Healthcare organisations face increasing pressure to optimise operations, expand access and enhance patient outcomes against a backdrop of changing regulations, tariff pressures and evolving patient needs. For multi-service healthcare providers — often juggling multiple specialties, facilities and care delivery models — identifying and resolving constraints that hinder core service growth is critical to clinical excellence, operational performance and financial sustainability.

This Executive Insights draws on L.E.K. Consulting’s recent project experience to illustrate how a structured strategic review can uncover underperforming or non-contributory services and streamline clinical support functions and overheads.

Beyond merely cutting costs, a strategic review lets healthcare organisations redeploy resources where they are needed most, improve care pathways and deliver a better patient experience.

Context and analysis

For many healthcare providers, constrained resources — clinical workforce shortages, insufficient facility space and tight budgets — can hamper the development of core services. This was especially true for one large healthcare network we advised, where loss-making service lines eroded profitability and impeded much-needed investments in higher-value clinical areas.

A comprehensive strategic review uncovered multiple non-contributory or underperforming service lines and under-optimised support functions. Taken together, these areas diverted resources away from promising growth segments, leading to inefficiencies and hindered patient outcomes.

Approach

A structured methodology — tailored to the complexities of both clinical operations and administrative services — is critical for sustainable improvements. This involves establishing clear financial visibility, identifying underperforming areas and aligning resources with the organisation’s strategic priorities.

Care delivery

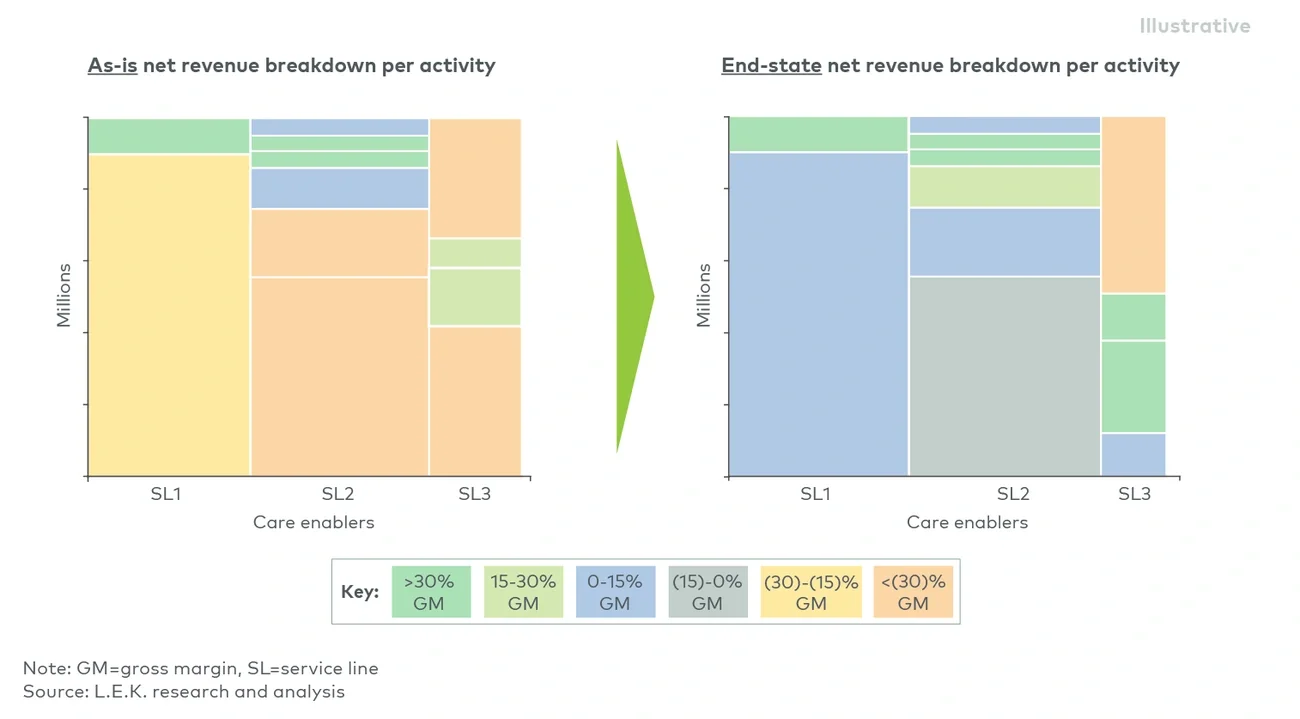

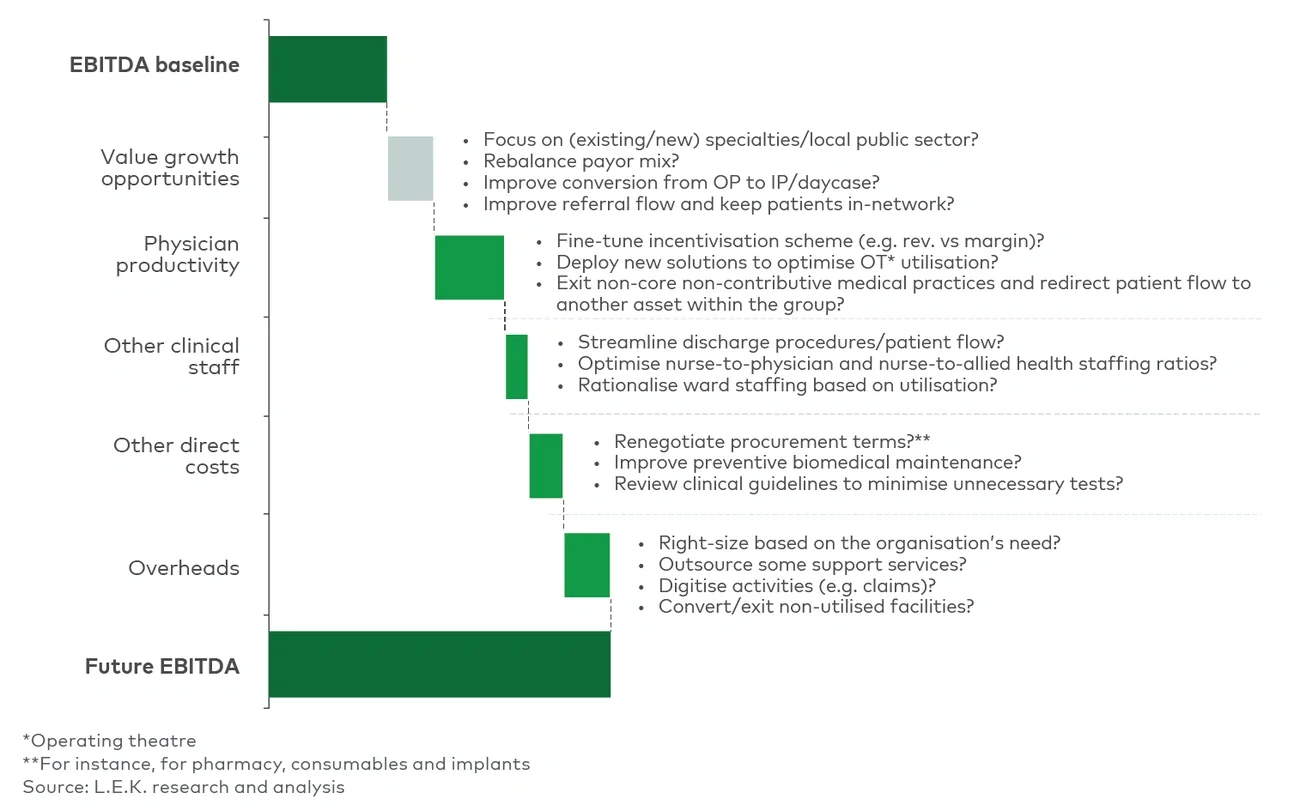

A key first step is to establish a financial baseline using activity-based costing (ABC). Shared cost centres — such as pharmacy, imaging, operating theatres and wards — often obscure the financial contribution of individual services. ABC clarifies how each service line contributes to overall margins, helping to identify high-impact areas for strategic reallocation or redesign.

Once financial clarity is established, the next step is to review improvement potential by assessing demand, patient needs, market opportunities and performance gaps. This holistic perspective allows organisations to determine which service lines should be repositioned, reinvested in or discontinued. Making these data-driven decisions ensures that brand equity is preserved while strengthening the hospital’s long-term market position.

Some further steps healthcare providers can take to improve care delivery include:

1. Strengthening revenue streams

- Enhancing scheduling, patient experience and follow-up processes to improve patient throughput

- Addressing inefficiencies in internal and external referrals to reduce patient leakage and improve resource utilisation

- Reviewing physician incentives to align with quality, productivity and patient experience objectives

2. Optimising resource allocation

- Assessing potential volume reallocation, specialisation and efficiency improvements

- Optimising theatre utilisation, reducing average surgical times and shifting minor surgeries to procedure rooms to enhance efficiency.

- Improving inpatient ward organisation through better coordination with operating theatre and admissions teams, aligning staffing levels with demand, and actively managing patient length of stay.

Care support

Beyond clinical operations, optimising administrative and support functions is essential to reducing inefficiencies and reallocating resources effectively. A zero-based budgeting (ZBB) review provides a structured approach to evaluating support services from the ground up. This method helps eliminate redundant processes, redeploy staff and identify opportunities for outsourcing non-core functions.

A ZBB review should address key questions such as:

- Are we doing the right thing?

- Are we using the right resources?

- Do we need to evolve our ways of working and care models?

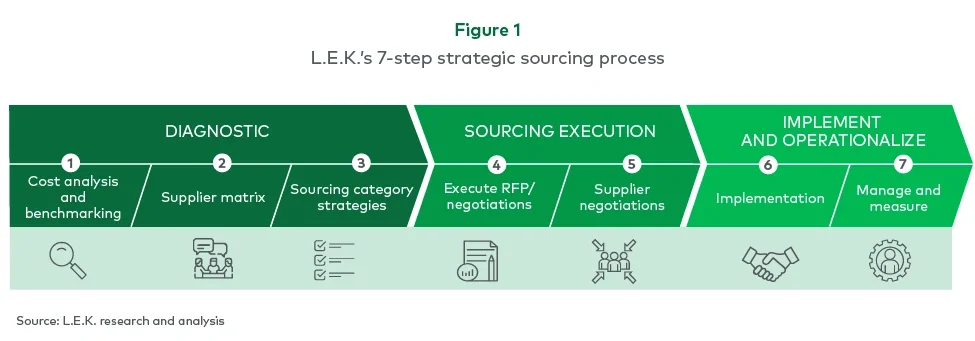

By systematically reviewing these areas, organisations can streamline administrative tasks, increase utilisation of critical staff and reduce non-value-adding expenses (see Figure 1).