U.S. specialty chemicals companies entered 2026 facing a more disciplined and selective operating environment. Against a backdrop of uneven volume growth and margin pressure in the broader chemical market, specialty players remain comparatively resilient due to differentiated products and exposure to higher-value end markets. At the same time, specialty chemicals firms are navigating four important trends:

- Persistent supply chain complexity

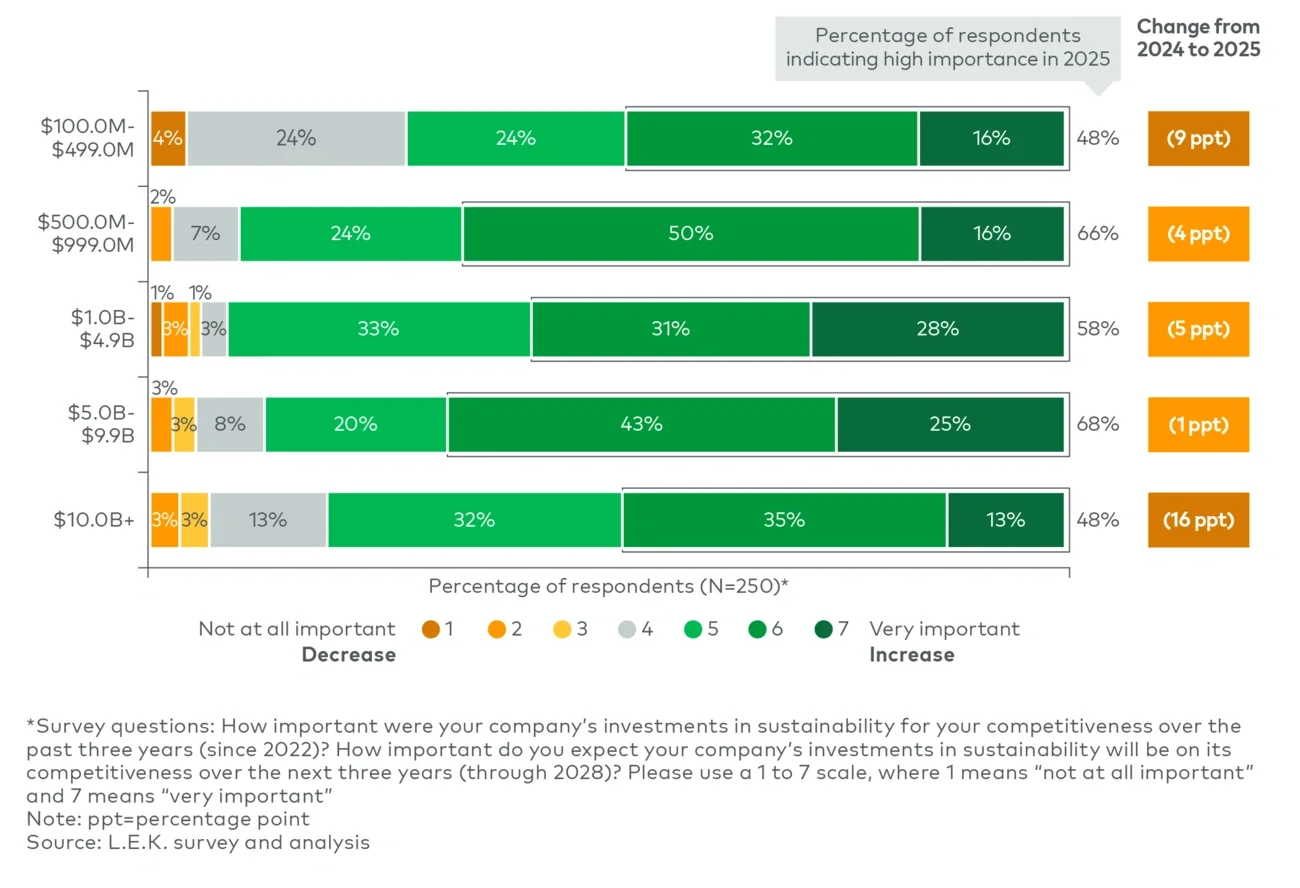

- Evolving sustainability and safety considerations

- Ongoing digital transformation

- Rising labor constraints

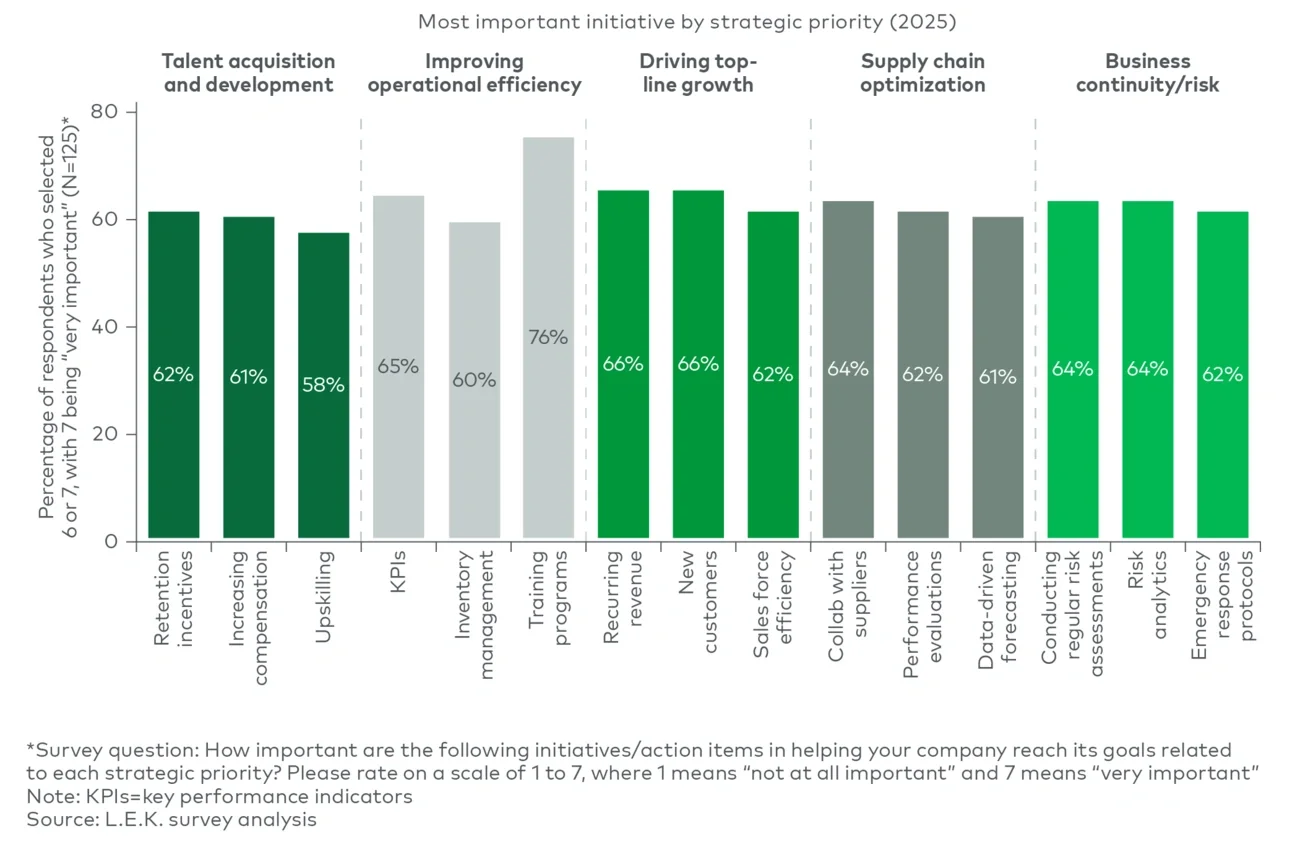

In this edition of L.E.K. Consulting’s Executive Insights, we take a closer look at each of these trends and how they’re influencing specialty chemicals executives’ strategic priorities and investments. Along the way, we highlight quantitative findings from our latest U.S. Specialty Chemicals Executive Survey to provide a clearer picture of where the industry stands as companies position themselves for the next phase of growth.

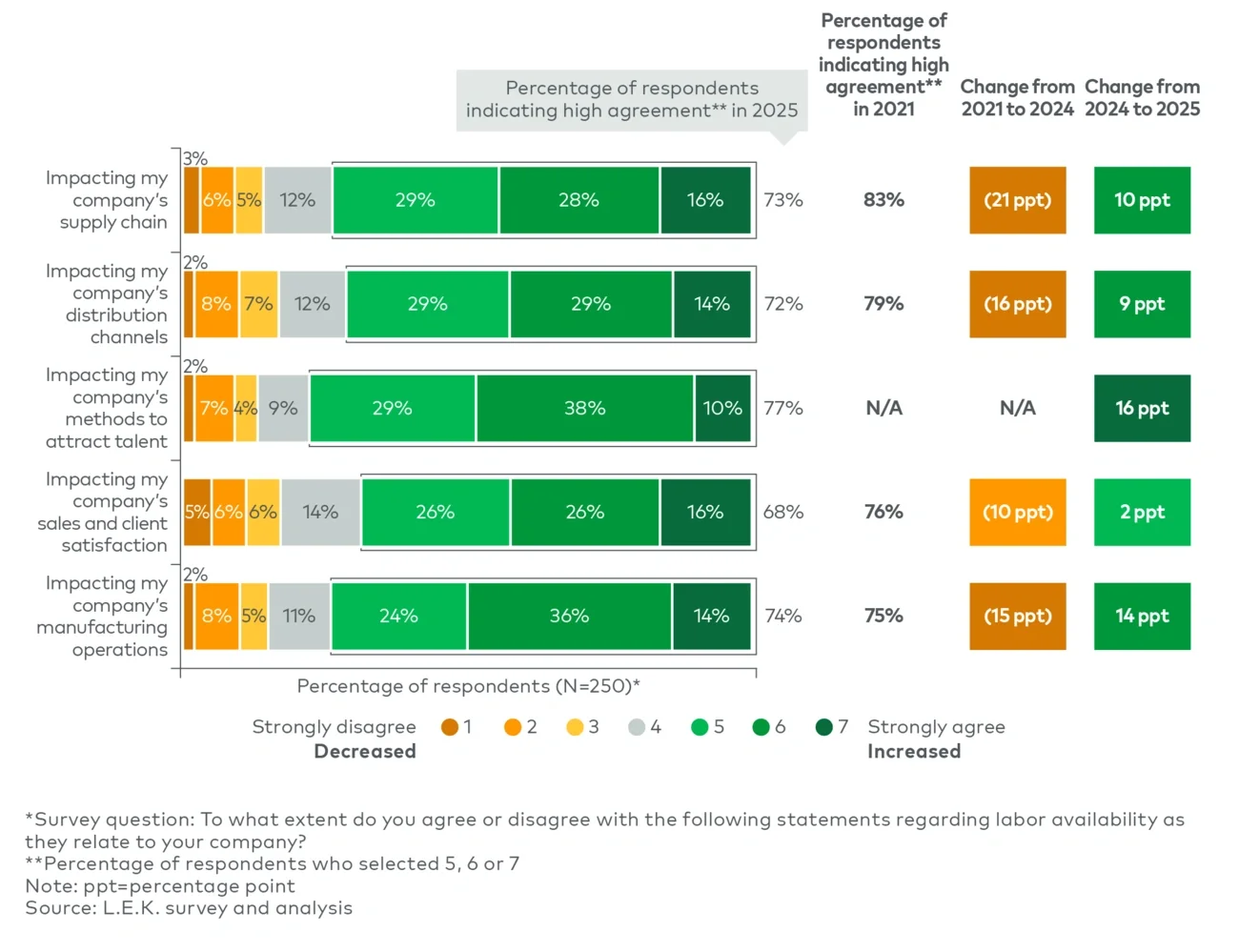

1. Supply chain and distribution strategies are becoming more targeted

Supply chain stability remains a central focus for specialty chemicals companies as they refine their strategies following several years of pressure. While supply and demand have largely rebalanced across chemicals supply chains, executives remain focused on shoring up reliability and mitigating risk.

Many companies have acted to reduce supplier risk in recent years. Now that supply chains have normalized somewhat, chemical industry executives are taking fewer mitigation measures. This shift reflects the distinction between measures taken during periods of heightened disruption and the needs companies prioritize in a more stable environment (see Figure 1).