Redefining strategy and operations

Private label

Private label (PL) has evolved from a cost play into a strategic pillar where sophisticated retailers have developed good-better-best tiers within PL that improve margin and build customer loyalty.

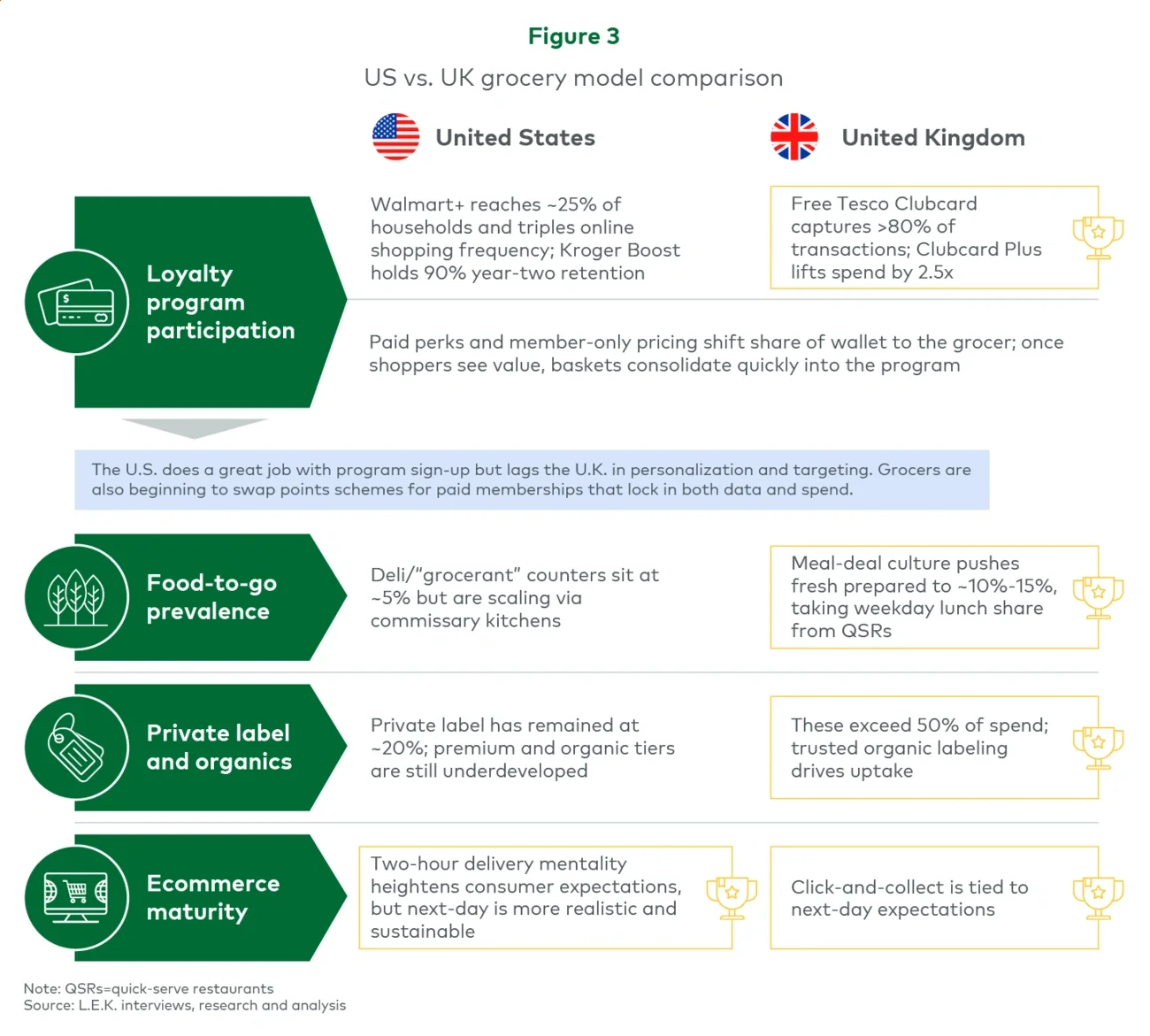

Despite the success retailers model, regional progress on PL varies. On one end, U.K. private label penetration exceeds 50%, Germany is nearing 50% and in Brazil, GPA’s wellness lines are outpacing the market by a factor of two. In contrast, most U.S. grocers lag at approximately 20% penetration, and Coles/Woolworths in Australia is at about 25%, leaving substantial headroom.

Tiered strategies are the benchmark. Tesco’s three-tiered range (Everyday Value, Tesco Own Brand and Tesco Finest) accounts for over 60% of Tesco’s food sales. Sainsbury’s and Loblaw (Canada) deploy similar models that align with shopper budgets while maintaining quality perceptions.

But innovation appears to be the new private label frontier. Costco’s Kirkland Signature has grown into about a $60 billion brand, rivaling top national labels. Metro’s Irresistibles line in Canada has expanded into more than 2,600 stock-keeping units (SKUs) across wellness, gourmet and ethnic cuisines, many of which outperform national brands in quality testing.

Loyalty and personalization

Leading UK grocers such as Tesco and Sainsbury’s have introduced loyalty pricing that acts as a strong value signal against discounters and encourages high loyalty card usage. The richness of data then supports personalized promotions and offers through dedicated apps.

In the U.S., grocers are generally still focused on simpler points-based or cash-back systems with limited personalization.

Store network optimization

Leading grocers are evolving their facilities to meet the distinct demands of their operating environments. Rather than cutting physical footprints, retailers are redistributing space and trying new concepts to better align with urban growth and digital fulfillment needs.

Some are using “urban formats” and microfulfillment centers to boost convenience and last-mile efficiency. Tesco (U.K.; 600-plus Express locations) and Carrefour (France; 1,500-plus Market/City stores) have deployed smaller-format stores that serve as both walk-in locations and click-and-collect hubs. Aeon (Japan) is deploying multistory urban stores with fulfillment centers in the basement that execute under-30-minute delivery in Tokyo’s dense neighborhoods.

And some have created hybrid stores that turn retail into a destination. Carrefour and Aeon have invested in combining grocery with nonfood retail, childcare centers and community clinics to increase trip frequency and deepen consumer loyalty. Carrefour’s “Act for Food” stores in LATAM, for example, are designed around healthier food choices, community space and omnichannel pickup lockers.

Pricing

Dynamic pricing driven by artificial intelligence (AI) is no longer experimental; Kroger (U.S.) and Tesco (U.K.) now use these tools at scale to offer personalized promotions that drive higher basket sizes and repeat purchases. Kroger reported in 2023 that households receiving personalized digital offers spent 20% more per trip than nonparticipants.

Meanwhile, Aldi’s and Lidl’s no-frills, transparent pricing structures continue to reshape shopper expectations. In Germany and the U.K., both discounters have gained share steadily over the past decade, now commanding close to 50% combined in Germany and approximately 20% in the U.K. Traditional grocers are being forced to simplify their promotional architecture and win back price-sensitive shoppers with clarity and consistency with their offers

Product offering insights: Vary levels of standards

Frozen vs. fresh

Japan’s leadership in frozen food, explored previously in L.E.K.’s 2023 prepared foods insight, challenges the Western perception that frozen equals inferior. Aeon’s dedicated @Frozen stores stock more than 2,000 SKUs, including sushi-grade fish, gourmet pasta and artisanal desserts. 7-Eleven Japan delivers frozen, chilled and ambient-temperature goods through separate daily routes, enabling fresh-like quality with frozen convenience.

While penetration in the U.S. of frozen food is not that low, sophistication and frequency of use lags most advanced markets by far. In the U.S., frozen food categories grew about 8.5% in 2023, according to IRI, as inflation pushed shoppers toward longer shelf life and meal-prep ease.

U.S. grocers continue to lag in fresh shrink optimization efforts. Marks & Spencer in the U.K., by contrast, uses predictive markdown algorithms to reduce fresh waste by more than 20%.

Packaged goods

Approaches to product selection vary by region, with varying consequences. In the U.S. and Canada, grocers often carry more than 40,000 SKUs per store. While providing customer choice, this complexity drives costs higher and diffuses value messaging.

U.K. grocers are moving in the opposite direction and reducing SKUs by 20%-30% in many categories in order to focus on high-velocity and private label items. Tesco reports improved inventory turnover and better supplier negotiation leverage as a result.

In LATAM and APAC, assortment curation is becoming a competitive differentiator, particularly in smaller formats targeting urban shoppers.

Nonfood products and services

Leading U.S. stores are attracting new traffic and increasing dwell time through nonfood and service offerings; e.g., Walmart’s health centers and Kroger’s in-store clinics. Pharmacy sales are also a key footfall driver in competitive U.S. markets.

China’s Hema stores have a second function as logistics hubs, processing more than 50% of orders online, with many fulfilled in under 30 minutes. This level of integration drives basket expansion and blurs the line between retail and fulfillment.

Spotlight on US vs. UK: A tale of two grocery models

A comparison of the largest market (U.S.) with the global grocery leader (U.K.) showcases clear growth areas for the U.S. (see Figure 3).