducting site monitoring and coordination to keep the trial running smoothly. Clinical Trial Site Operators (e.g., Site Management Organizations - SMOs, Integrated Research Organizations - IROs), are contracted by CROs or sponsors to manage individual sites or networks. Clinical Trial Sites are usually owned or managed within a network, with operations tailored to the therapeutic expertise of their principal investigators.

Figure 4

Clinical trial key stakeholders

Brazilian institutions primarily operate as clinical research sites, delivering trial services such as patient recruitment, treatment administration, and follow-up. Some have expanded into broader roles akin to Contract Research Organizations (CROs), though differentiation against global CROs remains limited. However, when acting as site operators, Brazilian institutions can offer distinctive advantages across the clinical trial value chain.

Participating in clinical trials as research sites creates substantial upside for local healthcare organizations:

Despite these advantages, Brazil’s research landscape remains fragmented (Figure 5). Around 50% of trials are concentrated in reference private hospitals, with the remainder split across academic centers, medical practices, and dedicated clinical trial centers. This fragmentation leads to inefficiencies, variability in quality, and lower sponsor confidence.

Figure 5

Clinical research site players in Brazil Number of clinical trial starts by site, 5-year aggregated

In contrast, the clinical research landscape in the United States is shifting toward consolidated site networks, replacing traditional individual site models. Scaled site operators provide greater efficiency, centralized trial management, enhanced patient recruitment capabilities, and strengthened relationships with sponsors, positioning themselves as preferred partners. This shift toward consolidation, often driven by private equity investments, is a potential strategic direction for Brazil, where scalability could become a significant competitive advantage.

Brazil has a window to adopt this model and reshape its research infrastructure. Institutions that lead this transformation will not only capture greater sponsor interest but also shape the standards for Brazil’s clinical research future.

Brazilian healthcare institutions interested in scaling their participation in clinical research must make deliberate, strategic choices. A clear roadmap can help guide their evolution from isolated sites into integrated research leaders:

Figure 6

Potential positioning archetypes for local healthcare organizations

The institutions that take clear, structured steps now—by defining their role, establishing the right partnerships, and scaling effectively—will shape the next phase of Brazil’s clinical research ecosystem. Those who lead will not only capture market growth but also help position Brazil as a global reference in clinical trials.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

Consumption-based and hybrid pricing models are becoming the SaaS standard, with 85% of companies already using or implementing usage-based strategies to better align revenue with product value.

Enterprise buyers now prefer usage-based pricing, with 39% of CIOs favoring models tied to actual consumption, signaling a broader shift in how software value is measured and purchased.

Hybrid models outperform subscription-only pricing, delivering stronger revenue growth and EBITDA margins while offering a more stable foundation for scaling AI-powered products.

The usage-based premium may fade over time, as the model becomes more common and macro conditions shift. Long-term success depends not on adopting the model, but on executing it effectively across pricing, forecasting and customer experience.

Artificial intelligence (AI) is pushing software-as-a-service (SaaS) companies to align pricing with product value. Usage-based and hybrid models are now used by over half of SaaS providers and are emerging as the most effective path to scalable growth, profitability and stronger valuations.

This Executive Insights, the final in our series on AI-driven pricing models, focuses on the rise of consumption-based pricing and its growing role in monetizing AI-powered products.

Earlier parts explored the key shifts shaping how SaaS companies price and monetize generative AI (GenAI) features:

Now we turn to what comes after the price tag: focusing on how to operationalize and forecast AI monetization at scale, especially when pricing is tied to consumption.

GenAI has widened the gap between how value is delivered and how revenue is captured. As we covered in Part 3, when pricing is tied to seats but value comes from usage, traditional SaaS metrics like annual recurring revenue (ARR) and net recurring revenue (NRR) become less reliable indicators of growth and retention.

In response, many software companies are adopting usage-based pricing models that better align revenue with actual product engagement. Some have moved to fully usage-led approaches, while others are layering usage into more traditional pricing structures. These models are gaining traction across all types of products and company sizes, from backend infrastructure to customer-facing tools.

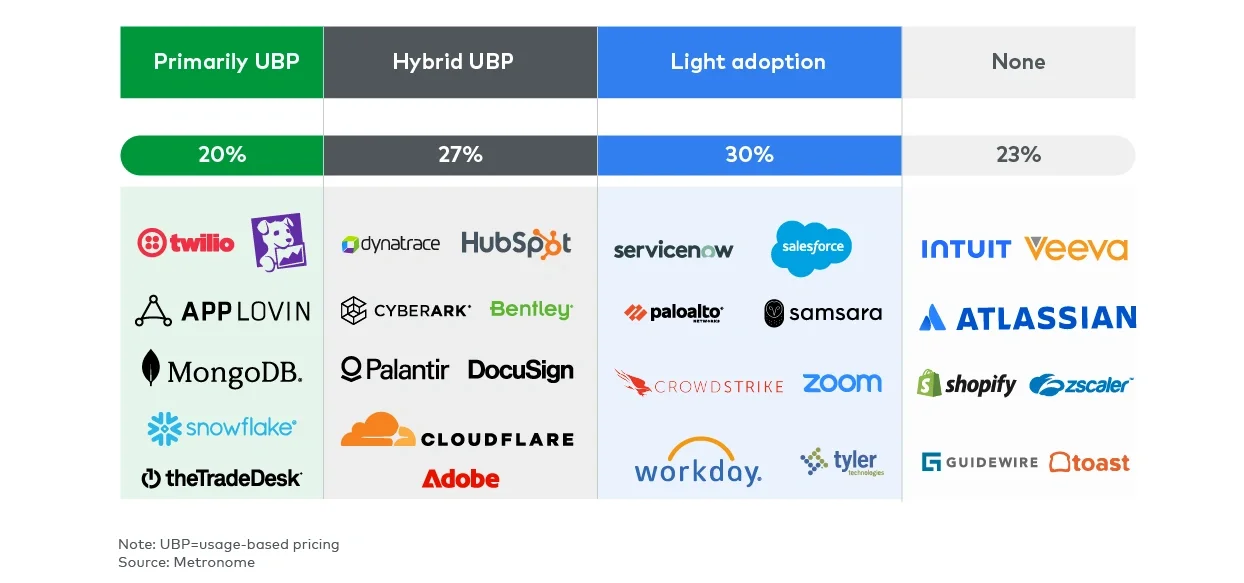

In a recent survey, 85% of SaaS companies said they already use usage-based pricing or are actively implementing it. Among enterprise software providers, 77% have incorporated consumption-based models into their revenue strategies. This marks a clear shift from emerging idea to enterprise standard (see Figure 1).

Figure 1

State of usage-based pricing

Only 23% of enterprise companies in the sample have yet to adopt usage-based pricing, but the landscape is far from binary: Many SaaS businesses are testing models between subscriptions and usage-based approaches to better reflect customer value.

Flat fees remain common in some segments, while others are piloting outcome-based pricing tied to results. As highlighted in Kyle Poyar’s report, “The state of B2B monetization in 2025”, these shifts reflect a broader move toward flexible, performance-driven strategies.

While this Executive Insights focuses on usage-based pricing, that shift is central as SaaS companies adapt to the demands of AI-powered products.

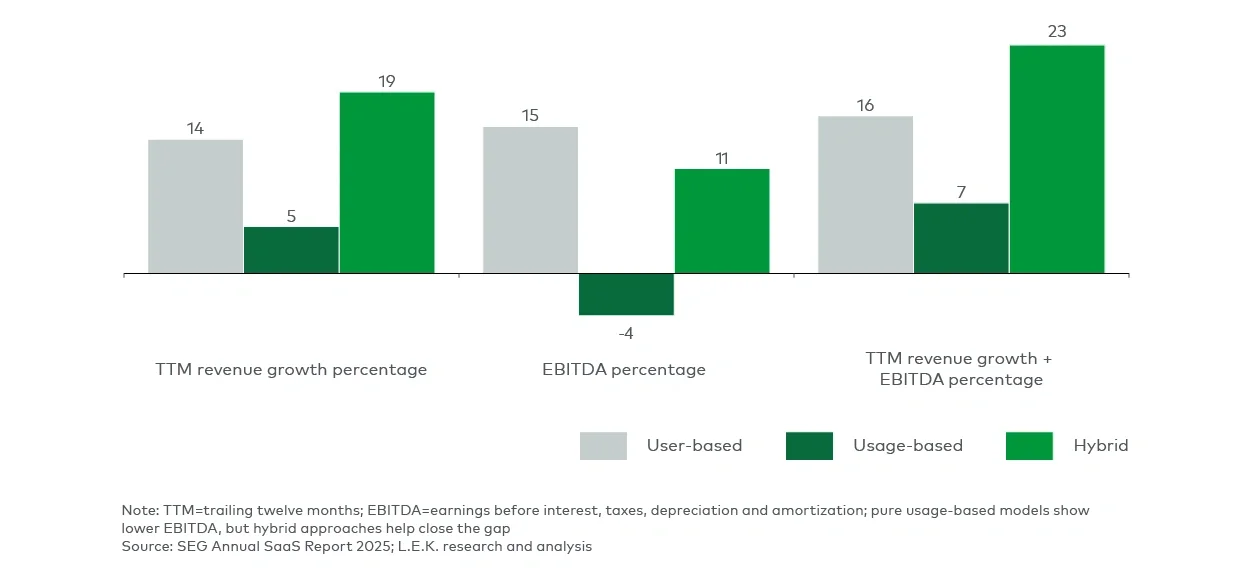

As more companies seek to capture the full value their products deliver, pricing models are evolving to reflect that payoff. Recent data shows that companies using hybrid pricing models achieve average revenue growth of 19% and EBITDA margins of 16%. These results outpace subscription-only peers, which often face tighter growth ceilings and margin pressure.

Hybrid models also help mitigate the revenue volatility that can accompany pure usage-based strategies, offering a more stable foundation for scaling AI-powered products (see Figure 2).

Figure 2

Hybrid pricing models outperform purely consumption-based pricing models

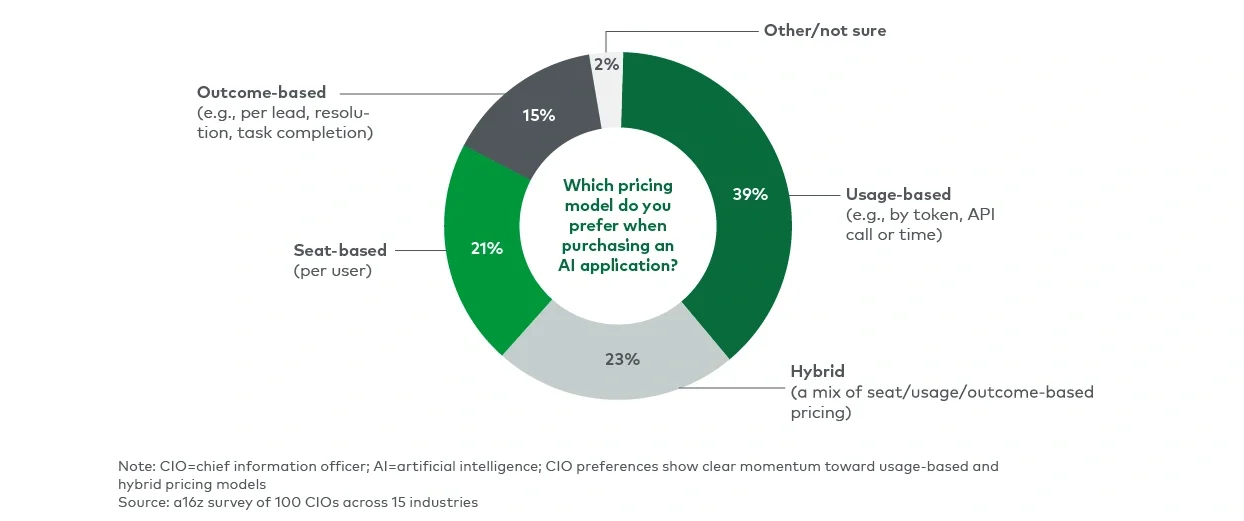

Buyer preferences tell an even clearer story. In a recent Andreesen Horowitz (a16z) survey of 100 chief information officers (CIOs) across 15 industries, usage-based pricing emerged as the most preferred model, with 39% of CIOs saying they favor pricing tied to tokens, API calls or time. Hybrid models, which combine seat, usage and even outcome-based components, came in second at 23%, while traditional seat-based pricing lagged at just 21% (see Figure 3).

Figure 3

How 100 enterprise CIOs are building and buying GenAI in 2025

This reflects a shift in enterprise buying behavior. Predictable billing is no longer the top priority. Instead, flexibility and alignment with actual usage are what drive purchasing decisions. CIOs are increasingly comfortable with the variability of usage-based pricing, especially as AI workloads such as large language models become more granular and performance-driven.

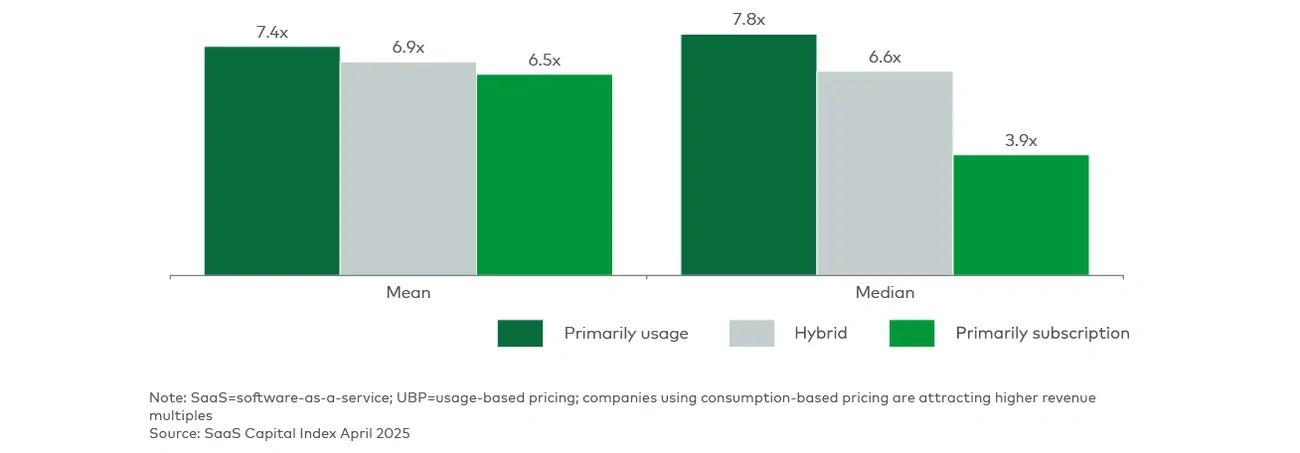

Companies implementing consumption-based pricing continue to trade at a premium, despite lower margins and weaker Rule of 40 performance. That premium is driven by investor expectations: usage-based models are seen as enablers of stronger NRR and more-effective land-and-expand growth (see Figure 4).

Figure 4

Valuation multiple (on revenue) for SaaS Capital Index companies using UBP vs. peers (April 2025)

However, there are signs that premium may not last:

The premium may narrow as the model becomes more common and macro conditions evolve. In the end, success depends less on adopting usage-based pricing and more on executing it well.

Pricing GenAI features was only the beginning. The bigger opportunity lies in building monetization strategies that scale. These strategies reflect how customers experience value and support long-term growth.

Consumption-based and hybrid models are becoming the norm because they reflect how customers buy and how SaaS companies scale. But pricing alone is not enough. Top performers are also rethinking metrics, forecasting and adoption.

L.E.K. Consulting has deep experience helping SaaS companies rethink pricing in the face of changing customer expectations, evolving value delivery and the rise of GenAI. If your team is working through how to price, package and scale more effectively, we can help. Contact us to start the conversation.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

Loading transcript...

In the final video in our series on IT service landscape, Aakash Gandhi explores how different revenue models influence valuation multiples and value creation opportunities across the IT services market in Australia and New Zealand.

He provides a comparative view of six core segments, highlighting where recurring revenue supports premium valuations, where consolidation plays are most viable and where segment dynamics pose greater challenges.

From cybersecurity and cloud consulting to SaaS and managed IT, the video offers a strategic framework for assessing risk, scalability and investment potential in a fragmented but evolving market.

Watch now to find out more.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

Loading transcript...

In the second video in our series on IT service Landscape, we introduce a two-by-two matrix to evaluate six core IT service segments in Australia and New Zealand, comparing them based on growth potential and margin profiles.

The analysis highlights where the most attractive opportunities lie, such as managed cybersecurity services in the mid-market, and where caution may be warranted, such as digital services under pressure from AI and offshore delivery.

The video also explores the nuances of segments like SaaS, cloud consulting and managed ICT, helping investors better understand where scalable growth and platform potential exist — and where value may be harder to unlock.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC