The U.S. youth sports market generates around $40 billion annually. Every year about 30 million athletes participate in tens of millions of organized events, from local leagues to national tournaments. The sector is attractive to investors given its noncyclical demand, recurring revenue and fragmented ownership. Families continue prioritizing participation even during downturns, with about 70% maintaining involvement and roughly 60% viewing sports as essential to development and college readiness.

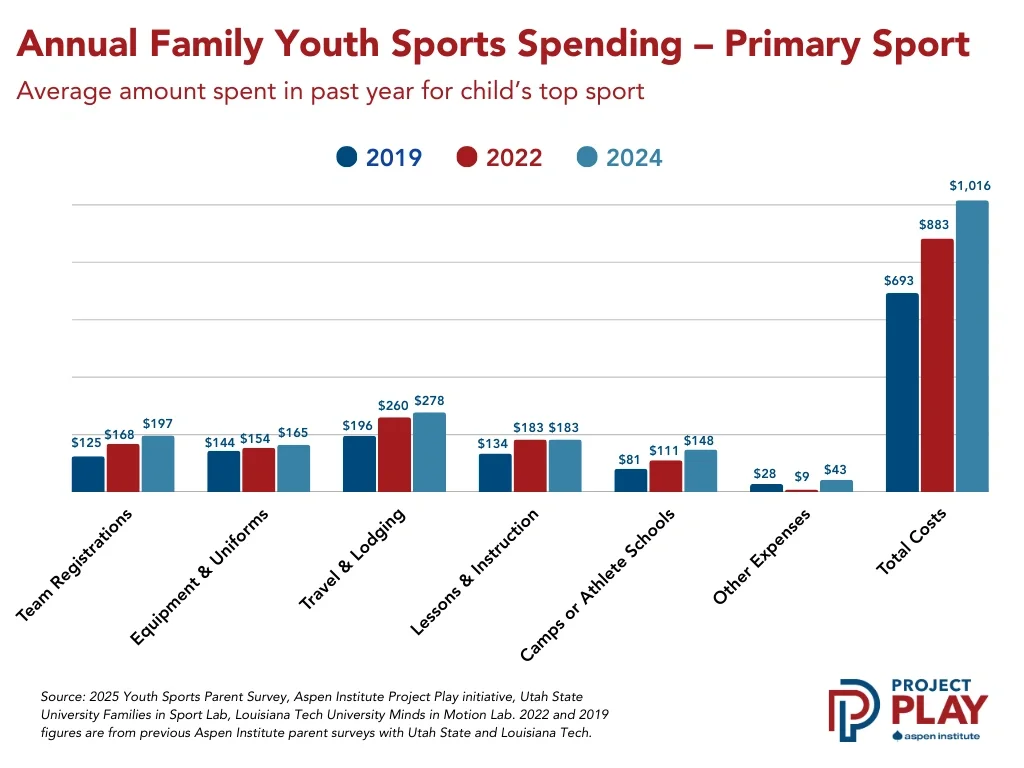

Household spending on youth sports has risen sharply over the past decade. Per-athlete annual spend increased from roughly $700 in 2019 to about $1,000 in 2024 across registration fees, travel and equipment. And about one-third of families now report taking on debt so their kids can participate in sports.

The Most Investable Segments in Youth Sports Going Into 2026

Key takeaways

Youth sports is now a scaled and resilient market, with families maintaining participation through economic downturns and spending rising to roughly $1,000 per athlete.

Physical infrastructure is professionalizing in parallel, with facilities, tournaments and club networks using standardized systems to improve utilization and expand recurring revenue.

Capital is concentrating in youth sports technology, where integrated platforms that unify registration, payments, scheduling and video are emerging as natural entry points into club and league operations.

Building real scale remains difficult because labor-intensive go-to-market dynamics, sport-specific credibility, capital-intensive assets and operational growing pains are limit how quickly platforms can expand.

Image 1.

Open configuration options Average annual spend on child’s primary sport (2019-24)

Participation has fully recovered from pandemic lows. Among ages 6 to 17, team sport participation rose 9% year over year in 2024. Lower-income households have posted notable gains as community programs and post-COVID-19 funding expanded.

This growth is reshaping the industry. What was once volunteer-run recreation has evolved into a year-round professionalized marketplace. Clubs that previously ran seasonal programs now operate like small enterprises, often charging $1,000-$2,000 annually per player before travel costs. Up to 35% of high school athletes now specialize in a single sport, training more than eight months per year. That intensity requires facilities, coaching and competition outside school seasons, making club sports essential infrastructure rather than optional enrichment.

The three-pillar investment framework

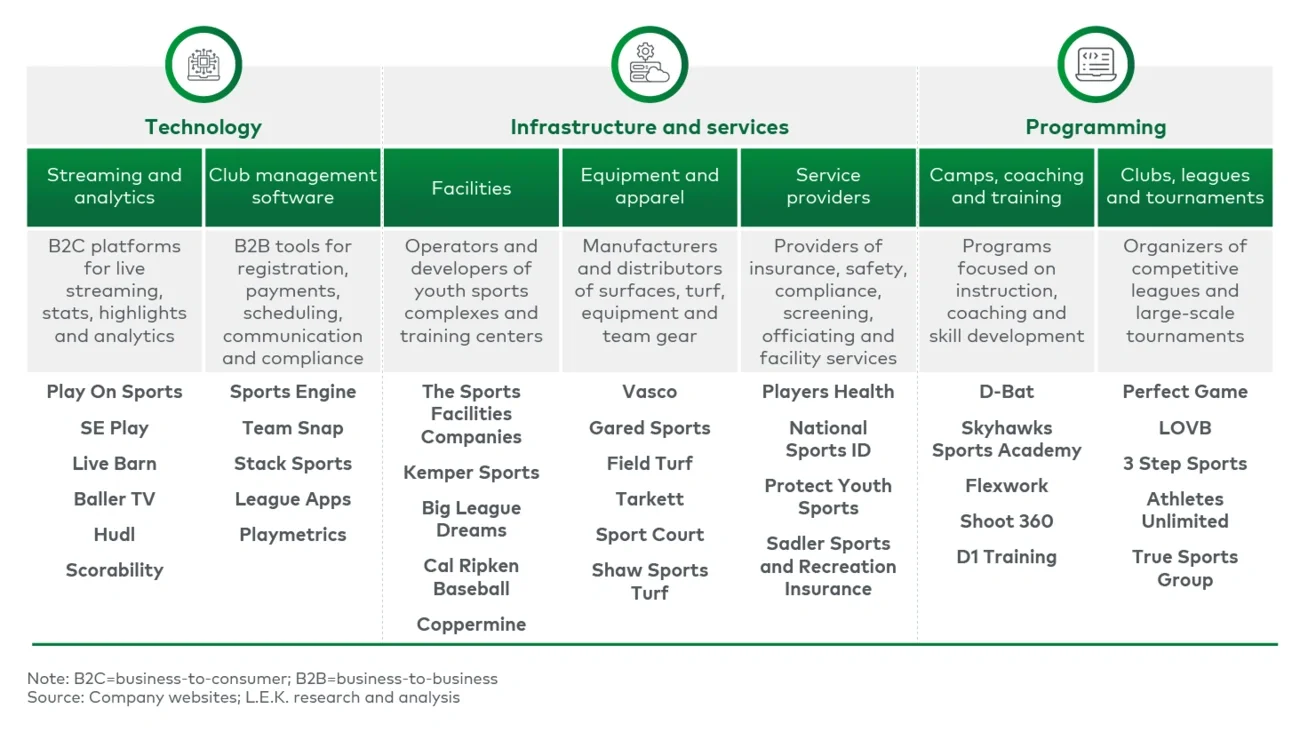

This shift toward professionalized operations has created three investable categories: technology, infrastructure and services, and programming (see Figure 1).

Figure 1.

Overview of investable areas in youth sports

The most defensible businesses combine at least two pillars. Software paired with facilities captures both digital and physical economics. Clubs and leagues that combine programming with merchandising extend monetization beyond the season. Integrated platforms separate scalable businesses from local operators.

Over the past two years, capital has concentrated most heavily in technology.

Digital infrastructure as a natural entry point

Youth sports management platforms support the operational backbone of clubs and leagues: registration, scheduling, payments, team communication and, in many cases, livestreaming or analytics. Their economics blend predictable subscription revenue with payment-volume fees and sponsorship data opportunities.

The market remains fragmented, ranging from established players like Stack Sports and SportsEngine with broad functionality to newer entrants competing on modern design and workflow simplicity. The landscape spans a wide range of platform scope, from focused, sport-specific tools to broader multisport platforms designed to support club and league operations (see Figure 2).

Figure 2.

Youth club management landscape by scope and focus

This fragmentation has begun to drive consolidation. Accel-KKR has backed LeagueApps and ArbiterSports to build end-to-end capabilities across registration, scheduling and officiating. Genstar Capital continues expanding Stack Sports through bolt-on acquisitions that integrate analytics and communication tools.

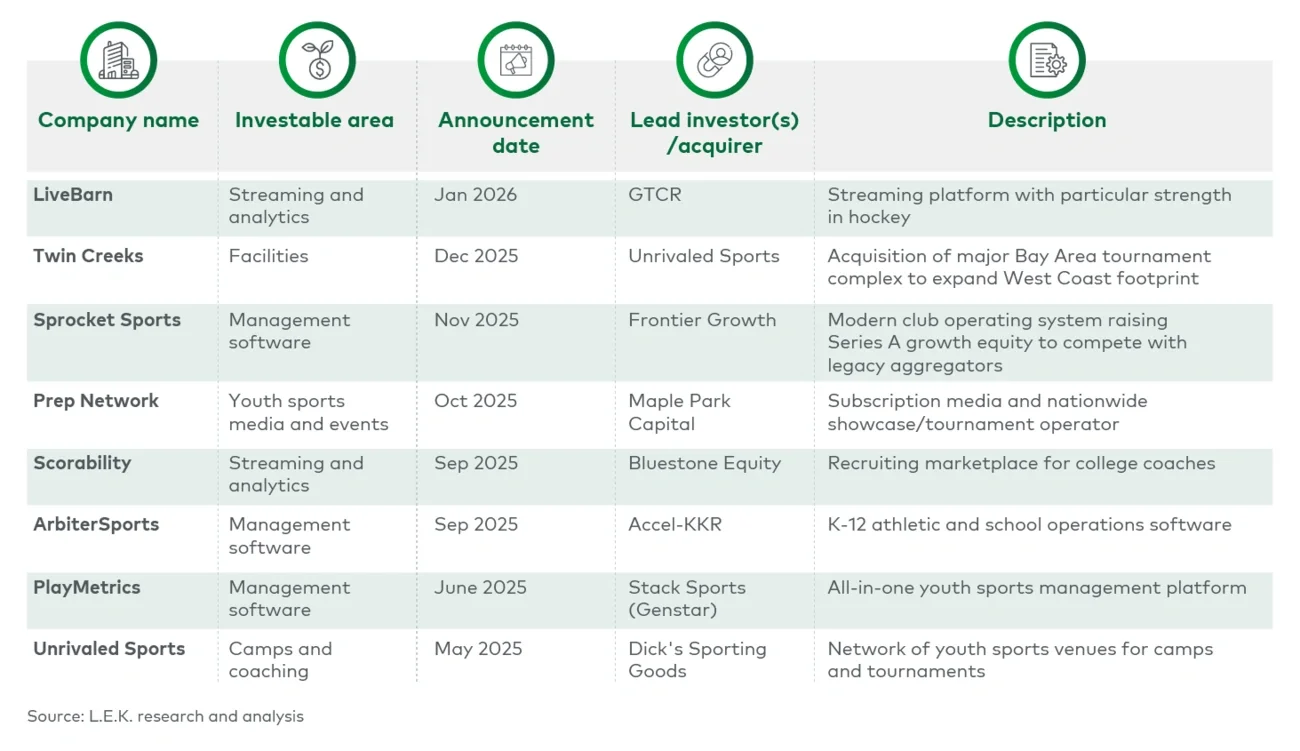

Beyond core management software, investors are increasingly exploring adjacent layers, including livestreaming (Scorability), safety and compliance (Players Health) and media and events (Prep Network), building vertically integrated ecosystems rather than single-product platforms (see Figure 3).

Figure 3, part 1.

Recent private-equity deals in youth sports (2024-26)

Figure 3, part 2.

The direction is clear: Platforms are moving toward true integration, linking payments, video, compliance and facilities through open application programming interfaces. Clubs increasingly expect one-stop solutions. The challenge is execution. Legacy platforms often rely on patchwork acquisitions that create inconsistent interfaces and redundant capability sets. Investors are betting on the next generation of clean, unified systems built around actionable data.

Physical assets follow digital

Capital is also flowing into facilities, tournaments and apparel, tying together the fields where kids play, the systems that run them and the commerce surrounding them. More than $2.5 billion has been invested in new or upgraded youth sports complexes between 2024 and 2026, with operators like The Sports Facilities Companies and Kemper Sports incorporating digital scheduling and registration into their models to maximize utilization.

Consolidators are using the same approach. 3STEP Sports, backed by Juggernaut Capital Partners, operates more than 300 clubs and has acquired operators like Front Range Volleyball Club, standardizing operations across its network. Unrivaled Sports, backed by Dick’s Sporting Goods, manages a portfolio of tournament properties and facilities including Ripken Baseball and Cooperstown All Star Village, using integrated systems to streamline payments and team management.

What makes scale difficult

Strong fundamentals and scalable technology do not guarantee easy execution. As one operator told us, “Everyone likes the underlying trends in youth sports, but it’s harder than it looks to build scale.” Several challenges stand out:

- Fragmented go-to-market: Growth is labor-intensive, with real marginal cost to sell and support thousands of small, distributed clubs, leagues and organizers rather than a centralized buyer base.

- Sport-specific credibility: Relationships, workflows and decision-makers differ by sport, making cross-sport expansion slower and more costly than a traditional software rollout.

- Capital-intensive assets: Facilities and events can generate steady returns but require significant up-front investment and long payback periods unless paired with recurring-revenue layers.

- Execution depth: Many organizations began as grassroots, mission-driven operations. As they scale, professionalized management, tighter processes and integrated systems that don’t disrupt local leadership and culture become increasingly important.

The investment case is clear: structural growth, rising spend per athlete and thousands of fragmented operators. The challenge is building platforms that scale across sports, geographies and business models.

Partner With L.E.K.

Whether you are evaluating a club management platform, exploring growth opportunities in facilities and programming, or developing a portfolio company go-to-market strategy, we bring the data, sector expertise and transactional experience to help you scale what’s next in youth sports.

For support evaluating investments in youth sports, contact L.E.K. Consulting’s Sports and Live Entertainment practice. Co-led by Managing Directors Alex Evans and Geoff McQueen in Los Angeles, this partner-led team works with investors, leagues, teams and service providers across the youth sports ecosystem.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC