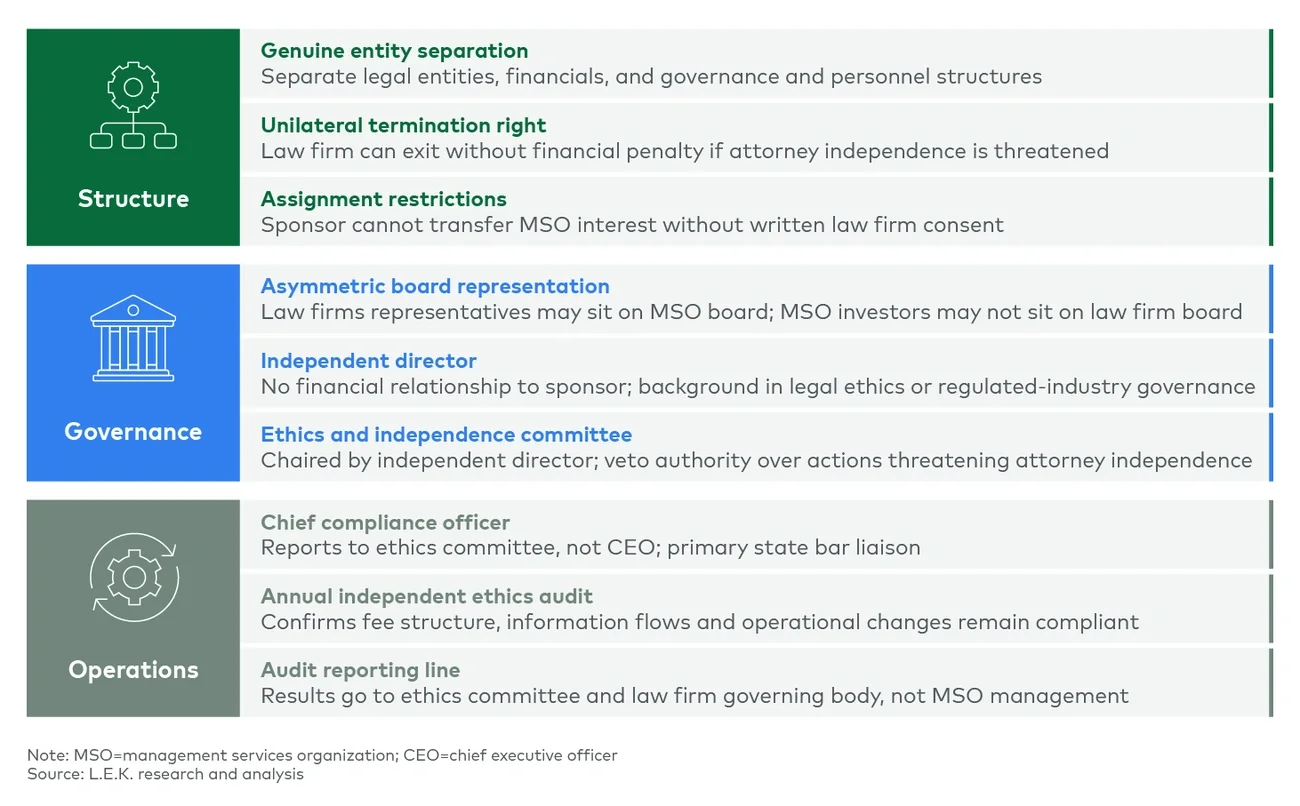

Recent regulatory developments, including Texas Ethics Opinion 706, California AB 931 and Colorado HB26-1421, have given firms and investors a clearer compliance blueprint for deploying capital into law firms via an MSO, and capital has flowed into the space. Industry reports indicate as many as 70 MSO transactions are currently under discussion, drawing in both law firms looking to restructure and investors looking to put capital to work.

Part 1 of this series established the mechanics of the legal MSO. Part 2 covered how investors evaluate them. This third installment focuses on building an MSO, walking through the key design decisions a firm and its investors must make to move from concept to a transaction-ready structure.

Define the MSO parameters

An MSO formation may be triggered by an investor approaching a firm or pursued proactively by a law firm seeking initially to build the structure on a smaller scale before bringing in outside capital.

Either way, the formation mechanics are the same: The law firm carves out its administrative, operational and financial support functions into a separate entity (the MSO), leaving all functions that practice law and interact with clients separate (NewCo), and then establishes a clear and compliant pricing mechanism for NewCo to compensate the MSO. This enables investment from a financial sponsor in that entity in exchange for an ownership stake.

How that MSO is designed depends on a set of foundational parameters.

Single firm or platform

A single-firm MSO is designed to optimize operations for one practice indefinitely. A platform MSO is built from the start to absorb additional firms across geographies or practice areas. The two options require meaningfully different approaches: Single-firm MSOs tend to be simpler in scope, with cleaner migration and a fee structure benchmarked to a known cost base, while platform MSOs require more infrastructure from day one to accommodate firms of different sizes and practice areas.

Practice area

Practice area shapes both the functional scope and the fee architecture of the MSO. A personal injury firm building an MSO to scale case volume has fundamentally different infrastructure requirements than a corporate firm building one to modernize its back office, driven by differences in billing models, workflow standardization and marketing dependence. An MSO designed to support multiple practice areas needs to reflect those distinctions from the start.

Geographic scope

Geographic footprint shapes both the regulatory complexity and the scaling potential of the MSO. Single-state operations are simpler to structure, with a more contained regulatory environment. Multistate platforms enable broader scaling through shared services and cross-market expansion but introduce meaningful complexity as state-level rules governing MSO structures, fee arrangements and attorney supervision vary significantly across jurisdictions.

Taken together, these three foundational parameters shape the scope and ambition of the MSO, but the structure ultimately needs to be designed around where it will create value: professionalizing operations and enabling platform scale. How those value creation levers are deployed in practice will be covered in Part 4 of this series.

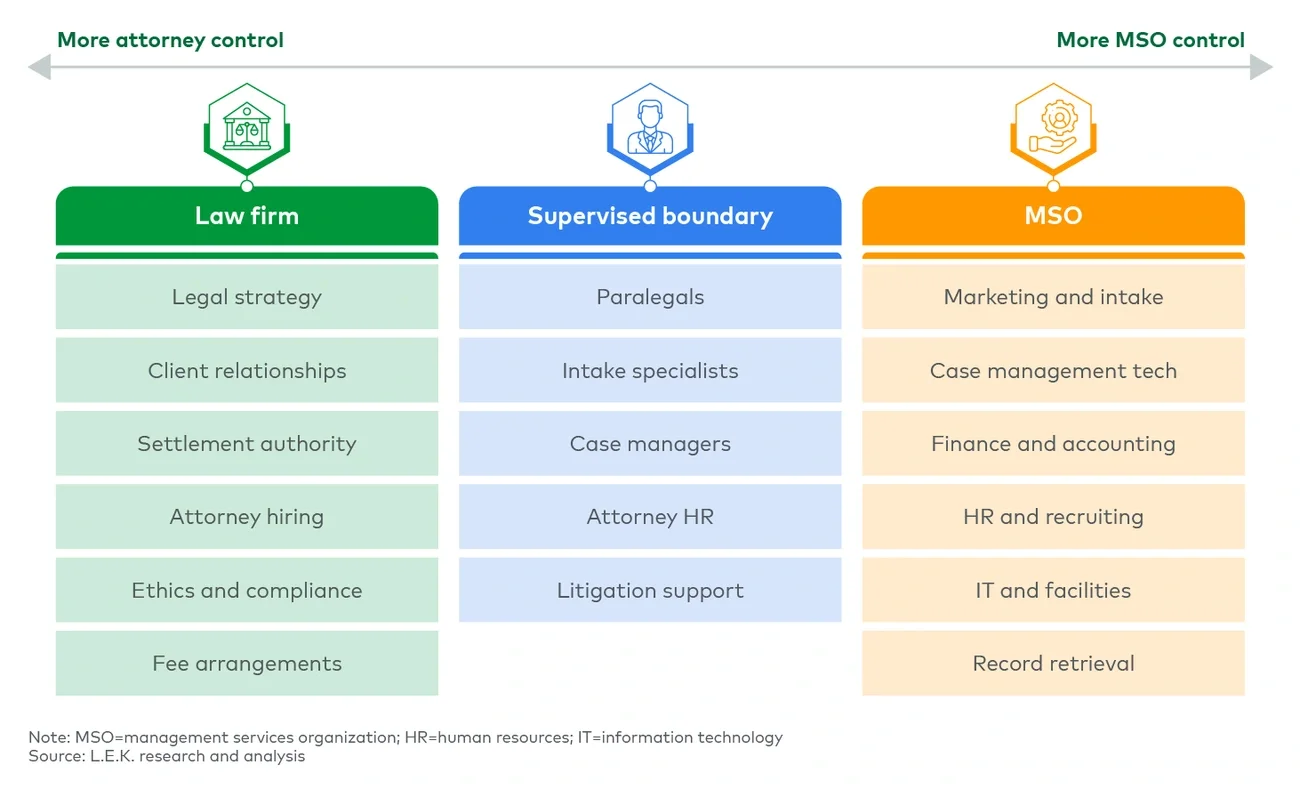

Determine what moves to the MSO and what stays with the law firm

With the MSO parameters set, the firm needs to determine what moves to the MSO and what stays, a question more nuanced than a clean “legal versus business” split.