Platform economics are earned, not assumed

In consumer health and beauty, the distinction between a collection of manufacturing assets and a fully functioning contract development and manufacturing organisation (CDMO) platform is a primary determinant of value. Investors may value asset collections at 8–12x EBITDA multiples, while fully integrated platforms can command 15–20x EBITDA multiples or more. The gap reflects more than perception. It reflects differences in operating model, commercial integration and the ability to generate repeatable value

A platform is not defined by the number of sites it owns. It is defined by its ability to route customers, data and capabilities across those sites through a coordinated commercial and operational infrastructure. By contrast, a portfolio aggregates assets under common ownership but leaves them largely independent.

The practical question for investors is therefore straightforward: can the business operate as a single system rather than a collection of parts? The answer determines whether platform economics are real and whether valuation premiums are justified.

The platform test: Commercial integration, visibility and control

A CDMO platform combines local specialist capabilities with a centralised operating spine. This distinction is particularly important in consumer health and beauty, where customer fragmentation, stock-keeping unit complexity and speed-to-market requirements are higher than in traditional pharmaceutical outsourcing.

Three conditions determine whether a platform model is functioning effectively.

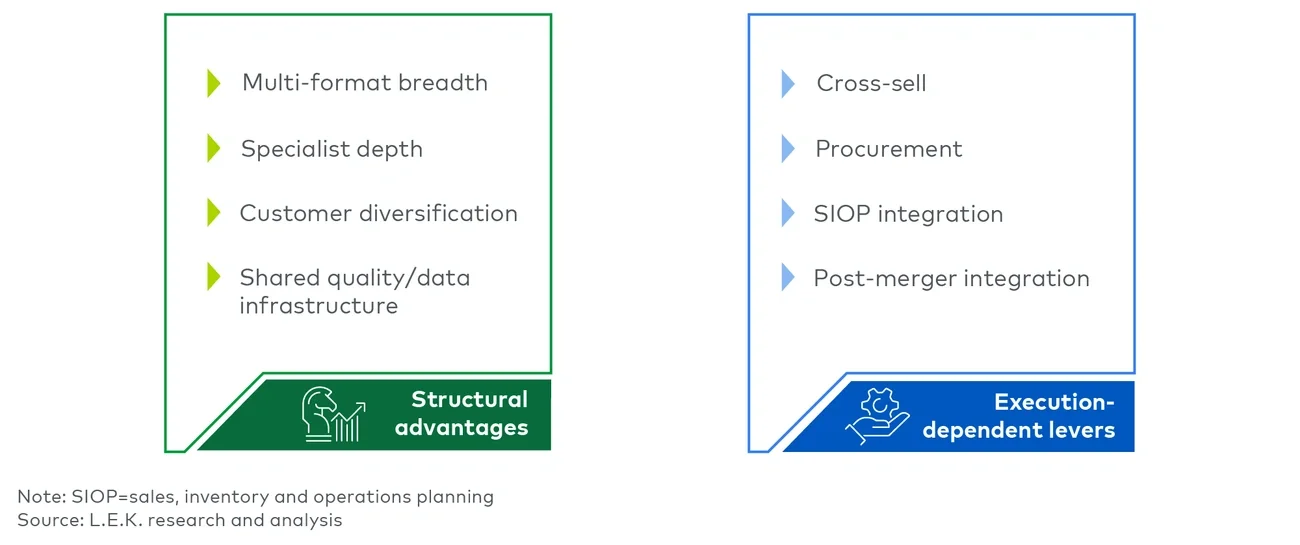

First, commercial integration must enable customers to buy across formats through a single relationship. Where sales teams remain siloed by site, cross-selling remains aspirational rather than embedded in the operating model. Evidence of multi-site customers and increasing wallet share is therefore a critical indicator of platform maturity.

Second, the central team must have sufficient visibility into performance to manage the business actively. This includes timely and granular insight into margins, utilisation, working capital and pipeline. Without this, scale introduces complexity without sufficient control.

Third, the platform must capture economic benefits from scale without weakening local responsiveness. In this sector, customer intimacy and technical agility are often decisive. Over-centralisation can undermine both, limiting the very advantages the platform is intended to create.

Failure in any one of these dimensions typically prevents platform economics from fully materialising.

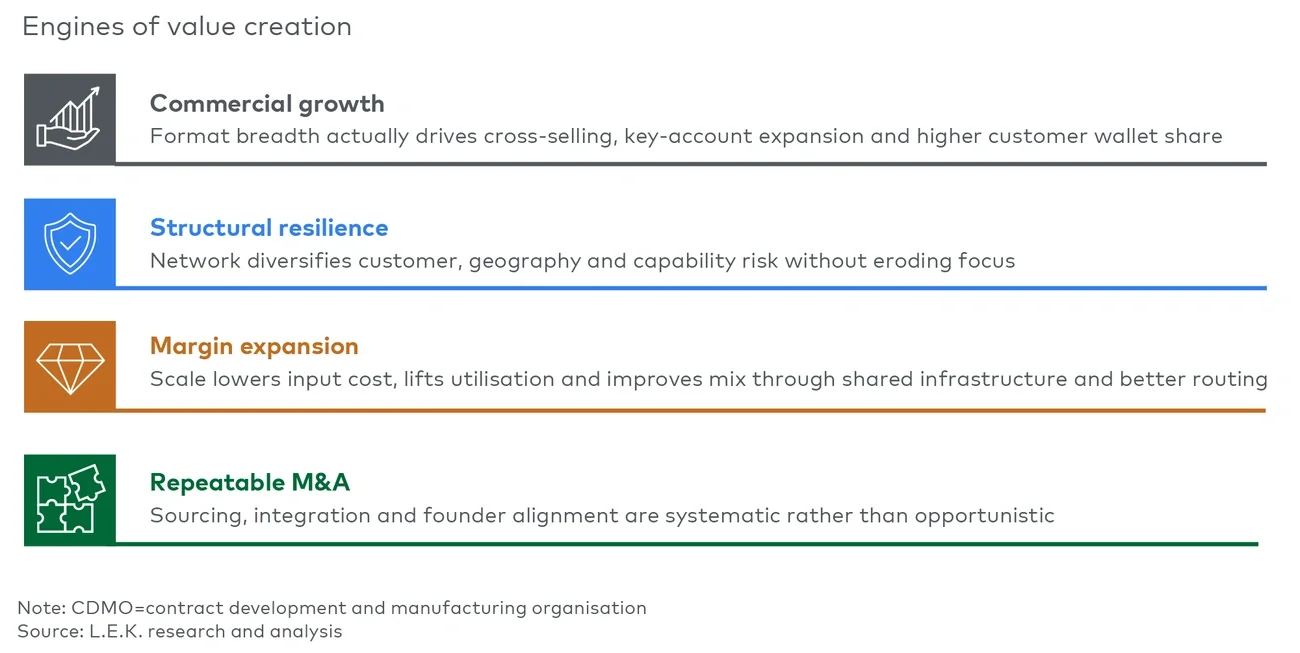

Four engines of value creation

Our analysis identifies four primary engines through which CDMO platforms create value: commercial growth, structural resilience, margin expansion and repeatable M&A (see Figure 1).