These shifts signal a broader trend. ARR is still the headline number, but its meaning is changing. Understanding what sits underneath the label is now just as important as the number itself.

Beyond ARR: The new metrics supporting usage-based growth

Even with new definitions like CARR and UARR, headline metrics rarely tell the full story. To forecast growth more reliably, companies need granular, behavior-based indicators that show how customers ramp, expand and stabilize over time. These include:

- Realized versus predicted revenue: A feedback loop for forecasting accuracy

- Time to usage: Onboarding speed as a proxy for time to revenue

- Usage ramp rate: Consumption growth during the first six to 12 months

- Usage volatility: Stability and predictability after ramp-up

- Cohort and customer-level tracking: Segmenting usage and retention trends to improve forecasting precision

These metrics help companies navigate usage-led pricing and give investors clearer visibility into AI-driven growth. To support this shift, many teams are rethinking how they use traditional revenue frameworks. NRR and GRR still matter, but both can mislead: NRR often appears inflated during ramp periods, while GRR understates growth by excluding expansion. Some investors view NRR below 90% as a red flag, prompting deeper scrutiny of ARR. That makes it even more important to pair headline metrics with usage-based indicators and customer-level forecasting.

Together, these new metrics reflect a more dynamic way of measuring performance that emphasizes not just what is sold, but also how customers grow and engage over time.

The cross-functional impact

Adopting new metrics is just the beginning. Turning usage-based pricing into a scalable, companywide strategy requires deep coordination across every function. This includes how deals are structured, how revenue is tracked and how performance is evaluated.

- Sales teams need compensation plans that reward consumption and long-term growth, not just up-front deal size

- Customer service and product must monitor and drive usage milestones that lead to expansion

- Finance and operations are reworking billing systems, revenue recognition processes and cash flow models

- Leadership and investors are looking for new ways to evaluate performance, especially during ramp periods when metrics like NRR can appear inflated

Monte Carlo, a data and AI observability company, took this challenge head-on. Their team described AI-native usage as “spiky,” with unpredictable patterns that made traditional monthly forecasts unreliable. In response, they shifted to daily revenue tracking. Pricing ownership moved to product, and go-to-market roles were rebuilt to better align with real-time customer behavior. Daily revenue became the shared performance metric across teams and board reporting, creating tighter alignment between product value and customer outcomes.

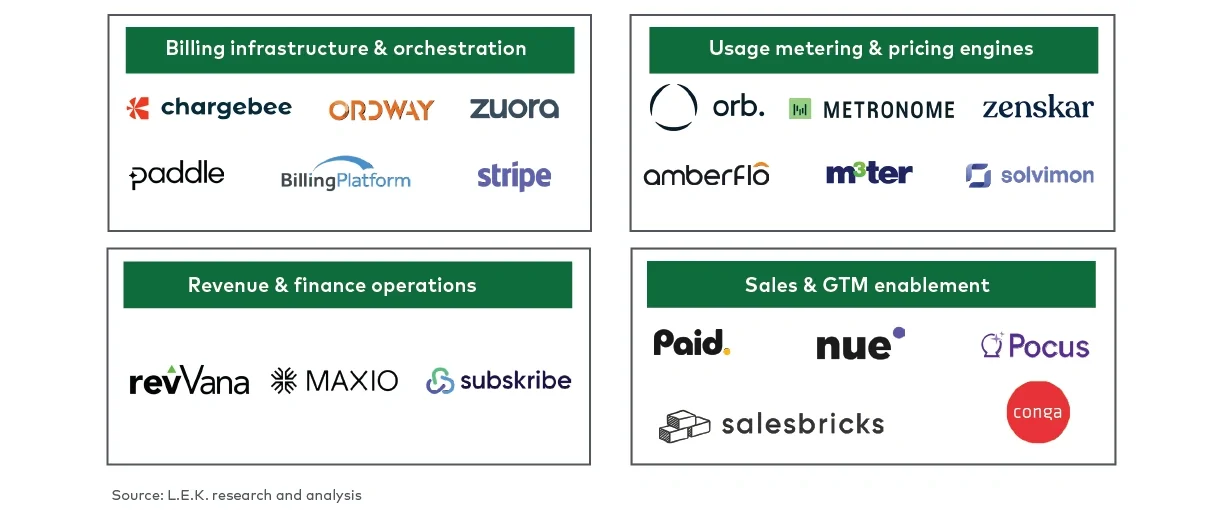

The rise of enablers

To support transformations like this, a new category of enablement tools has emerged. These platforms help SaaS companies meter usage, automate billing, recognize revenue and manage flexible pricing models (see Figure 4).