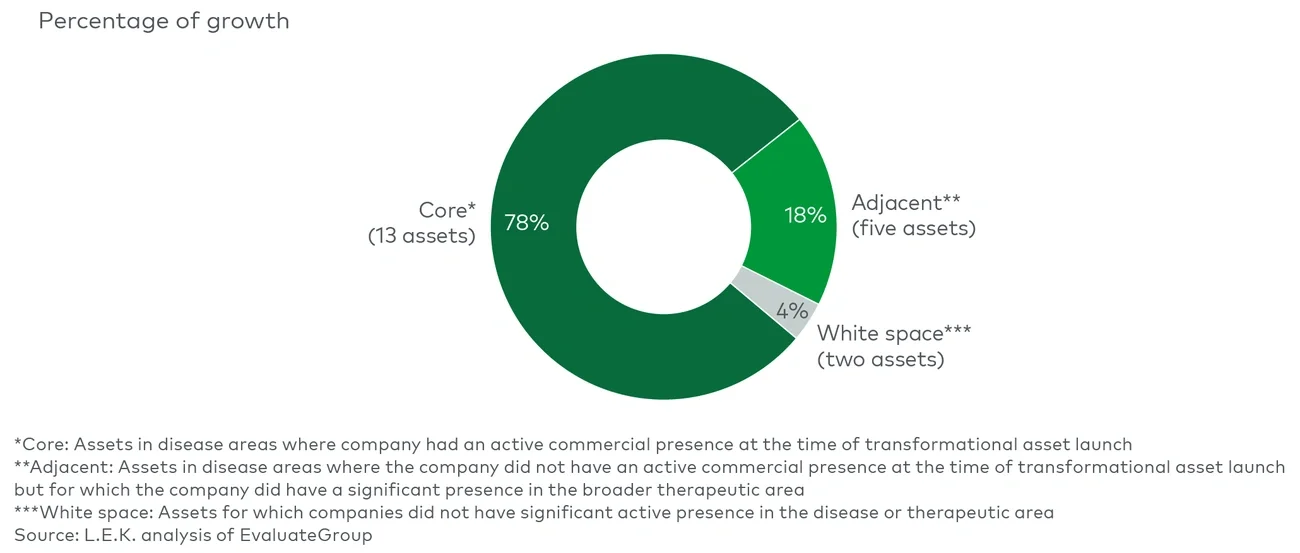

This concentration reflects the compounding advantages of building from the core: established science, mature commercial infrastructure, deep physician relationships and hard-won payer access. Yet there is a natural ceiling to how far such concentration can be extended. Success in any therapeutic or disease area inevitably attracts new entrants, intensifying competition and gradually eroding the differentiation that made the core attractive in the first place. The strategic implication is a dual imperative: Companies must continue to mine and defend their core franchises while simultaneously laying the scientific and commercial foundations to extend into adjacent disease and therapeutic areas. Those that manage this balance effectively will be best positioned to generate above-market growth across the decade.

2. Build leadership in novel therapeutic paradigms

Even a disciplined core-and-adjacent strategy has limits when the underlying science matures. In categories where dominant mechanisms are well understood and standards of care are largely set, incremental innovation often does not produce transformational economics, and later entrants often compete on the margins.

The industry’s most transformational assets have not always emerged from its most active markets. The assets are often the product of scientific frontiers and DAs the broader industry had yet to fully appreciate — developed by companies willing to enter DAs ahead of the field or those where breakthrough innovation had stalled, and in some cases these companies reimagined the commercial model entirely. For example, Novo Nordisk invested heavily in obesity biology years before GLP-1 therapies evolved into one of the industry’s largest commercial categories. Similarly, Regeneron and Sanofi expanded the Dupixent franchise across multiple type 2 inflammatory diseases by leveraging a shared underlying biological pathway and overlapping physician call points.

These companies do not simply follow the science; they shape it. By assuming early risk in areas of compelling biology and significant unmet need, they define standards of care and establish category leadership years before competitors can meaningfully respond — converting first-mover advantage into a structural position that followers can spend years trying to close.

The implication is clear: Disproportionate long-term returns require more than optimizing the existing portfolio. They require selective, courageous bets on novel therapeutic paradigms placed early enough to shape the market, not just participate in it.

3. Align capital and organization behind conviction

Portfolio strategy creates the conditions for success, but conviction determines whether breakout opportunities ultimately realize their potential. In large pharmaceutical organizations, transformative assets rarely advance on data alone; they require senior leaders willing to champion them before the evidence is fully established and sustain support through scientific uncertainty, development setbacks and competing portfolio pressures.

This challenge is especially acute for opportunities outside the company’s historical core. Leaders are often forced to choose between a higher-risk asset with transformative potential and lower-risk smaller investments with more predictable outcomes. Capturing breakout opportunities therefore requires a willingness to make and sustain difficult trade-offs over multiple years.

When a genuine breakout opportunity emerges, investment levels must match the scale of the ambition rather than the asset’s stage of development. That often means allocating disproportionate resources, accelerating capability building and deprioritizing other parts of the portfolio to create room. Companies that apply standard resource-allocation approaches to exceptional opportunities frequently constrain their upside before the opportunity has fully developed.

The ability to reposition early as science evolves is equally important. Merck’s transformation around Keytruda illustrates the point. In 2011, oncology represented less than 3% of company revenue⁶ and Keytruda had no late-stage trials. Within five years, however, the asset accounted for 40% of Merck’s phase 2 and 3 trials.⁷ Achieving that shift required far more than reallocating capital; it required building new capabilities, making explicit trade-offs across the portfolio and sustaining organizational commitment years before the commercial opportunity was fully validated.

Beyond the portfolio

For large biopharma companies facing a widening growth gap, the challenge is not simply one of portfolio composition. While getting the portfolio “geometry” right is an important first step, sustaining growth in a dynamic market also requires an operating model capable of reallocating resources toward emerging opportunities and away from subscale assets and increasingly exhausted areas of science. Underpinning both is a culture willing to tolerate risk, back conviction over consensus and support breakout opportunities through uncertainty.

Executing this shift is inherently difficult within large pharmaceutical organizations, where entrenched processes, budgeting cycles and competing stakeholder priorities often reinforce the status quo. Meaningful change therefore requires sustained sponsorship from the C-suite, not only to reshape the portfolio but also to rethink how capital, talent and organizational attention are allocated across the business.

The companies best positioned to capture the next generation of transformational assets are unlikely to be those with the broadest pipelines, but those most capable of concentrating resources behind a small number of differentiated opportunities and adapting as the science evolves. In an increasingly crowded industry, competitive advantage will come less from participating in the same high-growth categories as peers and more from identifying and scaling emerging opportunities earlier than the rest of the market.

For more information, please contact us.

The authors would like to thank Izzy Wilson for her contributions to this article.

Note: AI was used in the drafting of this piece

Endnotes

¹Based on 2025 total prescription sales excluding generics and biosimilars

²L.E.K. analysis of EvaluateGroup

³L.E.K. analysis of EvaluateGroup

⁴L.E.K. analysis of S&P Capital IQ and EvaluateGroup

⁵L.E.K. analysis of company-disclosed 2026 pipelines

⁶L.E.K. analysis of EvaluateGroup

⁷L.E.K. analysis of clinicaltrials.gov

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC