This is the first installment of The Great Reopening and Priority Reset Series, which reflects the results of a recurring consumer pulse survey. The objective of this series is to highlight the “priority reset” happening among consumers and how it is affecting their priorities for post-COVID-19 spending.

We will be publishing two parts for this edition. Edition 1, Part 1 will cover macro themes, and a subsequent report will identify strategically relevant segments of consumers with distinctly different attitudinal and behavioral profiles.

This survey includes responses captured April 21-23, 2021, from ~1,000 U.S. consumers who are demographically representative of the general population. Additional surveys can be found at the L.E.K. COVID-19 Insights Center.

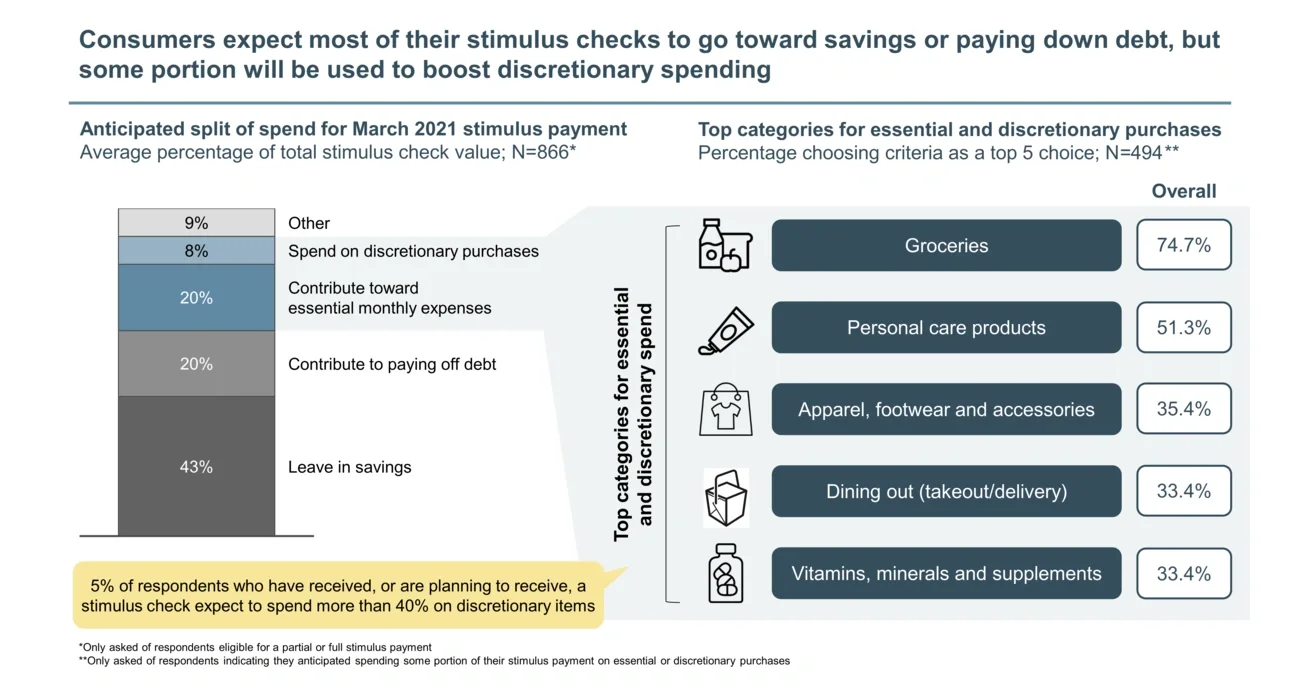

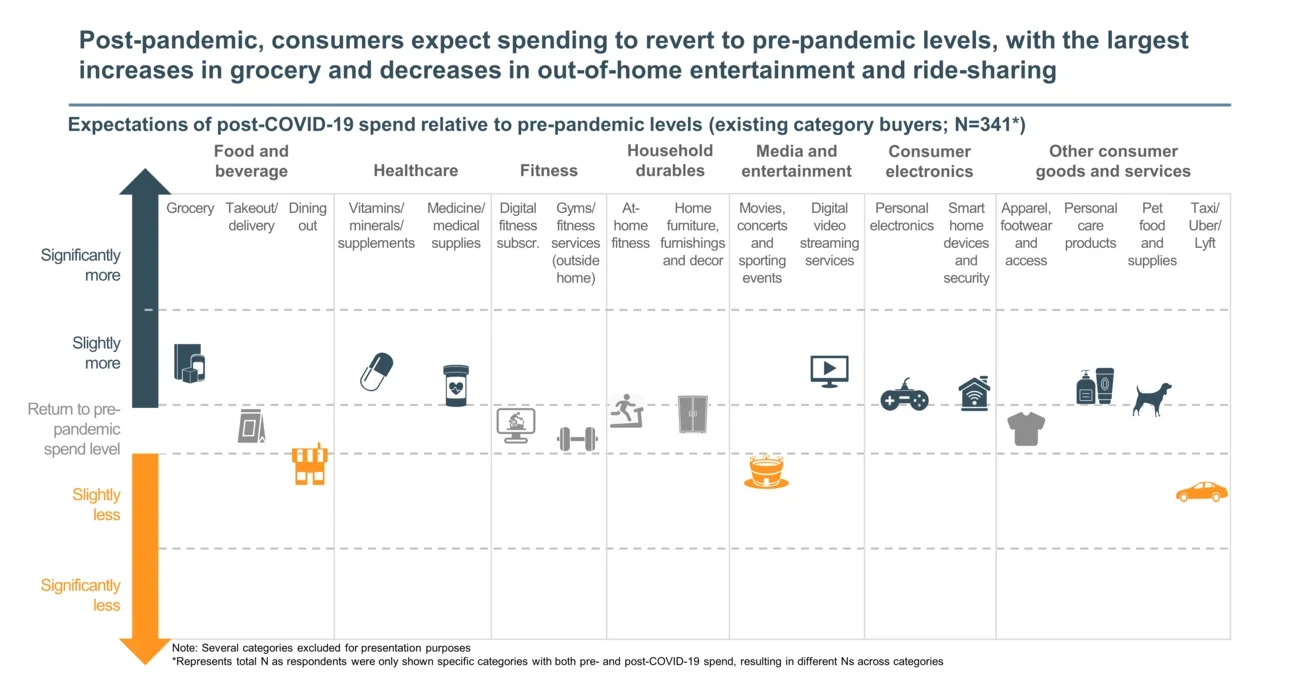

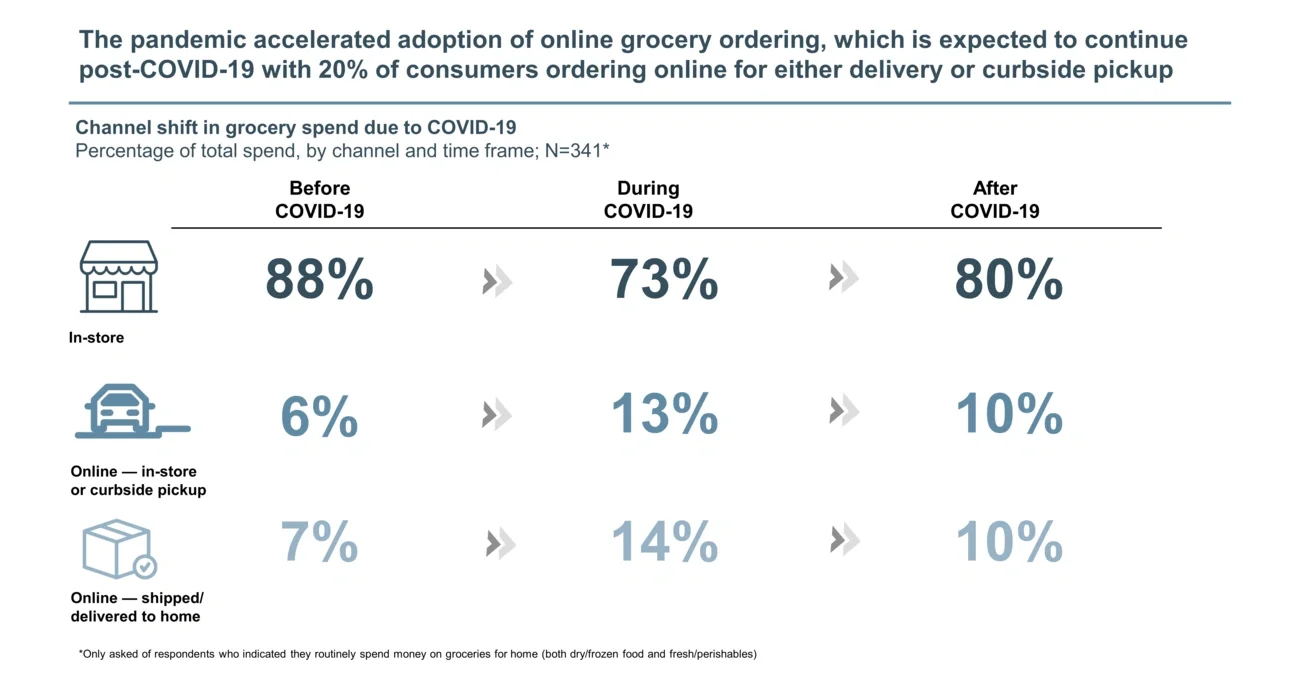

Edition 1, Part 1 yielded a number of interesting insights about changes in consumers’ expectations of activities they will engage in and categories they expect to spend money on once the outbreak is contained.

Important note: All forward-looking data reported is a reflection of consumer sentiment/expectations and is not an official L.E.K. forecast.

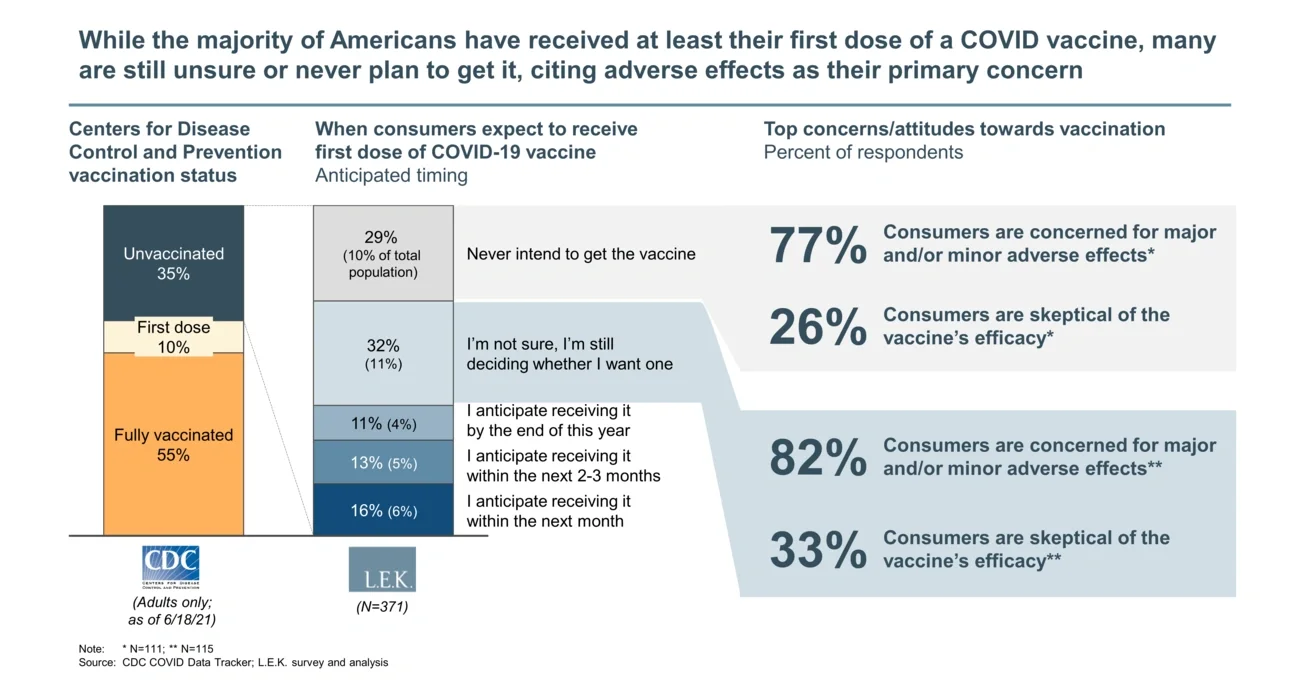

Many Americans are unsure about taking the vaccine

Government investment and resources have been instrumental in mobilizing the vaccine effort across the country. With the supply of vaccines continuing to increase and states continuing to broaden eligibility standards, many Americans have been able to get at least their first dose of the vaccine in recent months.

As of June 18, 2021, the Centers for Disease Control and Prevention (CDC) reported that almost 148 million Americans have been fully vaccinated and another 28 million have received at least their first dose. While many Americans continue to schedule appointments for the vaccine, many others still have strong concerns about its efficacy and the potential for adverse side effects.

Overall, the results from this survey suggest that ~10% of Americans never plan to get the vaccine and another ~11% are still unsure about getting it, although those proportions vary across demographics (e.g., race, gender, political affiliation, level of education).

The most common concern among those who are unsure about the vaccine or never plan to get it is the potential for adverse effects. This concern is shared almost universally across the major demographic cuts available in the data.