Related insights

You might also be interested in these insights.

English

Welcome to part four of our series highlighting key findings from the L.E.K. Consulting 2021 Energy Transition Study. In our last article, we relayed what 261 energy executives think their biggest energy transition opportunities are. We’ll continue the discussion now with a look at what oil and gas companies need in order to effectively scale their energy transition programs.

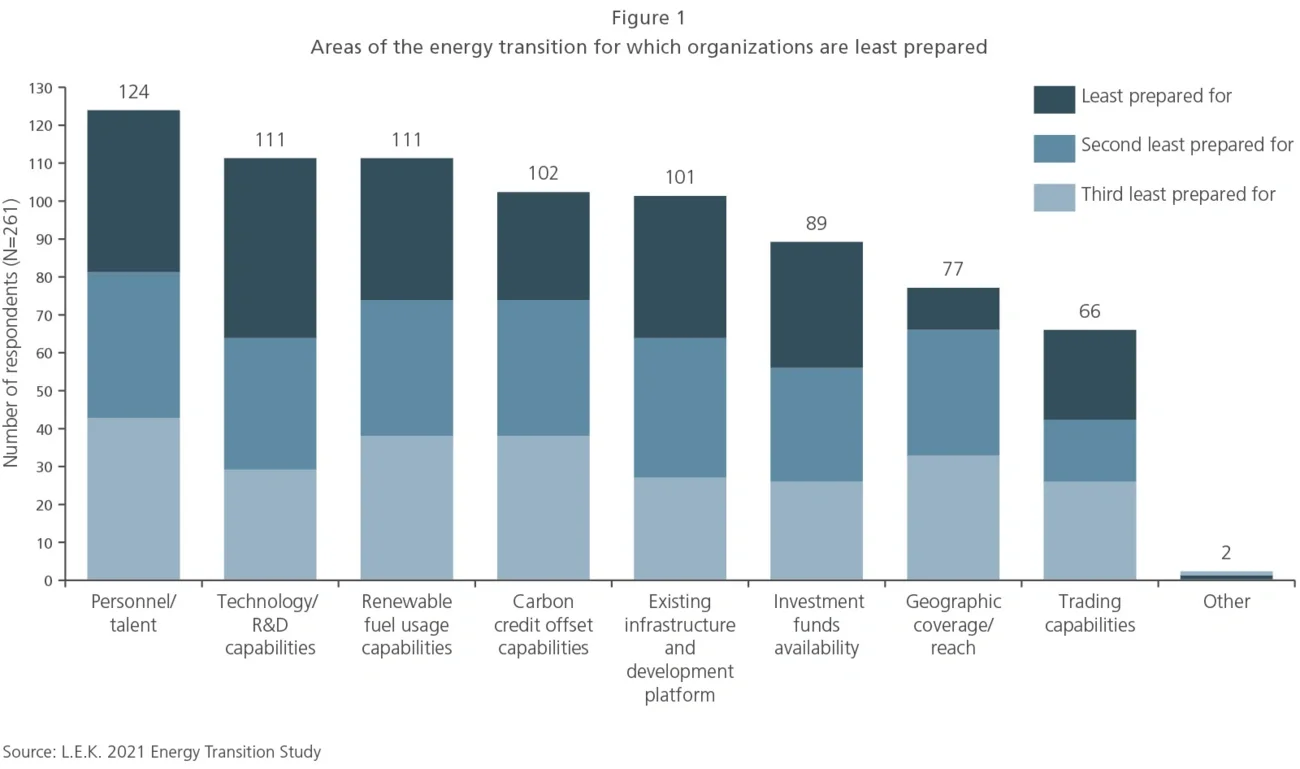

We gave our survey respondents a list of eight energy transition capabilities and asked them to choose the three they believe they’re least prepared for (see Figure 1). Almost half (48%) put personnel or talent in their top three. Technology/research and development (R&D) capabilities tied with renewable fuel end-use for the second-most-popular choice — each landed on the top-three list for 43% of our respondents. These were closely followed by carbon credit offset capabilities and existing infrastructure to support development platforms, both a top choice among 39% of respondents.

Let’s dig deeper into the first two issues — personnel and technology/R&D.

Personnel. The current generation of graduates view oil and gas differently from past generations, with many seeing a conflict with personal values around the societal impact of these industries as well as opportunities for “growth” in new energy technology. Furthermore, the personnel needs of an oil and gas operation vary from new energy transition areas in terms of skill set. Despite oil and gas companies leading capital investment in many of the emerging new low-carbon solutions, the aforementioned perception by the current generation of graduates and skills misalignment are creating challenges in recruiting and retaining top talent.

Technology/R&D. Oil and gas companies are technology companies that, for decades, have innovated engineering solutions to extract resources from miles below the surface. However, two elements of technology and R&D are making the energy transition difficult. First is picking (and timing) the winners, and the other is capability mismatches. For oil and gas companies with large R&D budgets, the big question still remains how to allocate the research and development across myriad energy transition solutions. Adding to the challenge is that many energy transition solutions are too far outside of a company’s R&D capability.

That said, the priorities shift by segment. They break down this way:

As it happens, survey respondents indicate similar capability gaps related to their sustainability initiatives and environmental, social and governance (ESG) goals. We haven’t talked about sustainability and ESG so far, focusing on energy transition initiatives instead. That will change in our next article, so stay tuned.

Here’s the latest in our series of articles on findings from the L.E.K. Consulting 2021 Energy Transition study. Last time, we looked at the kinds of energy transition investments that companies along the oil and gas value chain are making today and are expected to make in the future. What we didn’t discuss was which ones they believe would offer the greatest opportunity for the industry. Let’s touch on that briefly.

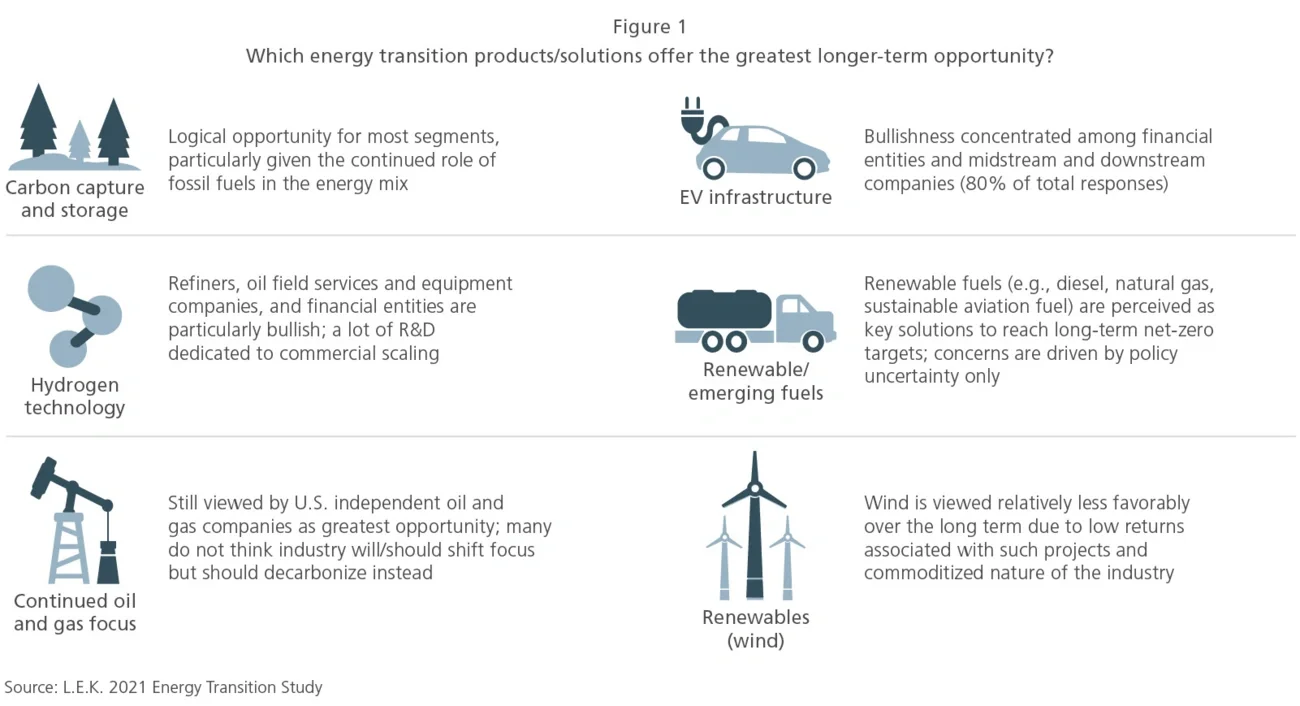

In our study, we asked 261 energy executives where they think the biggest energy transition opportunities are for the industry. More specifically, we asked them to rank their top three energy transition developments in order of opportunity potential.

Carbon capture utilization and storage (CCUS) comes out on top, with 54% of respondents choosing this development. “We’ll be managing these [oil and gas] assets for a long time, so it’s important to reduce their impact on the environment through CCUS,” one executive told us. Next is hydrogen technology, which 46% put on their top-three list despite lingering issues with profitability and whether use cases will be proven out and appear compelling versus alternative technologies vying for similar positioning. A notable example of this is the battle between batteries, hydrogen, liquefied natural gas (LNG) and others for the decarbonization of long-haul transportation. After hydrogen, a third of respondents identify a continued focus on oil and gas, which underpins the industry’s positioning that oil and gas — despite policy and societal headwinds and carbon emissions that can only be abated with the aforementioned CCUS technology — remains an enormous opportunity for the industry even over the long term. While undoubtedly true in the short term in a tight supply, and surging demand, market for oil and gas that is pushing commodity prices ever higher, the pace of transitionary technology development may shape the true answer to this over time.

There’s less consensus around the next group of picks. Electric vehicle (EV) infrastructure is a top choice for 30% of our respondents — nearly tied with renewable and emerging fuels. Both reflect an emphasis on innovation — and perhaps energy portfolio risk mitigation — to manage the transition from traditional fossil fuels. These are followed by solar power, carbon trading and offsets, and battery and energy storage. Wind power garners the least support as a top investment opportunity, with only 17% of executives saying they view it as the biggest energy transition opportunity.

Those are the top-line results. But a look under the hood reveals that not everyone sees every opportunity the same way. An investment that’s a top-three priority must have some impact in the longer term, and that can vary by business (see Figure 1).

This brings us to two important questions: What are the capabilities across talent and technologies that oil and gas executives deem required to capture opportunities in the energy transition? And to what extent do oil and gas companies have these capabilities? We asked respondents about that, too, and we’ll share what they told us in our next article.

The business momentum for sustainability is building, reinforced by the pandemic. Decarbonization is taking on particular urgency.

What sustainability means — and what matters to stakeholders — is evolving and varies by geography and industry. However, one constant is its importance to younger employees.

Uncertainty surrounds the cost of key technologies and whether sustainability will improve financial performance. Even a passive approach to sustainability can require significant change and investment. Meanwhile, what counts as a leading strategy can quickly become table stakes.

The growing consensus around sustainability is creating new opportunities for companies that act now. By taking a structured approach, L.E.K. clients can capture opportunities throughout their value chains and ecosystems.

Partners from the Executive Board of L.E.K.’s Sustainability Centre of Excellence met to talk about what sustainability means across their sectors and regions. The sustainability and environmental, social and governance (ESG) agendas for corporations and investors are evolving apace, with expectations growing and best practice rapidly changing. Businesses are under pressure from a range of stakeholders — including investors, customers, regulators, and often their own boards, leadership teams and employees — to improve the sustainability of their business models and operations.

The 2021 climate change report from the United Nations Intergovernmental Panel on Climate Change has drawn even greater attention to the environmental side of the matter. According to the report, scientific evidence points to human activity as the “unequivocal” cause of climate change. The statement marks a tonal shift that’s now being reflected by the sentiment of corporations globally.

Most companies understand that to successfully address sustainability, it must be at the heart of strategy, operations and value creation. However, companies can play offense or defense depending on the level of ambition and desire for a transformative approach. The financial impacts are complex, but an established consensus is clear — sustainability is an imperative that presents real opportunities for businesses in driving innovation, developing new products, offering new services and meeting rapidly evolving stakeholder needs.

Our Partners share their thoughts around six key sustainability themes observed across L.E.K. Consulting’s global practice areas and client base.

The philosophies and themes behind sustainability have been around for many decades with the notions of corporate responsibility, sustainability and ESG. One of the most critical areas of sustainability, addressing the climate crisis and the decarbonization required to do so, has increased in urgency. That’s been evident even in the past few months, with a confluence of events across political, governmental and societal forums driving an even greater commitment to a net-zero carbon world. In parallel, there have been developments in corporate sustainability reporting and a general rise in expectations around businesses’ sustainability plans.

Momentum is building, with about one-third of the largest 2,000 companies globally already having a net-zero emissions target in place. Concerns are now translating net-zero targets into real actions, and L.E.K. has written on the importance of considering the trajectory to net zero, not just the end date. Capital inflows to sustainable investment funds and financial institutions are growing as well, with examples of single fund raises geared to carbon transition exceeding $1 billion, not to mention the growing number of socially responsible exchange-traded funds now on the market.

While the COVID-19 pandemic initially brought new and pressing priorities for companies, governments and society more broadly, there’s strong evidence that it has reinforced the need to prioritize sustainability. JP Morgan and the Carbon Trust each conducted surveys on the early financial recovery from COVID-19 in late 2020. JP Morgan’s survey found that 55% of respondents believed the impact of COVID-19 would be positive on ESG investment momentum over the next three years. Carbon Trust’s survey validated that perspective, showing that sustainability and the environment had become more important for 74% of respondents for the future after COVID-19.

A number of parallels have also been drawn between the pandemic and the climate crisis. There’s been a recognition that we were woefully underprepared to deal with a high-impact catastrophe, and mitigating that is important in the face of the next climate-related catastrophe. We see further parallels in behaviors — the pandemic has demonstrated that people will actually change their behaviors quite dramatically if required.

However, the pandemic has also thrown up challenges (e.g., the lack of a global coordinated response), and the climate crisis requires behavioral change over a much longer period. As companies seek to recover from the impact of lockdowns, we’ve seen a rise in interest from clients seeking development and mobilization of their sustainability strategies across geographies and sectors.

Consumer-focused businesses are leading on circular economy initiatives and responding to increasing demand to provide products with strong sustainability credentials, while maintaining the functionality and costs consumers are asking for.

Industrial companies face both challenges and opportunities from the Energy Transition together with a drive to establish resilient and sustainable supply chains. Their aim is to ensure diversity and inclusion in the workforce and adopt strong work practices around the globe.

Healthcare companies are innovating in areas such as value-based care models, personalized and precision medicines, supply, manufacturing, and novel patient engagement.

Life sciences companies are confronting the environmental impact of manufacturing, packaging and waste management; issues of affordability; and the gap between high- and low-income countries in their access to medicine.

Energy companies are focusing on two angles to sustainability. On the conventional side, capital is flowing to decarbonizing operations. For example, Exxon is driving development of a carbon capture hub in Houston and certifying natural gas methane emissions management for customers. On the other side, the rise in renewables and solutions such as electric vehicles is driving demand for storage (e.g., battery technology) and further innovation in new technologies such as green fuels and hydrogen.

Travel and transportation companies are wrestling with the challenge to fund the move to more expensive zero emission fleets in an environment of increasing government regulations and requirements.

The European region is generally ahead of the curve on several dimensions, particularly those related to the environment, but there has been a distinct acceleration of intent from North American businesses. Although environmental issues are often front and center in discussions, diversity and inclusion issues have become more important across sectors and regions. So has governance in the wake of corporate controversies, getting to the heart of corporate responsibility.

One of the most common observations is the importance of sustainability in its broadest sense to younger employees irrespective of sector or geography. This is a critical constituency for today’s corporate leaders to engage and show progress with.

On the investment side, there’s significant uncertainty about how costs of key technologies are expected to evolve, impacting decisions around investment choices and timing. It’s clear that capital allocation is becoming that much more important with trade-offs requiring careful analysis and longer-term perspective. The potential returns can be challenging to quantify; while investors value a strong sustainability strategy, isolating the impact on multiples and profitability can be difficult — and arguably misleading given the rate of change of key considerations.

Some companies are looking for clear evidence that investment in sustainability will improve financial performance. But this is complicated and, if not carefully assessed, may lead to unintended consequences as regulation and/or external pressure tightens.

Alternative narratives focus on the fact that businesses have to become more sustainable, and so the key is getting it right. As far as addressing climate issues and the Energy Transition, we increasingly see that as the approach to take. The transition will happen; it’s about navigating it as successfully as possible and ensuring a proactive approach can provide strategic advantage.

Navigating a clear path is difficult, but a lack of clarity can create tension within organizations over where activities should fall in the hierarchy of strategic sustainability.

Divergence is emerging across organizations, with some taking defensive- versus offensive-minded positions toward sustainability. For some companies, sustainability is all about compliance and minimizing risk. It’s worth pointing out that even such a seemingly passive approach can often still require significant change and investment.

Other companies then seek to take more of a leading role among peers. What counts as leading is changing rapidly as companies improve — and so a once-leading strategy can very quickly become table stakes. For example, in Europe, a 2050 net-zero target is increasingly not seen as ambitious or leading, even in difficult-to-abate sectors. Within the leaders, there are the true innovators, the game changers that make sustainability their essence and mission. This is increasingly being recognized by investors and the financial markets.

Consensus continues to build around sustainability, creating substantial opportunities. New markets are becoming established (e.g., electric vehicles), new technologies are being developed (e.g., e-fuels) and new products and services are being launched (e.g., more sustainable food production methods and new sustainable packaging offerings).

However, companies need to act now to realize the potential opportunities that sustainability can bring. Success will require adept management of uncertainties, assessment of evolving market preferences, and an ability to reflect the pace and tone of government policy responses — such as potentially material implications coming out of the 2021 United Nations Climate Change Conference (COP26).

All businesses have the chance to make their products, services, operations and supply chains safer, circular and less emissions intensive. They can develop a diverse, inclusive workforce and make a positive impact on local communities. And they can choose best-in-class governance structures to inform sustainability choices on an ongoing basis.

By taking a structured approach, L.E.K. clients can capture opportunities throughout their entire value chains and ecosystems in terms of:

In M&A, we increasingly see ESG issues impacting inorganic growth strategies, approaches to due diligence, valuation considerations and ultimately deal outcomes. Meanwhile, more boards are bringing sustainability front and center to corporate decision making.

These are exciting yet complex times for businesses as they balance near-term financial performance with the desire to set and deliver on sustainability targets. Successful players will put sustainability at the heart of strategy and steer their “where to play” and “how to win” choices accordingly.

The L.E.K. Sustainability Centre of Excellence draws together the expertise, best practices and strategic insights necessary to support your approach, address the challenges and capitalize on the opportunities that sustainability brings.

L.E.K. conducted its fourth annual Brand Owner Packaging Study with 425 brand owners across the consumer packaged goods (CPG) spectrum.

Our findings show that packaging spend continues to grow in response to four major trends: competition on the shelf, SKU proliferation, sustainability goals and the acceleration of ecommerce.

The study also reveals that the pandemic has accelerated and intensified changes impacting packaging demand — presenting a set of significant and growing challenges for brand owners.

Meeting those challenges represents opportunity for packaging manufacturers and suppliers as well as investors in the packaging space.

The consumer packaged goods (CPG) industry faced several major challenges in 2021. The industry seems to be weathering the COVID-19 pandemic, and CPG companies’ spend on packaging is no exception — with spending on packaging continuing to increase in line with long-term trends across a range of brand product categories. And expectations are that the trend will be sustained. Sixty-five percent of brand owners expect to increase their packaging spend over the next two years. And for Tier 1 brands, the number is even higher — 78% of Tier 1 brand owners plan to increase their packaging spending.

But as in other sectors, the pandemic has served to accelerate and intensify changes impacting packaging demand that were already underway, such as the resumption of stock keeping unit (SKU) proliferation after a temporary reversal in some segments and the accelerating penetration of ecommerce. In parallel, there is rapidly growing pressure for sustainable packaging solutions from consumers and regulators — pressure that brand owners are hard-pressed to meet.

The result is a set of significant and growing challenges for brand owners with packaging decision-maker power. Meeting those challenges represents opportunity for packaging manufacturers and suppliers as well as investors in the packaging space.

To better understand how brand owner packaging needs are evolving — and the implications for the industry and investors — L.E.K. Consulting conducted its fourth annual brand owner packaging study in summer 2021.

We asked about brand trends and their impact on packaging, as well as changes to packaging itself. Specifically, we wanted to know:

Here’s what we learned.

Packaging spend on CPG brands has grown over the past two years. According to the self-reported numbers provided in the survey, overall growth over that period was 3.7% in 2019-20, approximately 200 basis points above the 1.6% rate of inflation as measured by the U.S. Consumer Price Index. Fifty-six percent of brand-owner respondents increased their spend on packaging during that period.

The biggest spending increases involved Tier 1 brands, where overall, 78% of those surveyed reported increased spending (and 36% increased it by 6%-10%). But private-label brands registered the most variability — 24% of those surveyed reported a spending increase of more than 10%, and 12% decreased it by more than 10%.

Going forward, respondents expect spend on packaging to increase further. Sixty-five percent of those surveyed said they anticipate growing their spending in 2022 and 2023, and nearly a third (31%) plan a 6%-10% increase. But most of the expected increase appears to be in Tier 1 brands — fully 78% of Tier 1 brand owners and decision-makers anticipate increasing their spend on packaging, with 18% forecasting a more-than-10% increase and another 18% looking at a 6%-10% increase. Only 4% of Tier 1 brand owners report they expect to spend less on packaging in the next two years.

Tier 2 and micro brand owners’ packaging spend forecasts are roughly in line with the overall forecast, and a degree of variability is expected to continue in private label, with 11% planning an increase of 10% or more, and another 11% expecting a decrease of 10% or more.

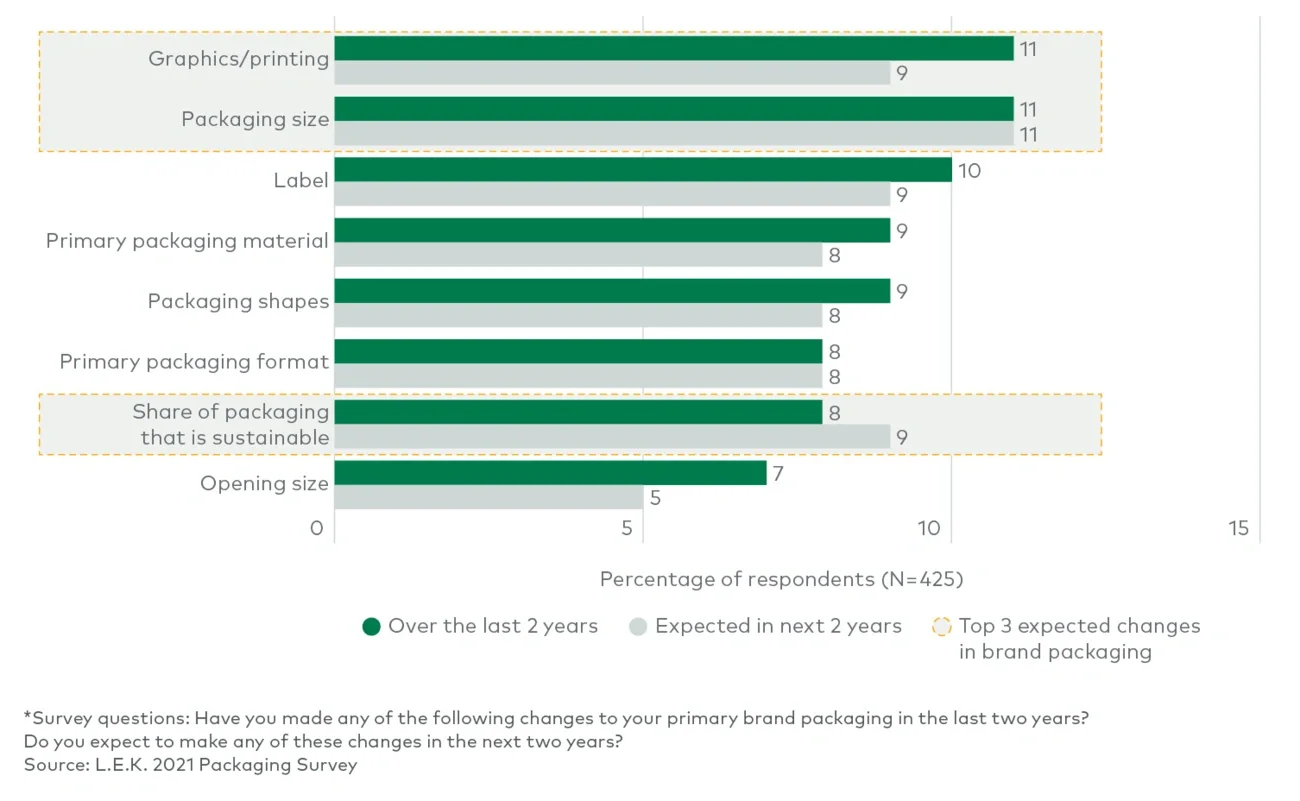

What are brand owners spending on? In a nutshell: brand promotion and sustainable and ecommerce-friendly packaging. Changes in graphics and printing lead the pack, especially in household and pet products. Spending to reduce the size of packaging (for example, by downgauging) is almost equally high. Changes in primary packaging materials, changes in packaging shape and format, and increasing use of sustainable materials are all the focus of spending increases. Change is in the air — only 3% of those surveyed report they expect to make no changes to their packaging in the next two years (see Figure 1).

Figure 1

Changes in brand packaging (2019-2023F)*

What’s driving the spend? It’s a response to four major trends that have impacted the industry over the past two years and continue to do so — increased competition on the shelf that leads to increased emphasis on packaging as a selling tool, continuing SKU proliferation, changes in packaging to meet sustainability goals and accelerating shifts in ecommerce.

The biggest spending driver is that brand owners continue to overinvest in packaging. This isn’t surprising given intense competition on the retail shelf for consumer mindshare and share of wallet, not to mention the continuing proliferation of SKUs (see below). Brand owners regard packaging as a high ROI tool for awareness, promotion and sales, and look to it to drive differentiation and win over consumers.

A spending rate that steadily doubles relative to the rate of inflation reflects the high demand for promotional packaging and high expectations for performance.

Overall spending levels are a response to competitive demands, but they are also a sign that the industry is healthy and that opportunity abounds for converters and investors — at least for those that can rise to the occasion and meet the challenge.

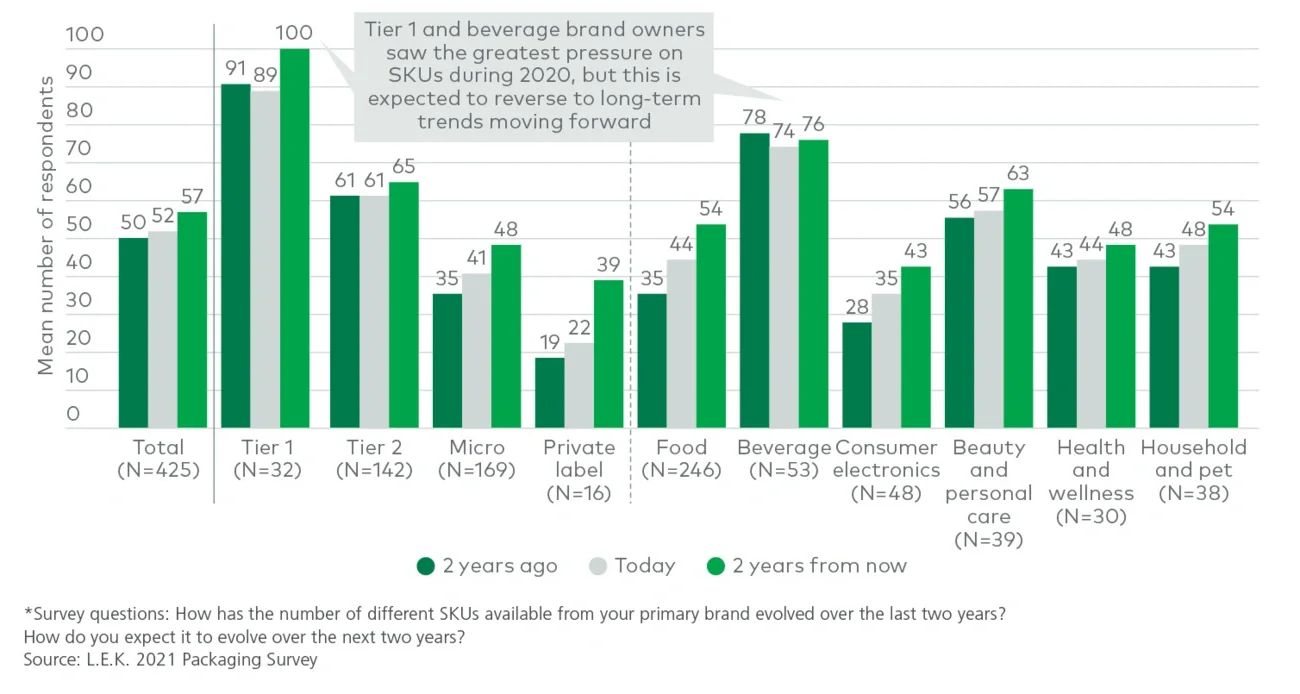

Despite COVID-19-related headwinds — especially among Tier 1 and beverage brands — SKU proliferation is expected to persist across consumer product segments over the next two years. Even factoring in the pandemic, the growth forecast is largely in line with long-term trends.

There was in fact some SKU rationalization at the height of the pandemic as supply chains became constrainers and brand owners responded by returning to their core SKUs. However, brand owners report that the SKU count is likely to increase in the future, rebounding and resuming pre-pandemic growth rates.

There has been SKU volatility, especially in the beverage category and for Tier 1 brands overall. Both saw the sharpest decreases of any category during the pandemic, which was a temporary divergence from the long-term SKU proliferation trend. Both are expected to reverse the trend and grow over the next two years (see Figure 2).

Figure 2

Average number of SKUs available for primary brand (2019, 2021E, 2023F)*

Proliferation is not the whole story, however. Brand owners also report that they expect sales volume of top SKUs to increase modestly over the next several years. Again, this varies by segment. Micro and private-label brands generate significantly more sales (~45% and ~60%, respectively, in 2021) from their top SKUs, compared to Tier 1 and Tier 2 (~33% and ~35%, respectively, in 2021). But overall, brand owners expect the sales volume for top SKUs as a percentage of overall sales to continue to grow (from 40% in 2021 to 42% in 2023) while other top SKUs and long-tail SKUs decline somewhat as a share of sales.

All of that suggests that run lengths for long-tail SKUs will continue to decrease — and that there will be disproportionate benefit for industry participants that can support brand owners that require shorter run lengths and custom packaging and labeling — including design. And thanks to SKU proliferation, the overall profit pool is expected to expand at rates greater than market growth. But to meet the challenge, converters will require design support and they will need to maintain — or increase — their flexibility. At the same time, the likelihood that Tier 1 brands will continue to rely on long run lengths means that the ability to provide cost-effective production for long run lengths will still be a differentiator for industry participants seeking to win over Tier 1 accounts.

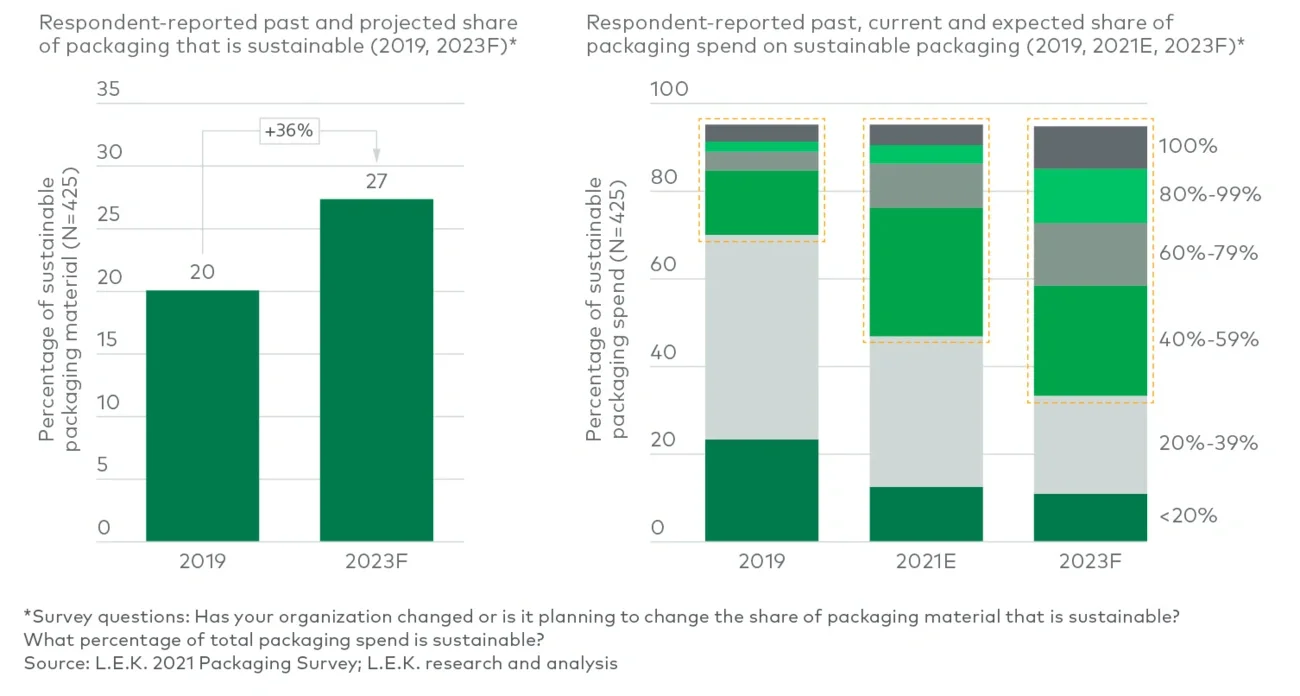

As in multiple industries, sustainability is a significant factor in packaging. In fact, when asked what the greatest change in packaging has been over the past two years, most respondents cited an increase in the share of sustainable packaging.

But when it comes to sustainability, brand owners find themselves running behind. Approximately 74% have set a sustainability goal for 2025. But the majority of brand owners report they are behind the pace required to meet their target. They report that to date, they have achieved only 40% of their 2025 goals, and expect to meet only 68% of their targets when 2025 rolls around.

To advance their packaging sustainability goals, most brand owners are focused on materials. Asked for their top three criteria for sustainability, 42% cited recycled content, 30% cited biodegradable materials, 28% cited compostable materials and 28% cited materials manufactured using renewable energy. Ranking at 27% or lower were manufacturing issues (carbon footprint to manufacture, minimal materials) and working with suppliers that support environmental issues.

Perhaps under pressure to meet their targets, brand owners appear ready to pick up the pace. They reported they expect to increase the amount of sustainable material in their packaging by 36% from 2019 to 2023, and to spend dramatically more on sustainable packaging by that year (see Figure 3).

Figure 3

Spend on sustainable packaging

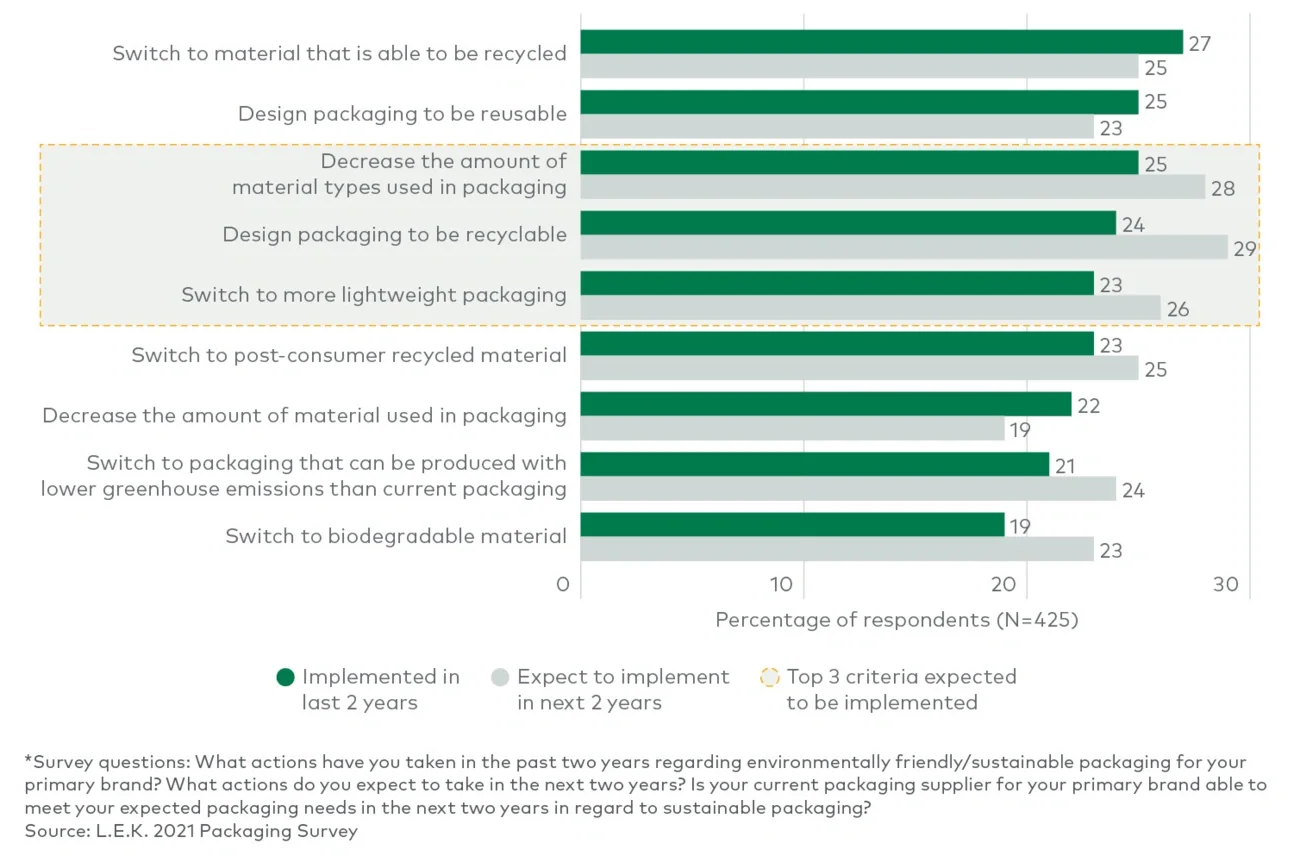

Their main focus is on decreasing the number of material types used in packaging, designing packaging to be recyclable and switching to lightweight packaging (see Figure 4).

Figure 4

Actions taken on primary brand regarding sustainable packaging (2019-2023F)*

But access to materials is a significant limiting factor. While ~75% of brand owners reported they have some access to sustainable packaging materials today, the capacity of material recycling facilities (MRFs) is insufficient to meet the demand. That suggests there will be future imbalances for supply. And a shortage of recyclable materials adds to supply-side pressures, especially for plastics, where only 9% of the material in use is currently recycled.

The struggle to keep pace on sustainability targets and the materials shortfall represent major opportunities for industry participants and investors. Any converter able to partner with brands to decrease packaging weight and to design recyclable packaging will achieve a critical level of differentiation. Also critical for differentiation is the ability to ensure sufficient supply of sustainable packaging materials. There have been examples of converters purchasing or developing supply relationships with MRFs in order to reduce supply risk.

Ecommerce growth continues apace — with the pandemic accelerating well-established trends. Brand owners expect pandemic ecommerce gains to hold and brick-and-mortar share to fall ~10% from an indexed 2019 baseline between 2019 and 2023.

So it’s not surprising that brand owners report making increasing use of ecommerce-specific formats. Approximately 50% of brand owners report using them, and 56% have increased their spend on ecommerce packaging relative to regular formats.

But with increased ecommerce emphasis come concerns — in particular about packaging performance. In fact, brand owners value function (such as lightweighting and performance through the fulfillment process) more than sustainability. They seem to be following the advice of legendary auto racing engineer Colin Chapman: “Simplify, then add lightness.” Thirty-six percent report acting to reduce packaging weight, 32% report introducing new formats, 31% report reducing packaging size, 29% report they have redesigned their packaging for automated environments and 28% report increasing protective packaging to avoid damage in transit. En route damage is especially concerning for the consumer electronics industry, which needs cost-effective ways to ship fragile products.

Given the enormous and sometimes contradictory-seeming challenges involved in ecommerce packaging — protecting the product, reducing weight, promoting the brand — brand owners are likely to value solutions that the packaging industry can provide. Participants that serve brands that are winning in ecommerce can generate above-market growth. But to gain traction, it will be necessary to take a consultative approach, add value by helping brand owners overcome challenges and create shipping-friendly — as opposed to generic — packaging formats.

Interestingly, some of the value-add capabilities required for ecommerce performance — such as reducing packaging weight — are also central to creating sustainable packaging. There’s a strong business case for adding capabilities that allow converters to produce lightweight packaging that targets both sustainability and ecommerce needs.

Given the complex and sometimes contradictory dynamics of the CPG industry — marked by external challenges, increasing overall spend and shifting priorities — where do the opportunities lie?

The major opportunity for converters and investors alike is to partner with brand decision-makers, understand what they are up against and deliver value-added solutions.

In practical terms, delivering those solutions can take many forms. Some providers will be able to draw on existing capabilities. Others will need to build or acquire them.

One of the most significant sets of challenges — cutting across both sustainability and ecommerce — concerns materials. The ability to, for example, work with sustainable materials without sacrificing performance, or to design packages that reduce weight while providing robust product protection for ecommerce, will be a main source of competitive advantage.

For industry participants, enhancing or adding such capabilities should be a strategic priority. For investors, identifying companies that offer these capabilities, or facilitating strategic acquisitions that add such capabilities to the offering, has the potential to be a pathway to competitive returns.

The good news is that while the industry is changing, its trajectory seems clear. Act now to be ready for a world of continued SKU proliferation, intensifying sustainability demands and a continued shift to ecommerce — and to help brand owners rise to the challenge.

If you would like to learn more or request access to the full 2021 Brand Owner Packaging Study, please contact us at industrials@lek.com.

The nutritional supplement market has experienced dramatic growth, particularly in ecommerce sales.

L.E.K. Consulting surveyed over 1,000 consumers to better understand these changes.

We found that food, drug, mass merchandise and club (FDMC) is the largest category, but Amazon is a powerful launching pad.

Channel strategy is critically important to the success of new products, and considering your consumers in terms of channel preference can provide an edge.

It’s no surprise that COVID-19 has upended consumer buying patterns for a wide array of products. The nutritional supplement market is no exception. According to the Nutrition Business Journal, the nutritional supplement market experienced dramatic growth of 14.5% from 2019 to 2020. Furthermore, in an industry where brick-and-mortar sales dominate, ecommerce rose from 10% to 17% of sales in the same period.

To better understand these changes in consumer behavior, L.E.K. Consulting surveyed over 1,000 consumers who spent at least $25 on vitamins, minerals and supplements (VMS) or active nutrition products in the previous 30 days. We asked them about both their usage of these products and their buying preferences.

Our first question was whether changes in the market over the past year are likely to persist. The short answer is, we think so. Our research indicates that the dramatic growth in the nutritional supplement category and the shift toward online purchasing are primarily due to an acceleration of existing trends.

COVID-19 sparked an intense focus on personal health. It brought new consumers into the nutritional supplement market who were looking for general wellness products or immunity solutions. In addition, it deepened the participation of existing consumers who were seeking expanded solutions in areas such as sleep, anxiety and mood. But it doesn’t appear that this focus is temporary.

For example, we asked consumers about their vitamin consumption before and during COVID-19, as well as their expected usage once the pandemic eases. The percentage of nutritional supplement consumers using vitamins at least four to six times per week increased from 74% pre-COVID-19 to 80% during COVID, and 81% say they expect this level of usage post-COVID-19.

Ecommerce grew disproportionately during COVID-19. While some share gains will be lost to offline channels in a post-COVID-19 world, our survey suggests that some 60% of the ecommerce share gains will remain, establishing a new baseline for ecommerce moving forward.

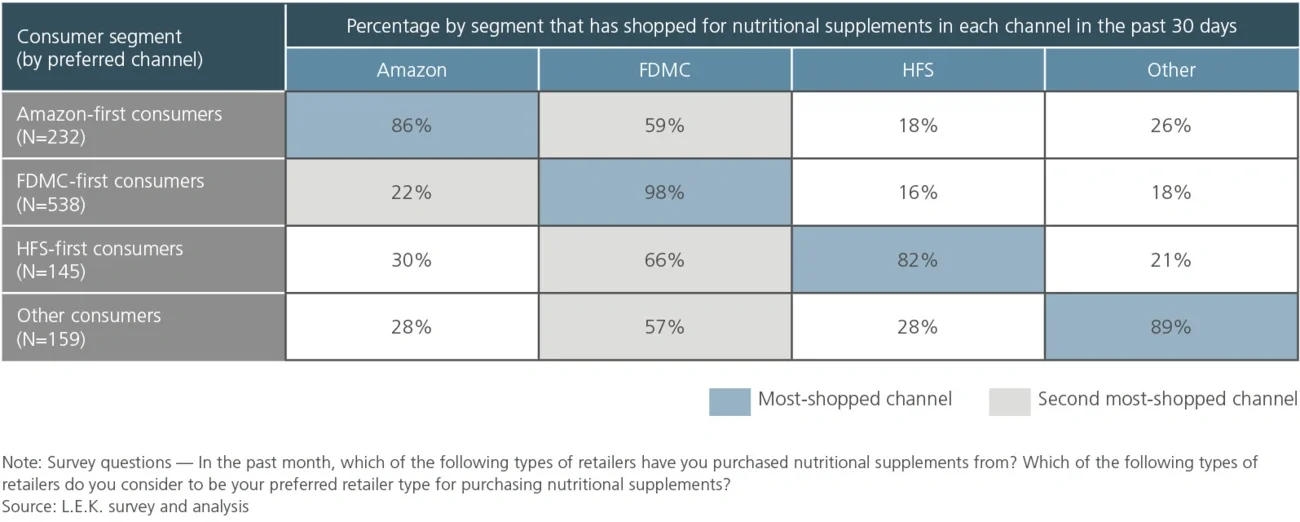

A common way to analyze consumers is to look at where they shop. However, because there is so much cross-channel shopping in this category, we decided to conduct our channel analysis with a twist: by segmenting nutritional supplement consumers based on their preferred shopping channel rather than based on where they actually purchased products. These consumers don’t shop exclusively in their preferred channel ― they would just rather shop there, all else being equal. Looking at the market through this “preferred channel” lens yielded some important insights into consumer buying behaviors, attitudes and key purchasing criteria.

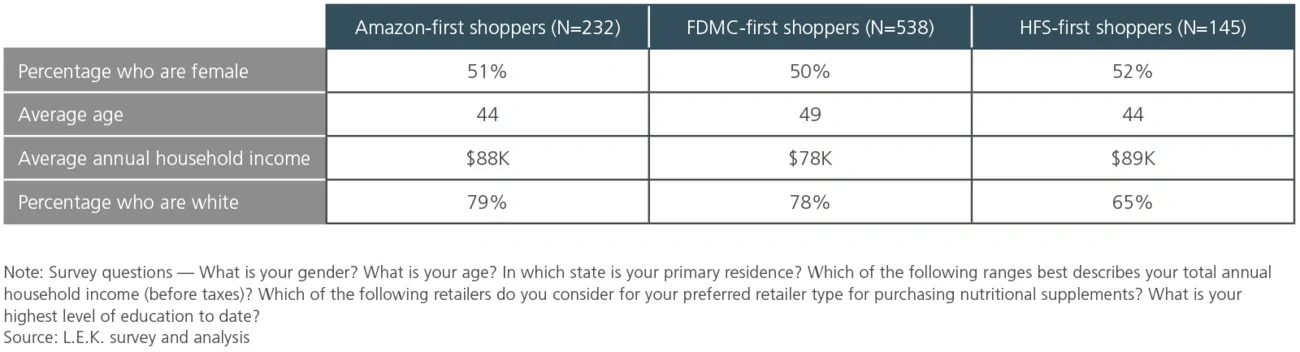

We categorized consumers into three preferred-channel groups (see Table 1).

This group prefers to shop in FDMC big-box stores for nutritional supplements. They skew older and are the least wealthy of the three groups. They report spending an average of $1,250 per year on nutritional supplements. They shop more for “core” products (general health and multivitamins) and for those promising immunity (likely a result of COVID-19). They say they need more guidance in finding the right product for them. This group focuses on value, price per unit, total cost and preferred modalities (e.g., gummies).

Consumers who shop Amazon first tend to be younger and wealthier. They report spending around $1,300 a year on nutritional supplements and are willing to pay for quality and try new products with innovative ingredients. They tend to shop for condition-oriented products and wish that major retailers had a better assortment to choose from. They also place emphasis on online reviews and perceived value (not lowest cost).

Like the Amazon-first group, health food store (HFS)-first consumers are younger and wealthier. This is the highest-spending group, with an average annual reported expenditure of nearly $1,500. Overall, they have a high engagement with the category and are willing to pay for quality, but most importantly they demand all-natural solutions. Their favored purchases include condition-oriented and active nutrition products. They wish traditional retailers had a better assortment. They place a high value on products with clinical backing that meet organic and clean-label standards.

Of course, a preferred channel doesn’t always dictate where shoppers end up shopping, so we also looked at where consumers purchased nutritional supplements in the past 30 days (see Table 2). The first thing that jumped out was that almost all FDMC-first consumers (98%) shopped in their preferred channel in the past month, compared with 86% of Amazon-first consumers and 82% of HFS consumers. Secondly, when shopping outside their preferred channel, consumers most frequently shop for nutritional supplements in FDMC (59% of Amazon-first shoppers and 66% of HFS-first shoppers). These findings, combined with the fact that FDMC-first consumers comprise the largest category, underscore the importance of this channel.

Knowing where your customers prefer to shop can tell you a lot about who they are and how to meet their needs. The findings from our survey imply a roadmap for new brands, as well as for brands seeking to broaden their reach.

As our research shows, the online channel has experienced a step-change in growth as a result of COVID-19. While the eventual end of the pandemic may partially reverse the trend and return consumers to in-store purchasing, ecommerce will remain a powerful channel — and Amazon is by far the dominant player. Companies can set up an Amazon store fairly quickly, and Amazon can handle the bulk of the logistics. Amazon’s digital marketing programs are a further benefit. Amazon also makes an ideal platform for condition-specific products including those targeting heart, digestive health, weight, beauty and mental/cognitive health — all areas for which Amazon-first consumers are receptive buyers.

The unique profile of Amazon-first customers suggests a few key strategies for success:

For brands looking to expand beyond an online presence on Amazon, it helps to understand how customers shop in different channels and what they are looking for. In this way, brands can customize their offerings and marketing strategies to provide prospective retailers with the potential for incremental category sales.

FDMC remains an important channel. FDMC-first consumers are the largest customer base and represent the most overall spend. Additionally, FDMC is the most-shopped channel when non-FDMC-first consumers shop outside their preferred channels, primarily due to convenience. These consumers tend to be value oriented, prioritizing price per unit, and focused on general health and immunity products. Generally speaking, FDMC-first customers have less interest in trying new or innovative products.

The products best suited to the FDMC channel are value and core VMS products. You can raise awareness of your products via digital platforms and strategic use of social media influencers. Messaging that emphasizes simple, easy-to-understand ingredients and reasonable prices is likely to be the most effective. Goli Nutrition is a prime example of an innovative yet simple brand whose marketing strategy helped garner impressive FDMC success. Goli used highly effective social media campaigns, as well as midi- and micro-influencers, to break into FDMC in a big way.

HFS-first consumers are similar to Amazon-first consumers in that they are willing to pay for and try new products and want more innovative products. Like the Amazon-first customer, they are open to a longer list of condition-specific offerings. HFS-first consumers also place significant value on all-natural products and clinical studies supporting effectiveness.

Given what we know about consumer preferences, there is an opportunity for brands to appeal to both Amazon-first and HFS-first shoppers with premium, condition-specific items.

FDMC-first customers are interested in guidance on locating the right products. This finding suggests that once you have gained a foothold in FDMC, you can expand your presence through increased personalization and offering a range of products to accommodate specific customer needs. For example, multivitamin maker Smarty Pants has been very successful with its offerings targeted at specific groups with varying nutritional needs, including toddlers, kids, teens, pregnant women, and men and women in different age groups. There may be opportunities to explore further personalization as personalized nutrition becomes more mainstream.

Channel strategy is critically important to the success of new products in the nutritional supplement category. Yet developing an optimized channel strategy can be a complex endeavor, especially in a post-COVID-19 world where priorities and shopping patterns may have shifted. Thinking about your consumers in terms of channel preference rather than historical buying patterns can provide an edge and suggest innovative ways to gain traction with your core set of customers.

We’ve been unpacking key findings from the L.E.K. Consulting 2021 Energy Transition Study. In our last article, we talked about the budget allocations for energy transition capabilities and initiatives that are rising across all segments of the oil and gas industry. Now let’s look at where those allocations are going.

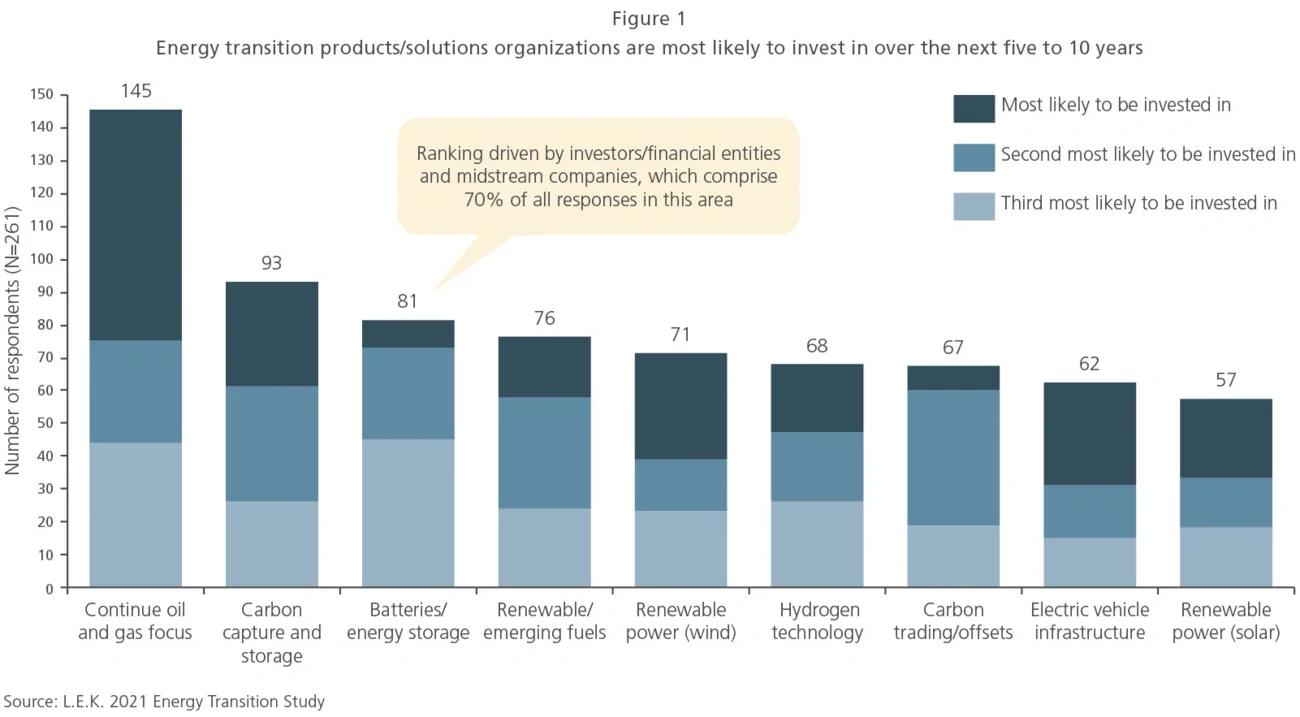

We gave our 261 respondents — all energy executives — a list of products and solutions. Then we asked them to select the three that their organization was most likely to invest in over the next five to 10 years. We also asked them to rank their top picks in order of priority (see Figure 1).

The results vary by type of company, but in general most participants indicated that energy transition solutions/initiatives that are closer to their current operations are most likely to get investment attention versus other initiatives that are longer term and farther from their respective core business.

Here’s a breakdown of the top three energy transition solutions/initiatives based on survey responses:

What’s the takeaway? In the short-to-medium term, traditional oil and gas will remain a top priority among all segments of the oil and gas industry. But expect to see some shifts. Here’s what the top investment areas seem likely to become, in order of priority:

In our next article, we’ll share what oil and gas executives say about where the greatest investment opportunity is in the longer term.