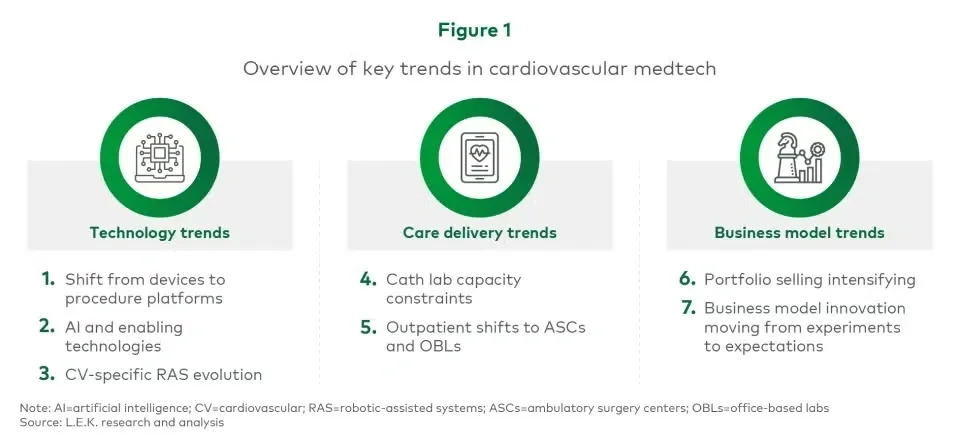

Technology trends

1. Imaging-therapy convergence is accelerating the shift from devices to procedure platforms

CV is moving toward a model where imaging is inseparable from intervention. The world of a preprocedure diagnostic procedure or step is evolving into real-time integrated imaging guidance that can help determine therapy choice, device size and procedural endpoints.

This is evident in structural heart imaging with an explosion of preprocedural diagnostic imaging, screening and planning software as well as visible within structural heart, coronary and peripheral vascular intraprocedural imaging (e.g., 3D intracardiac echocardiography, intravascular ultrasound (IVUS), intravascular optical coherence tomography (OCT)), physiological assessment and navigation tools increasingly defining procedural quality and optimizing cath lab capacity/procedure time.

Imaging innovation is driven by increasing clinical complexity and precision requirements, economic pressure to reduce complications and lengths of stay, and demand for reproducible results. As a result of imaging advancements, competitive differentiation is shifting from single-product superiority to end-to-end procedural ecosystems (i.e., planning, guidance, therapy, verification, follow-up). Winners will be players that can integrate imaging, software and therapy into a simple, repeatable workflow that improves both outcomes and throughput.

2. Artificial intelligence (AI) and enabling technologies will help reshape clinical decisions, lab throughput and commercialization

AI’s first wave in CV focused on image segmentation and interpretation. The next wave is likely more operationally disruptive: AI as a workflow orchestrator and procedural copilot, spanning scheduling optimization, case triage, automated reporting, complication prediction and intraprocedural decision support. The impact of AI is most likely to be felt in cath lab productivity increases, procedural guidance (i.e., device selection) and chronic management (e.g., remote monitoring, predictive alerts).

Winners in AI will need access to high-quality data at scale, integration into clinical workflows and regulatory/provider trust. Integrating AI into solutions has the potential to help accelerate the shift from transactional selling to recurring revenue models. While monetizing AI add-ons is a constant question, the decision to not integrate AI into offerings may have bigger consequences as the market rapidly evolves.

3. CV-specific robotic-assisted systems (RAS) will move from “nice to have” to an operational lever, if economics and workflow are solved

RAS in CV settings are advancing, with multiple strategics shifting focus from an early adoption phase to a future scaling phase, driven by the promise of precision, standardization and occupational health benefits (notably radiation reduction and ergonomic improvements). The long-term vision of remote or distributed expertise remains compelling, but near-term value will be determined by pragmatic workflow and ROI.

Manufacturers must solve the challenges around workflow integration (reduced cognitive load and procedure time), utilization (sufficient case volume) and interoperability. There are numerous RAS players interested in the CV market, as well as CV players interested in bringing RAS into the cath lab. The technical challenges will be solved, and the future opportunity is up for grabs.

RAS are likely to become part of broader digital cath lab modernization programs. Device companies should treat robotics less as a discrete category and more as a capability embedded into integrated solutions — potentially paired with AI-driven navigation, imaging guidance and standardized procedure playbooks.

Care delivery trends

4. Cath lab capacity is becoming a binding constraint — and a major source of competitive advantage

Demand continues to rise (aging populations, broader indications, improved diagnostics) and case complexity is increasing, while cath lab capacity faces pressure from staffing supply shortages (across interventional cardiologists, electrophysiologists, technicians, nurses), increased documentation burdens and increased operational expectations (e.g., room turnover).

Winners will deliver throughput improvement through workflow automation, procedure standardization and reduced complications, winning a disproportionate share by becoming a partner to constrained providers.

5. Outpatient shift: Ambulatory surgery centers (ASCs) and office-based labs (OBLs) are becoming strategic battlegrounds — now expanding into more complex CV and electrophysiology

Economic pressure from payers and health systems is steadily moving cases away from inpatient settings (e.g., the recent approval of cardiac ablation in ASCs). ASCs and OBLs are both highly important in this shift in care setting. Different settings create new call points that have unique purchasing criteria and are starting from scratch in terms of capital equipment. Manufacturers need to be ready with a playbook and sales team to cater to the needs of these new sites of care or risk falling behind. This includes:

- ASC-/OBL-specific product configurations and service bundles

- Simplified training and credentialing support

- Per-case pricing options and risk sharing tied to complications or reinterventions

- Dedicated evidence that speaks to outpatient endpoints: time, discharge readiness, readmission and total cost

Business model trends

6. Portfolio selling in CV will intensify as providers buy pathways, not products

Health system consolidation, procedure complexity and integrated service lines are pushing CV procurement toward portfolio decisions. Providers increasingly prefer fewer strategic vendors that can cover a broad share of cases with consistent workflows, data integration and contracting simplicity as long as it does not compromise clinical outcomes or clinician satisfaction.

Vascular provides an earlier example in terms of offering a range of vessel visualization modalities (e.g., IVUS, OCT), vessel preparation devices (e.g., intravascular lithotripsy, specialty balloons, atherectomy) and treatment options (e.g., balloon vs. scaffold, drug-eluting bioresorbable stents vs. drug-eluting stents vs. bare-metal stents, drug-coated balloons vs. plain-old balloons).

Winners will craft compelling portfolio narratives linked to patient outcomes and efficiency, provide evidence for value analysis committees and integrate services that help operationalize change. Players with narrow portfolios will either need to become indispensable through overwhelming evidence and clinician pull or partner with other players to create a portfolio.

7. Business model innovation: Pricing, risk sharing and recurring revenue will move from experimentation to expectation

Traditional per-unit pricing is increasingly misaligned with provider economics — particularly in outpatient settings and under-bundled payment dynamics. Acceleration in alternative pricing models is expected:

- Per-procedure pricing that bundles disposables, software and service

- Subscription-as-a-service models for software, analytics and workflow tools

- Outcome-linked arrangements (e.g., warranties, complication guarantees, reintervention-linked rebates)

- Managed services for capital equipment and lab operation support with or without minimum device utilizations

To avoid margin erosion, companies must build pricing architectures that tie to measurable value — throughput, complication reduction, readmissions and total episode cost — supported by data and credible analytics.

Critical activities to stay ahead of key trends

With a number of critical trends shaping the CV industry, there are a number of key steps manufacturers can take to best position their portfolios for success:

- Reframe strategy around procedures and sites of care: Define where you will win (inpatient, ASC, OBL) and tailor offerings accordingly to prioritize consistently predictable and efficient procedures for at-capacity customers.

- Build a portfolio narrative with evidence: Not just clinical superiority but economic proof tied to outcomes and operational impact from leveraging the comprehensive portfolio.

- Leverage strategic M&A to supplement core capabilities: Capture meaningful innovation from startups through early partnering and incubation, disciplined M&A and thoughtful integration.

- Invest in the workflow layer: Data, AI, integration and services that unlock cath lab throughput and standardization.

In short, the CV industry is transitioning from a product arms race to a platform-and-economics competition. The next era will reward organizations that can converge imaging, therapy, AI and service into repeatable procedure success — delivered wherever the patient is treated, increasingly outside the hospital.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC