Related insights

You might also be interested in these insights.

English

Loading transcript...

The scalability of software presents limitless growth opportunities for businesses from day one. However, without a clear strategic focus, the sheer number of options can be overwhelming. Gaining strategic clarity allows businesses to prioritize the most impactful growth paths, ensuring sustainable success and the ability to scale globally.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

Loading transcript...

Scaling a software company involves balancing growth strategy, product differentiation, sales and marketing execution, and operational scalability. A clear growth strategy provides clarity on long-term direction, while product differentiation and pricing ensure sustainable monetization.

Strong sales and marketing execution drive customer acquisition and retention, while scalable processes help build long-term efficiency. However, most companies can only optimize one or two areas at a time, making strategic focus critical to sustainable growth and competitive advantage.

Watch the full video to learn how investors and operators can prioritize the right initiatives to maximize value in software assets.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

While the number of transactions has fluctuated in recent years, North America saw significant growth in transaction value in 2024, outpacing the overall M&A market. Investment in education remained strong, with a rise in mega deals.

The overall number of deals remained steady, with some recovery in lower-value segments. This recovery is supported by the four-quarter moving transaction value average, which declined from Q4 2021 through Q3 2023, began rising in late 2023, and continued its upward trend in 2024.

Private equity took a leading role, gaining transaction share from corporate M&A. Corporate training and professional upskilling consistently accounted for the highest share of total transaction volume over the past five years, followed by K-12, higher education and early childhood education (ECE).

Low interest rates, buyer and seller alignment on value expectations, and strong underlying growth drivers — such as demand for upskilling/reskilling, bridging the K-12 learning gap and the need for higher education to diversity revenue — mark positive shifts for 2025. Investors should watch for policy and regulatory changes, as well as deal fatigue following similar transactions in 2023 and 2024.

Our analysis unpacks the trends shaping education M&A and the strategic priorities investors should consider.

Private equity firms played a leading role in education M&A in 2024, capitalizing on the sector’s recession resilience and technological transformation potential. While corporate buyers remained active, PE investors pursued deals in adjacent sectors such as technology and healthcare, with a strong focus on expanding into education.

The return of larger transactions also stood out. Mega deals over $1 billion spanned K-12, higher education and youth enrichment, underscoring sustained investor appetite for scalable opportunities.

Despite a cautious investment environment, three segments led deal activity:

With valuations stabilizing and deal sizes increasing, 2024 set the stage for a more dynamic investment landscape in 2025.

Education remains a resilient and attractive investment sector, with M&A activity poised to accelerate in 2025. As market conditions evolve, investors will need to align their strategies with the shifting demands of learners, institutions and employers.

For a deeper dive into these trends and their strategic implications, please download our full analysis and get in touch.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

Navigating a post-pandemic market, a premium kitchen appliance manufacturer faced decreasing demand, leading to negative EBITDA margin in its largest business unit. The company needed a comprehensive end-to-end supply chain assessment to identify areas to reduce cost of goods sold and improve product margins as part of a holistic go-to-market strategy refresh.

L.E.K. Consulting took on the challenge with a two-phase approach to identify and validate cost reduction opportunities and develop a detailed implementation plan to return the company to profitable margins.

The comprehensive supply chain assessment and category strategy development equipped the company with the tools to drive a substantial margin improvement. Key outcomes include:

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

A leading biopharmaceutical company engaged L.E.K. Consulting to optimize its global manufacturing network. The client sought to reduce costs while maintaining business continuity and production flexibility so that it could adapt to varying demand. Facing a potential downturn in demand — particularly in a worst-case scenario for several key pipeline products — the company needed a blueprint for network rationalization. This entailed evaluating network configuration options, assessing the financial and strategic implications of potential scale-backs and third-party outsourcing, and weighing various operational risks, including business continuity, supply chain stability and regulatory requirements.

The biopharma required a strategy that balanced near-term cost savings with longer-term flexibility, ensuring the organization would remain competitive and resilient under changing market conditions.

Current-state network assessment

We began by examining the cost burden across the biopharma’s global manufacturing network under a downside demand scenario, establishing a baseline to measure rationalization opportunities. We identified a range of options to reallocate capacity, considering owned and third-party site capacity constraints, regulatory limitations, financial obligations, and capex associated with site capacity expansions. Our approach evaluated average cost per dose across the network under each reallocation option, incorporating the fixed and variable cost profiles of each site.

Identification of future-state network configurations

Our team analyzed the economics of internal and third-party sites under the baseline and downside demand scenario volume levels to identify breakpoints where external sites are more attractive than internal sites, including cost of goods sold (COGS), overhead, startup costs and existing financial commitments. We then developed five network configuration options, including divestment of owned site(s) to outsource more volume to third-party contract manufacturing organizations (CMOs) and replacement of higher-cost third-party CMOs with lower-cost blends of insourced production and other CMOs.

We evaluated the cumulative three-year cost savings associated with each of the five options relative to the current-state baseline, considering cash impacts in addition to run-rate cost savings (e.g., cash inflow from site divestment). These options provided savings upwards of 7% of total network cost ($80 million), in addition to material cash inflows.

Option evaluation and risk analysis

We weighted run-rate savings and cash impacts against the critical network risks of each option and the strategic implications of removing network nodes. Divesting owned sites ran increased risk of business continuity interruptions and higher rates of quality issues. However, a greater degree of insourcing would decrease flexibility to scale in higher-volume scenarios and jeopardize key partnerships.

Recommendations and roadmap

Based on our findings, we advised a demand-dependent approach. Should the downside scenario not materialize, we recommended preserving the current network and maximizing efficiency through reallocation of capacity. This would enable the biopharma to maintain critical redundancies, avoid network continuity disruptions and maintain control of key manufacturing stages. If the downside demand scenario materialized, we recommended divestment of the highest-cost site to unlock near-term cash flow and materially reduce fixed cost in the network. We also developed a high-level roadmap, identifying triggers for recommended choices and key execution milestones.

Our team provided the biopharma a portfolio of network rationalization options to realize significant cost savings with varying degrees of production outsourcing. The portfolio of options enabled the biopharma to select a future state that best meets anticipated market demand, desired operational flexibility and risk appetite.

Cost reduction

The biopharma received actionable steps for cutting overhead and production costs, achieving meaningful near-term savings through focused consolidations and reallocation of capacity.

Informed decision-making

A comprehensive financial model and risk assessment empowered leadership to choose from rationalization strategies and select an option that effectively balanced cost efficiency with network resilience and business continuity.

Financial forecasting and flexibility

By anticipating multiple demand scenarios, the client can swiftly rebalance capacity across manufacturing activities as needed, safeguarding profitability and maintaining robust supply capabilities.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

A leading pharmaceutical distributor saw a sharp decline in warehouse productivity after implementing a new Warehouse Management System (WMS). L.E.K. Consulting was engaged to evaluate warehouse performance and identify improvement opportunities. Through a comprehensive, four-facility assessment, L.E.K. uncovered a 17%-34% potential productivity uplift and designed a phased implementation plan to capture the gains and restore sustainable operations.

The company lagged industry benchmarks in warehousing performance, with declining efficiency further driving up labor costs.

New technology investments failed to deliver expected productivity gains, with labor instead increasing to handle operational disruptions.

Management was unclear on where to focus for maximum uplift and sought an outside-in assessment to identify and prioritize 4-wall improvement initiatives.

Our team designed a rapid, hands-on 4-wall improvement program to identify operational challenges, develop efficiency uplift solutions and build a playbook for execution:

This hands-on assessment delivered actionable improvement opportunities that were initiated across the distributor’s network as a comprehensive performance improvement program. Collectively, this program enabled 17% labor reduction or capacity gain in one to two years, with 34% total uplift potential within three to five years.

Improvement opportunities were organized into five key solution areas:

We defined 2 to 5 target initiatives within each of these key solution areas, each with corresponding execution guidelines. The improvement program was divided into three phases: the first six months focused on building foundational tools and processes, months 6-24 on gradually rolling out improvement initiatives and months 24+ on aggressively pursuing improvement targets.

L.E.K.’s 4-wall DC improvement program disrupted the company’s status quo and established a clear path to reverse poor performance trends. If your business is looking to transform your warehousing operations, our Operations and Supply Chain team can help deliver similar impactful results.

Contact us to learn how we can drive sustainable improvements for your organization.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

Generative AI (GenAI) fundamentally shifts SaaS pricing from seat-based to outcome-/value-driven models, with many leaders viewing AI as transformative.

Companies are charging premiums for Microsoft Copilot-style AI features, with value created through both productivity enhancement and complete task automation.

Emerging pricing models are either outcome-based (pay per result), consumption-based (pay per usage) or hybrid subscription models combining fixed fees with variable AI components.

Data architecture becomes more critical than UI as workflows shift to AI agents, positioning companies with robust data infrastructure for success.

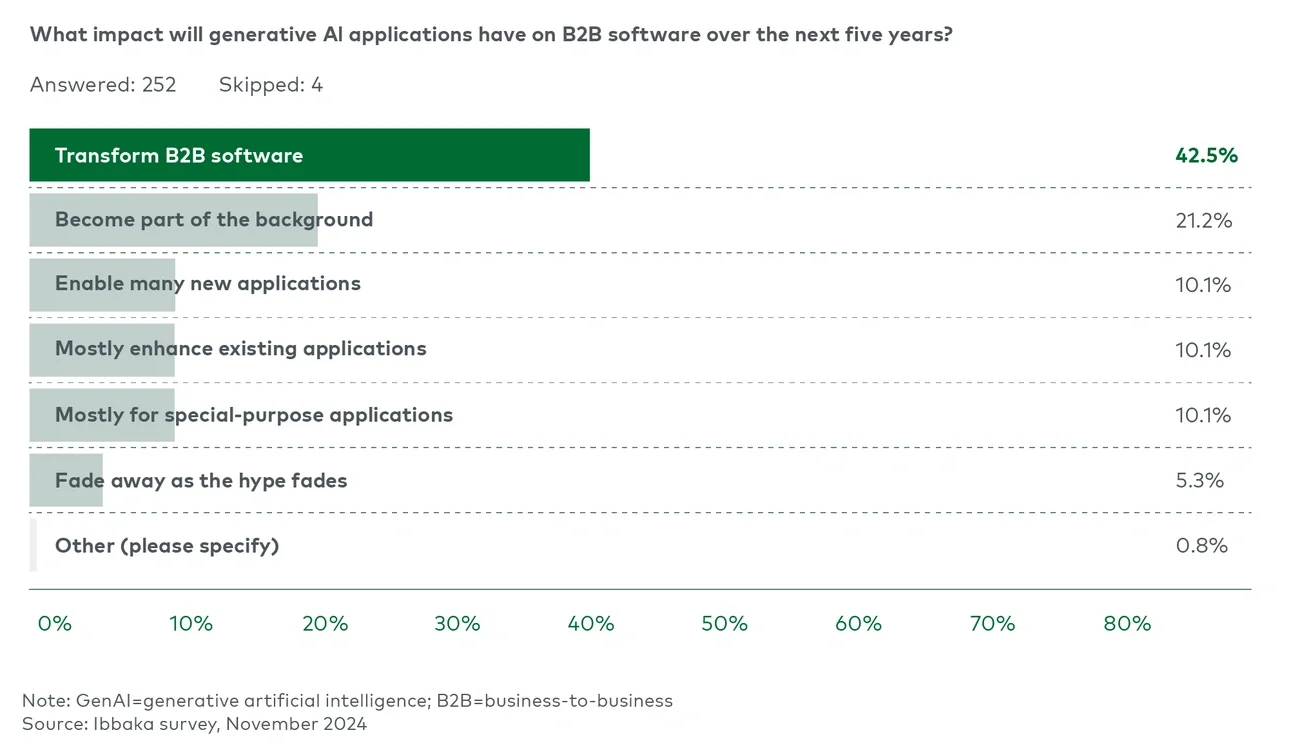

The business-to-business (B2B) software industry is undergoing a pivotal transformation driven by generative artificial intelligence (GenAI). Once primarily focused on enhancing human productivity, this technology is now reshaping how businesses develop, deliver and price their offerings. A recent survey revealed that 42.5% of industry leaders view GenAI as transformative, with the potential to disrupt domains such as development, sales and pricing (see Figure 1).

Figure 1

GenAI’s impact on B2B software

This narrative of revolutionary change underscores a critical shift. Companies are no longer just building AI into their products; they are actively rethinking pricing strategies to reflect its transformative potential. How can businesses align their pricing with the value that AI delivers, and what challenges must they navigate along the way?

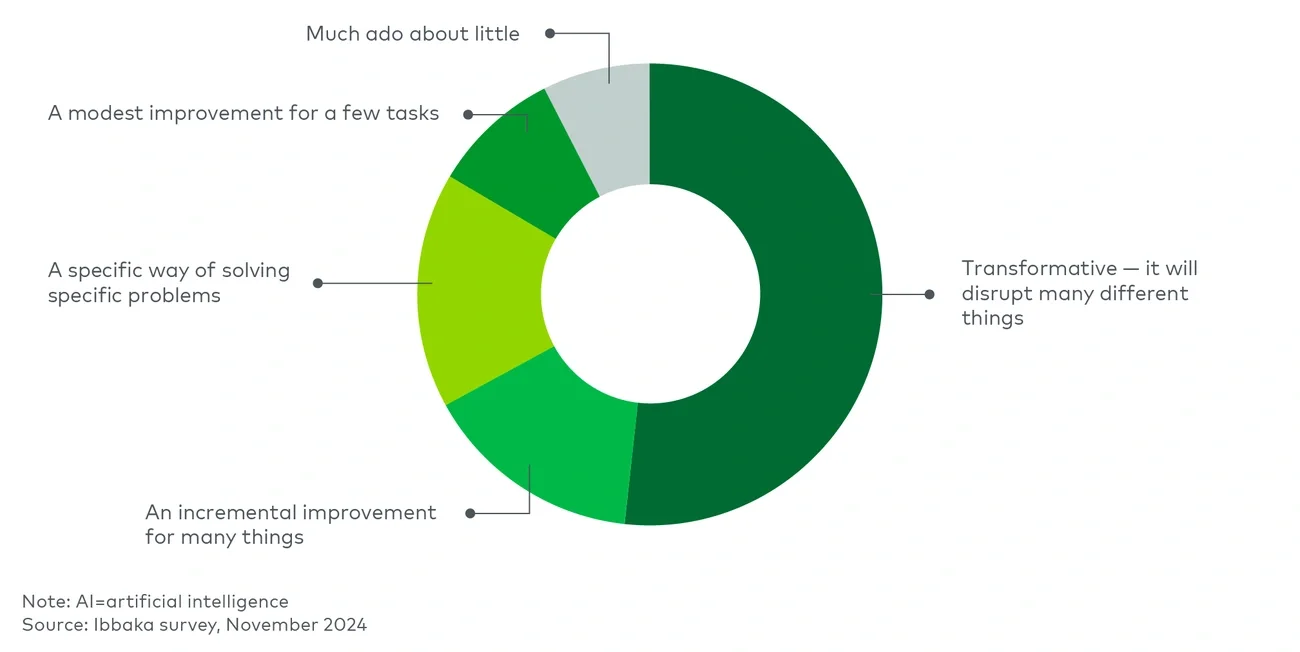

Industry attitudes toward AI reveal widespread enthusiasm, particularly among early adopters. Over half of respondents in a recent survey conducted by Ibbaka, a pricing and value management platform, believe GenAI will disrupt multiple domains, from product development to customer support and pricing (see Figure 2).

Figure 2

Over 50% of respondents believe AI is transformative across domains

This growing excitement has a direct impact on pricing strategies. GenAI isn’t just another feature — it represents a paradigm shift that demands innovative pricing models capable of capturing its unique value. Traditional subscription-based approaches are being challenged as software-as-a-service (SaaS) companies grapple with new ways to align costs with outcomes and usage.

GenAI is fundamentally reshaping the traditional relationship between pricing and usage. By enabling businesses to “do more with less,” AI challenges the relevance of seat-based pricing models while driving innovation in outcome-based, consumption-based and hybrid strategies.

Companies such as Zendesk are leading the way with hybrid approaches, charging per seat for human users and per resolved ticket for AI agents. This shift reflects a broader trend: SaaS companies are aligning their pricing strategies with the dynamic value AI delivers.

Outcome-based pricing ties costs directly to measurable results, offering a transparent and ROI-aligned approach. Examples include:

Advantages: Outcome-based pricing offers transparency by tying costs to success metrics such as resolved tickets and tasks completed. This alignment allows customers to perceive direct value from their spending.

Drawbacks: Attribution disputes can arise when outcomes involve multiple tools or manual inputs. Additionally, scalability can become challenging if success metrics are unclear or poorly calibrated.

Consumption-based models align pricing with resource usage, providing flexibility for businesses of varying sizes. Examples include:

Advantages: Consumption-based pricing is highly scalable and flexible, adapting seamlessly to customer usage patterns. It allows businesses to pay only for what they consume, reducing waste and maximizing efficiency.

Drawbacks: This model introduces revenue volatility, as usage can fluctuate unpredictably across customers and time. Customers also face the risk of unexpected cost spikes, requiring careful monitoring to avoid surprises.

Hybrid subscription models combine the stability of subscription fees with the adaptability of consumption- or outcome-based pricing. These models are particularly effective for AI-driven tools, capturing value from both predictable base fees and variable AI-powered usage. Examples include:

Advantages: Hybrid subscription models provide predictability through stable base fees while offering flexibility with variable charges for AI-powered features. This approach meets the needs of diverse customer segments, encouraging broader AI adoption.

Drawbacks: These models require sophisticated systems to track and manage both fixed and variable charges effectively. Customers may need education to understand the value proposition and navigate the model’s complexity.

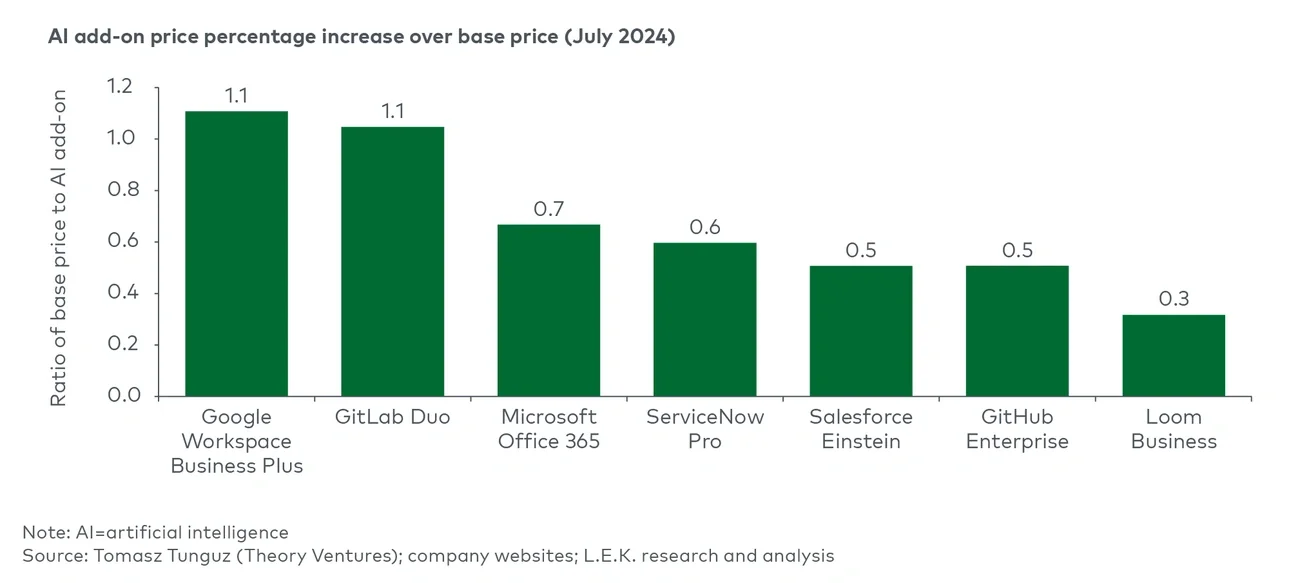

The growing trend of premium pricing for Copilot-style AI add-ons (AI features assist with tasks within existing user-centric software), ranging from 30%-110% above the base per-seat cost, underscores the growing value attributed to AI-driven productivity tools. This range reflects a strategic balance: Some companies prioritize usage with lower add-on prices, while others focus on monetization with higher premiums.

Examples such as Microsoft’s Copilot and Salesforce’s Einstein 1 highlight how hybrid pricing models blend predictable subscription revenue with flexible, usage-based components (see Figure 3).

Figure 3

Pricing model progression from traditional to AI-driven pricing models

GenAI is driving SaaS companies to innovate beyond traditional pricing models. By aligning strategies with AI’s transformative potential, these companies are better positioned to meet customer expectations and unlock new revenue streams.

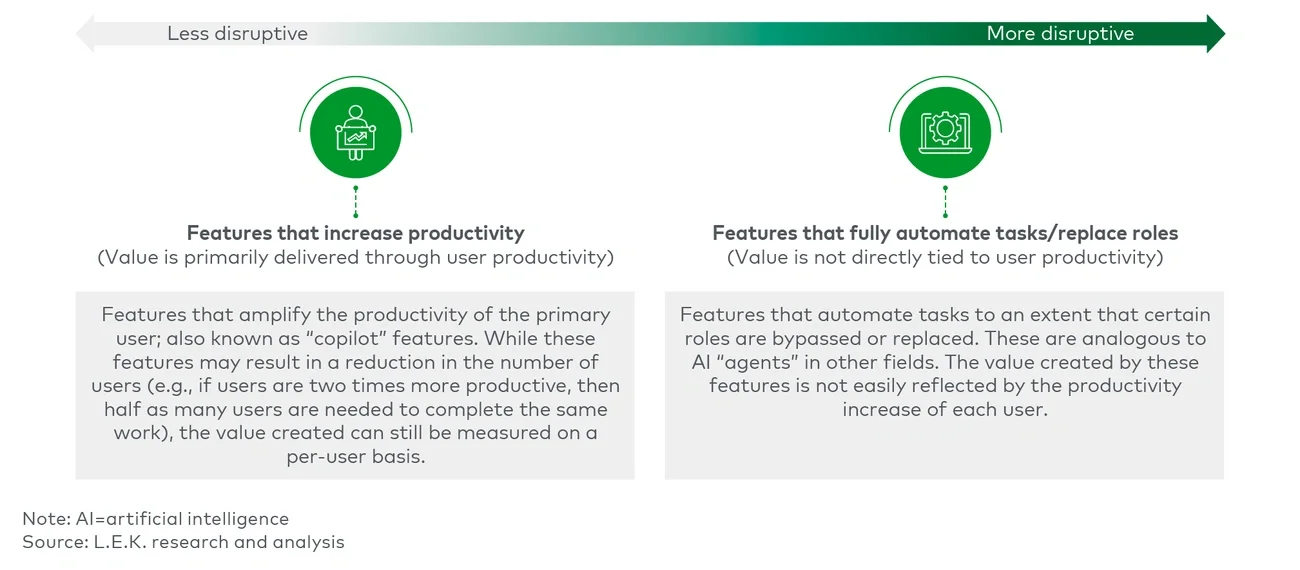

GenAI creates value in SaaS through two distinct approaches:

These benefits capture not only productivity improvements but also benefits such as reduced errors, faster workflows and better decision-making capabilities. As SaaS companies explore AI pricing models, they must distinguish between tools that enhance human productivity and those that fully automate processes to align costs with value (see Figure 4).

Figure 4

AI capability continuum

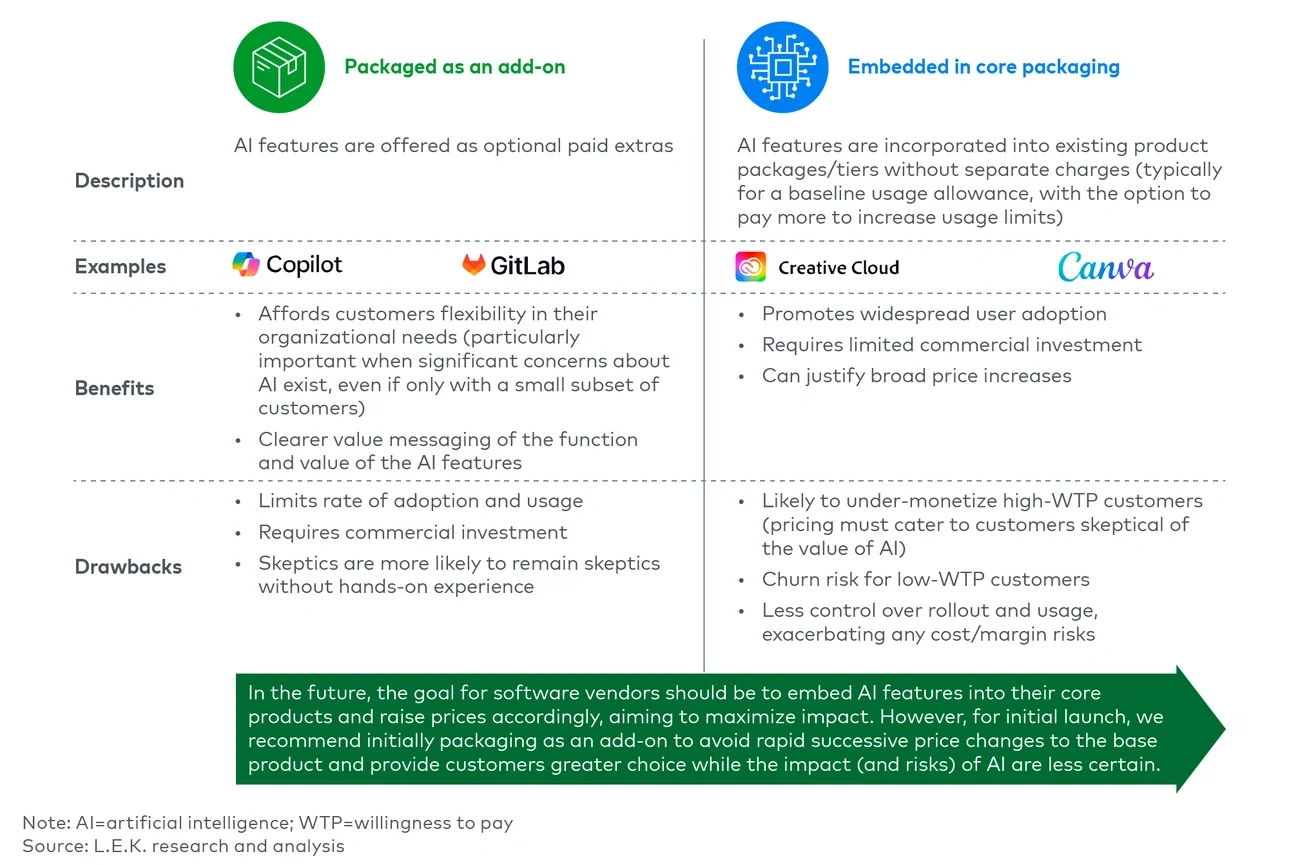

AI features that increase user productivity can be embedded into core products eventually and be initially packaged as an add-on to reduce complexity in the near term. This strategic choice shapes how companies introduce and monetize their AI capabilities (see Figure 5).

Figure 5

Strategic approaches to AI feature integration

GenAI shifts the focus from user-friendly interfaces to robust data architectures. With workflows increasingly handled by AI agents rather than human users, the emphasis is on structured, accessible data to support AI-driven decisions and operations. Companies such as Snowflake and Databricks, which excel in advanced data infrastructure, are well positioned for this shift.

As Jamin Ball, a venture capitalist investing in enterprise software businesses, notes, “The best end-user experience will come from a better underlying data architecture, not an easy-to-use UI. The leading application vendors today have become systems of record that workflows are built around. A system of record is just a database. And the workflows will be carried out by agents and API calls.” This shift fundamentally changes how we think about value creation in SaaS.

The integration of GenAI into SaaS products is driving a profound evolution in how companies approach pricing. Traditional models often fail to capture AI’s dynamic value, necessitating innovative strategies. This article is the first in L.E.K. Consulting’s four-part series exploring the future of SaaS pricing in the AI era. The remaining three topics are:

AI product packaging strategies: This article will examine approaches for incorporating AI into your product offering, from add-on features to fully integrated solutions. We’ll analyze how companies such as Microsoft, OpenAI and Synthesia structure their AI offerings and how different packaging decisions impact market adoption.

Pricing models for AI features: This article will explore pricing strategies for AI-enhanced products, from traditional licensing to usage-based models. We’ll examine how companies determine and implement value metrics across both horizontal applications (e.g., content generators) and vertical solutions (e.g., healthcare diagnostics).

The future of annual recurring revenue (ARR) and valuations with GenAI pricing: This article will examine how SaaS companies can rethink ARR in the context of variable revenue. It will discuss managing baseline and variable income, forecasting dynamic usage patterns, and evaluating AI’s impact on SaaS valuations.

GenAI is reshaping how SaaS companies deliver and monetize value. Innovative pricing models tied to outcomes and usage allow businesses to reflect AI’s transformative potential while meeting evolving customer expectations. Success in this shift requires balancing transparency, scalability and alignment with market needs. Companies that adapt to these changes will unlock new growth opportunities and solidify their positions in the competitive AI-driven landscape.

GenAI is compelling SaaS companies to innovate their pricing strategies, pushing beyond traditional models to reflect its transformative impact on value creation and delivery. For more on these topics, visit our in-depth perspectives on consumption-based pricing and outcome-based pricing to explore their advantages and challenges, hybrid approaches to these models, and real-world applications in detail.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

A fast-growing industrials manufacturer was facing persistent supply chain disruptions that threatened its operations. Late shipments, inconsistent quality and supplier failures were creating backlogs, straining customer relationships and putting revenue at risk. At the center of the issue was a critical rotomolded plastic component ― essential for product quality ― sourced from an external supplier struggling to meet demand.

Recognizing the need for greater control, the company engaged L.E.K. Consulting to assess the feasibility of in-sourcing production. The goal was to determine operational requirements, assess financial viability and build a compelling business case for investment.

We conducted a comprehensive, data-driven assessment to ensure the transition to in-sourcing was both financially feasible and operationally sound. We worked collaboratively with the client in establishing a baseline, identifying key operational considerations, modelling implications and developing a roadmap for success:

Our strategic guidance provided the manufacturer with the confidence and clarity to proceed. Expected results include:

By addressing supply chain weaknesses with a structured, data-driven strategy, the manufacturer transformed a recurring challenge into a long-term competitive advantage. With greater control over production, improved efficiency and reduced risk, the company positioned itself for sustainable, cost-effective growth.

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC

The recruitment industry is undergoing a profound transformation as AI, advanced analytics and digital platforms reshape traditional practices. However, human value isn’t diminishing: these innovations accentuate it, freeing advisers from repetitive tasks and empowering them to focus on strategic counsel, cultural alignment and long-term talent development.

In an era of ubiquitous talent visibility, the real differentiator lies not in identifying candidates, but in ensuring that chosen leaders thrive within their organisations.

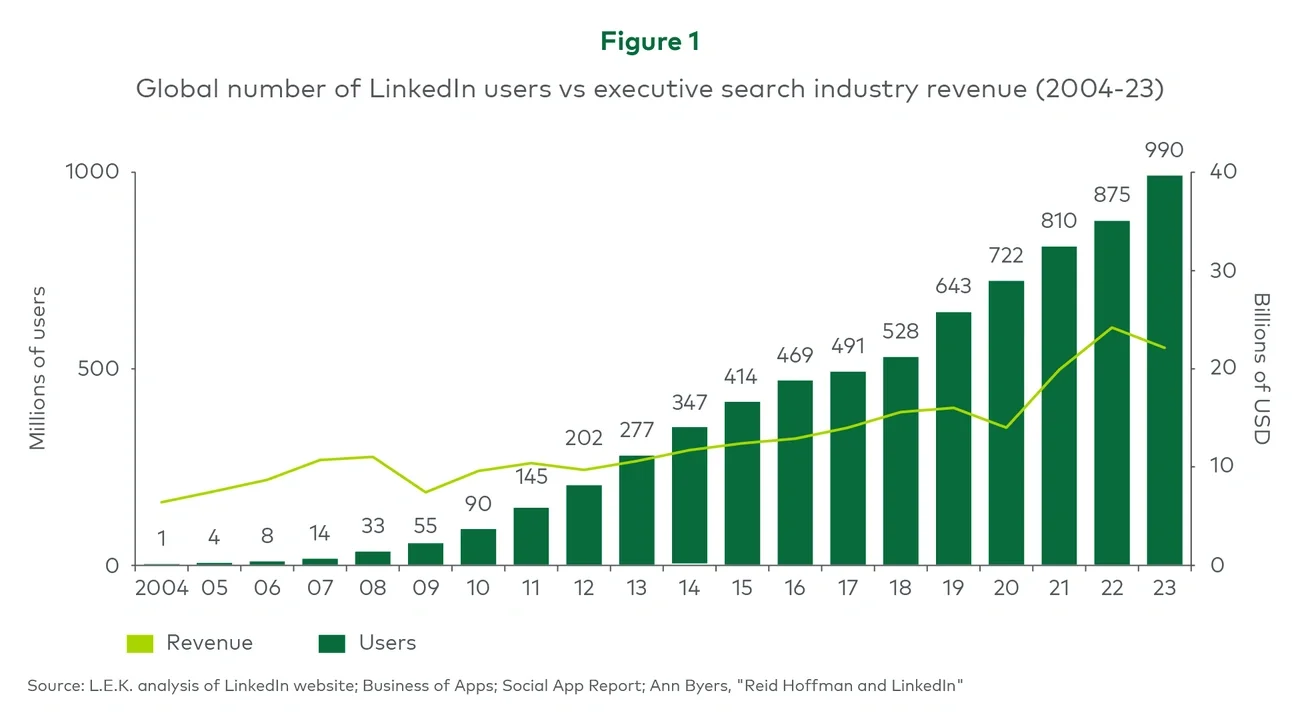

When LinkedIn and similar platforms emerged, they dramatically increased talent visibility. Over time, LinkedIn’s user base rose from a few million to nearly a billion, making it easier to find candidates. Many expected this to erode the talent search model. Instead, global search revenues grew as well (see Figure 1).

Identifying raw talent was no longer the challenge; interpreting context, ensuring cultural fit and providing strategic reassurance remained indispensable. Technology made discovery universal, but human judgement still determined whether people would actually succeed in their roles.

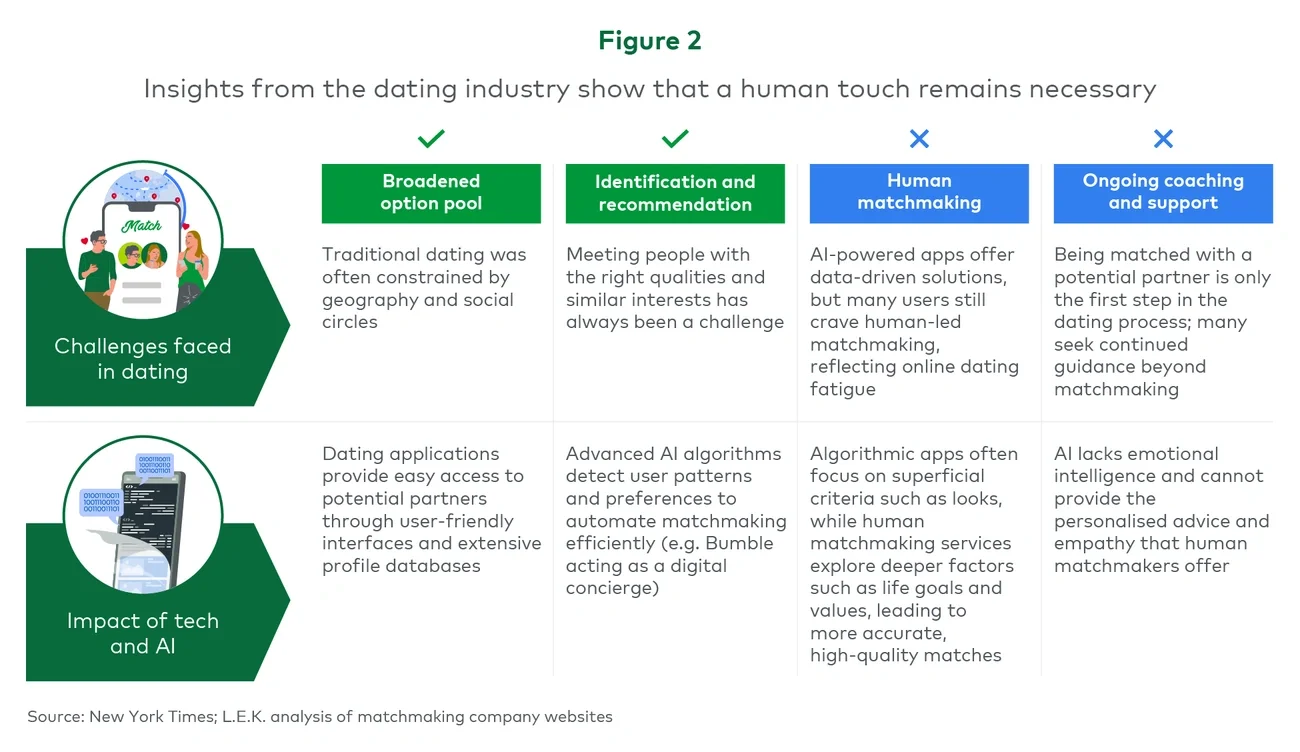

Online dating platforms show a similar pattern. Algorithms broaden the pool of potential matches and suggest likely fits, akin to how AI assists in initial candidate filtering. Yet people still seek empathy, intuition and personal understanding to form meaningful connections.

Similarly, while AI-driven recruitment tools handle initial screening and recommendations, organisations rely on human advisers to interpret intangible qualities like leadership potential, cultural compatibility and long-term impact. Technology refines the options; human insight ensures enduring alignment (see Figure 2).

Automation significantly impacts high-volume recruitment, where large candidate pools benefit from rapid, algorithmic filtering. By contrast, senior executive and board-level searches remain deeply relationship driven. These roles depend on discretion, trusted networks and the nuanced evaluation of leadership qualities that algorithms cannot fully capture.

However, AI is playing a growing role in leadership assessment and candidate benchmarking, enhancing the process rather than replacing human judgement. At this level, technology assists with data gathering and initial assessments, but the final decision still hinges on an adviser’s ability to align talent with strategic priorities, cultural fit and long-term organisational success.

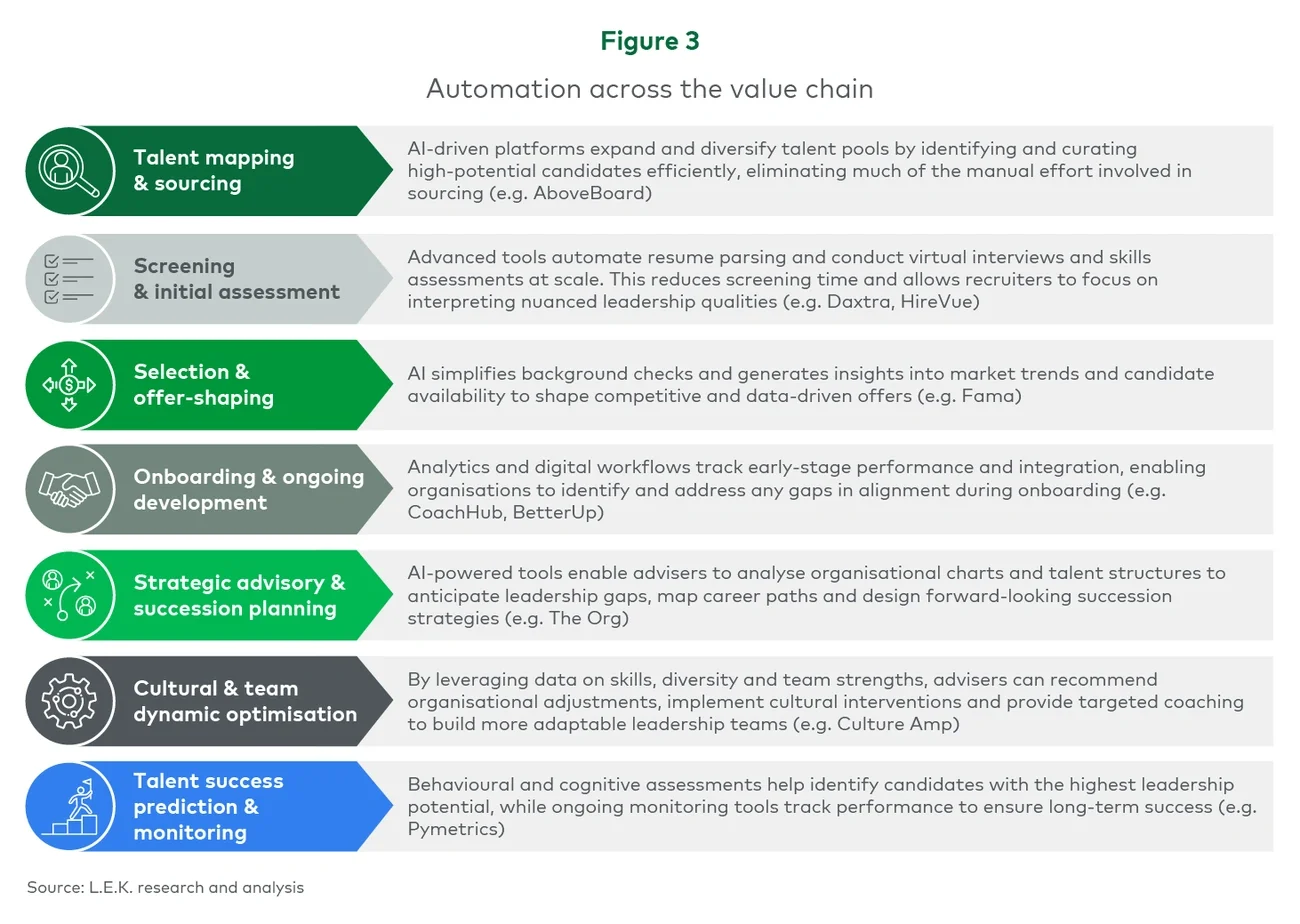

Recruitment comprises multiple steps: mapping talent markets, screening candidates, shaping offers and nurturing long-term development. As technology touches each phase, it automates routine tasks and injects data-driven rigor, allowing advisers to concentrate on strategic guidance, cultural alignment and forward-looking leadership planning.

In this expanded model, technology underpins not only efficiency but also strategic foresight and long-term organisational health. Recruiters move from reactive problem-solvers to proactive architects of leadership ecosystems (see Figure 3).

Meanwhile, in-house teams are becoming more capable of leveraging the same technology. Many searches, especially at mid-levels, can now be handled efficiently and cost-effectively in-house.

“In-house teams are a huge threat,” noted one industry leader, “you can hire a Head of Talent and pay them the equivalent of one search with an external company, so in-house you could even do five searches for the price of one.”

However, in-house teams face clear limitations when it comes to the most complex and high-stakes leadership appointments. Senior roles often require discretion, external market benchmarks and the nuanced assessment of leadership fit that external advisers provide. As one executive observed, “those teams would never do board of directors or CEO search […] it’s relationship driven and AI won’t replace that.”

Technology is narrowing the capability gap between in-house teams and external search firms, enabling internal recruiters to handle more searches autonomously. However, for highly specialised or sensitive leadership hires, many organisations continue to partner with external advisers who provide market intelligence, benchmarking data and discreet candidate outreach. External firms will also have wider networks, especially over time as the in-house team’s Rolodex goes stale.

The way recruiters create value is changing – narrowing in recruitment and broadening into other related services. The infusion of AI, analytics and digital platforms doesn’t overshadow human skill. Instead, it highlights what exceptional advisers do best: interpret subtle signals, align hires with broader strategic goals and nurture leadership talent for sustained impact.

By streamlining the transactional elements of recruitment, technology creates space for deeper engagement, helping recruiters guide clients through complex decisions and shape leadership teams that endure and evolve.

Far from becoming obsolete, advisers who embrace technology become more valuable partners. They focus on what truly differentiates top-tier recruitment: cultural insight, strategic alignment and the long-term viability of chosen leaders.

In this new landscape, human expertise and AI-enabled efficiency form a powerful combination that leads to stronger, more resilient organisations. To find out more, please contact one of the team.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2025 L.E.K. Consulting LLC