Warehouse execution systems (WES) are becoming more sophisticated, featuring better interface and integration with warehouse management system layers as multisystem warehouses become harder to manage through rules-based control alone. AI is increasingly part of the same story, with nearly half of operators rating it as highly important to warehouse automation investment. The primary use cases for AI in this context are centered on forecasting, knowledge support, warehouse planning and demand prediction.

As the warehouse automation space evolves, investment is not moving away from hardware. Instead, it is moving toward the orchestration layer, which makes existing hardware more productive and selectively pulls through additional robotics. With operators moving from isolated automation purchases to interconnected systems, value migrates toward the layer that can coordinate people, equipment and decisions in real time. Consequently, in warehouse automation, a growing margin pool is expected to sit less in the most visible machine and more in the intelligence wrapped around it.

Integrators play a central role in ROI delivery

As warehouse automation investment grows in complexity, system integrators have emerged as the primary purchase channel, providing the expertise across hardware and software that drives measurable returns. Rather than purchasing discrete components, operators increasingly seek end-to-end solutions tailored to the physical and operational realities of their facilities, with integrators helping navigate trade-offs between near-term disruption and long-term efficiency gains.

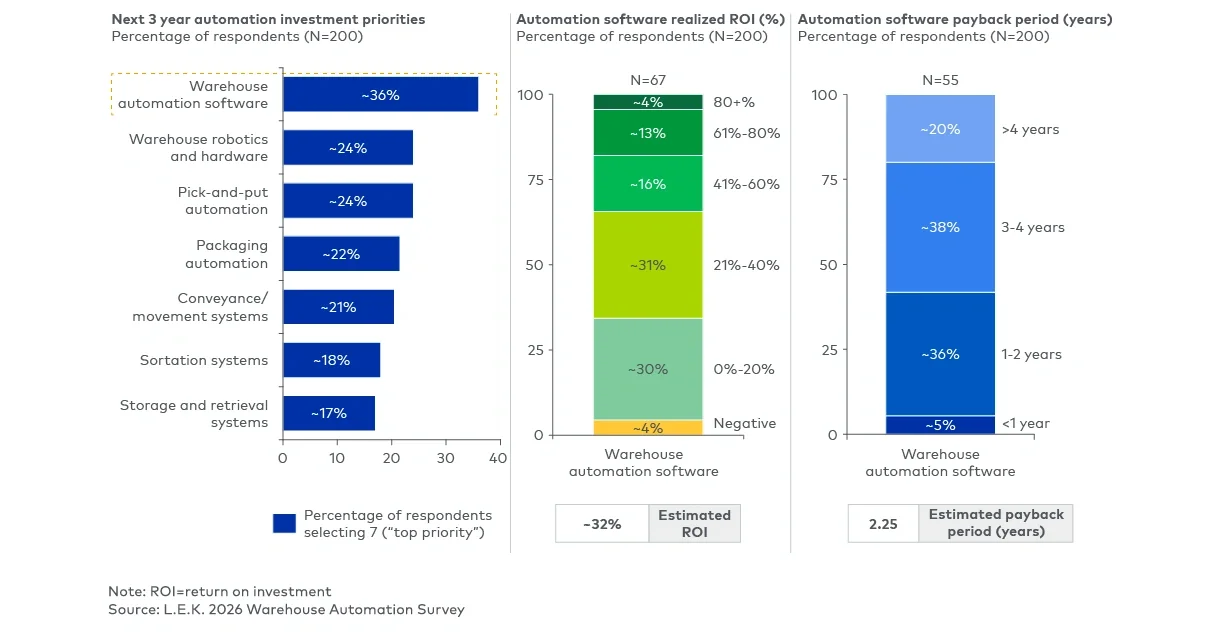

Effective integrators are shifting from hardware-led integration to software-driven orchestration to drive service differentiation and margin, placing added focus on the ability to develop or access complementary technology capabilities. When done well, the results are compelling: More than 80% of warehouse operators report automation payback periods under two years, with approximately 20%-40% ROI driven by labor savings, throughput gains, damage reduction and lower operating costs. As a result, integrator use is expected to expand, making it one of several durable, high-value entry points for automation investors.

Warehouse automation offers diverse value creation opportunities

U.S. warehouse automation is growing and increasingly has multiple vectors for investment. Operators are not only turning toward new scaled facility build-out but also prioritizing brownfield modernization, software-led orchestration and high-ROI upgrades inside the installed base. They are concentrating their efforts first on large throughput-critical nodes, then expanding into smaller facilities as technologies become easier to deploy. And they are favoring the partner that can make heterogeneous systems work together reliably. In a market still early in its penetration curve, structural growth and favorable value capture are beginning to converge.

At L.E.K., we support warehouse automation stakeholders across the value chain as they navigate their most pressing challenges. Our experts bring proprietary perspectives on investable opportunities and operational due diligence, identifying stress points and inefficiencies in existing models in order to deliver tangible cost savings and productivity improvements.

Please contact us for more information.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC