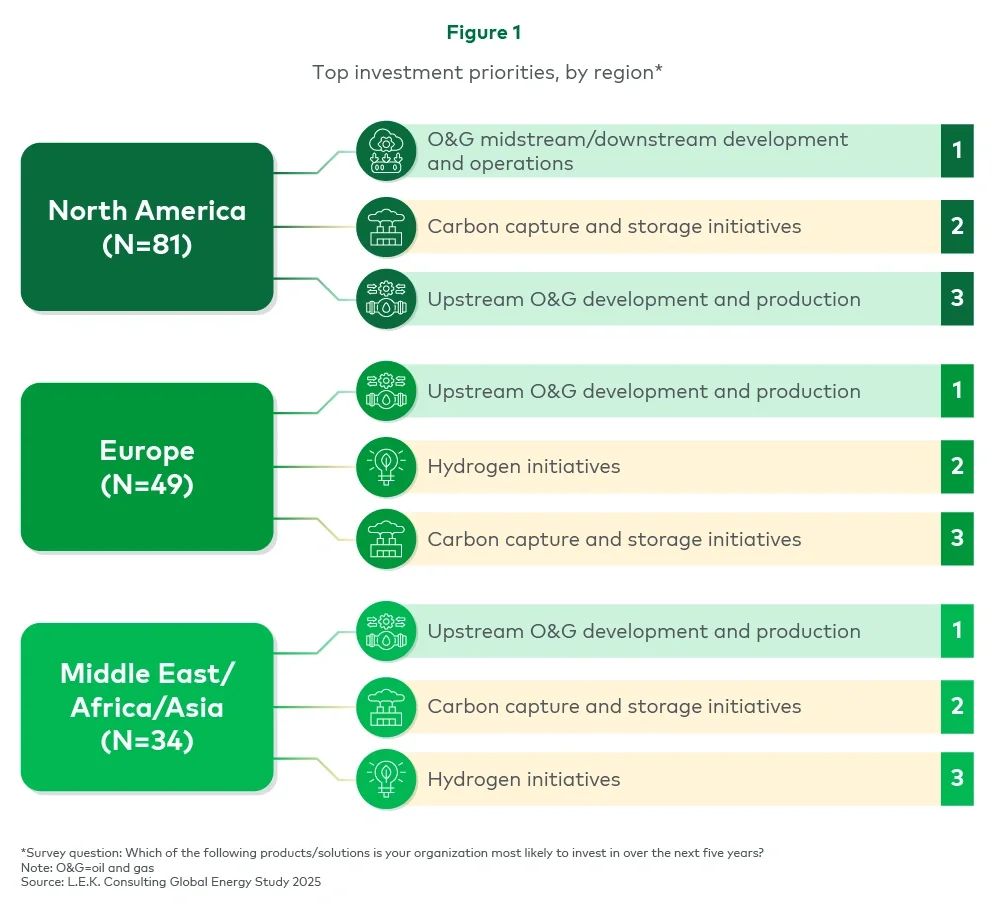

Renewables: Growth meets reality

Renewables developers remain the most growth-oriented group, but their confidence is tempered by policy uncertainty and rising costs.

Supportive policies in Europe, and generation needs in the U.S., continue to attract investment, yet permitting constraints, tariffs and supply-chain inflation have raised barriers. The outlook remains constructive for solar, storage and onshore wind, but developers acknowledge that commercial discipline now matters as much as policy support.

Gas and grid: Flexibility becomes the bridge

Natural gas continues to underpin system reliability and remains critical to the energy transition. Eighty percent of energy executives view gas as indispensable to the renewables transition, providing dispatchable backup for intermittent generation.

However, constraints are mounting. Only 22% of utilities express strong confidence that sufficient gas-fired power build-out will be achievable under current conditions, while 58% say a significant investment in gas infrastructure is required to meet the demand.

The result is a pragmatic response: BTM gas solutions are scaling rapidly as a bridge for power-intensive users such as data centers. Nearly half of new data center megawatts are expected to be powered off grid by 2030, mostly as temporary (less than two-year) solutions, though some may stay on longer depending on local interconnection costs and power prices. But BTM is too subject to potential constraints on equipment availability, and penetration growth will require a mix of solutions (e.g., turbines, reciprocating generators and fuel cells) to be available.

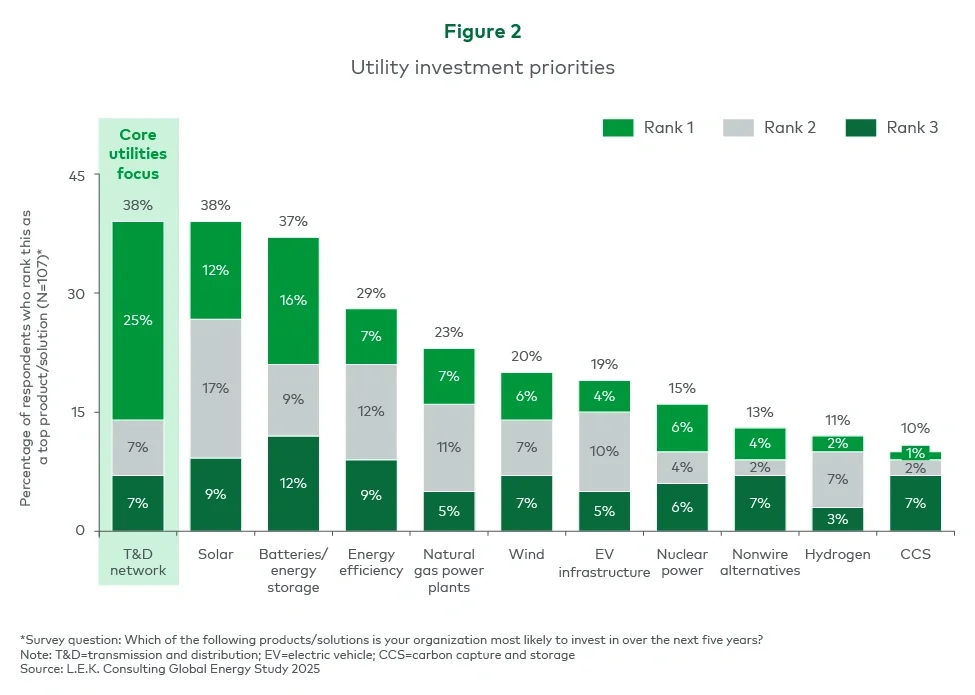

AI moves from pilot to performance

AI is shifting from the lab to the field. More than 60% of utilities now use AI for demand forecasting and 53% for predictive maintenance, while over half of O&G companies deploy it for performance analytics and downtime reduction.

Yet most firms acknowledge they are only scratching the surface, with data quality, return on investment measurement and governance continuing to pose challenges. Even so, 80% of energy leaders expect to achieve full value realization from AI within the next decade — a notably confident view given the sector’s current implementation maturity.

The message is clear: Scaling AI will depend on embedding it into operational decision-making, not treating it as a stand-alone digital experiment.

Navigating energy’s next phase

The global energy sector is entering a phase where execution precision defines progress. Each segment faces distinct pressures, but all share a common challenge: balancing investment discipline with the urgency to modernize and decarbonize.

What unites them is a pragmatic approach. Growth continues, but selectively. Capital flows, but toward proven solutions. Innovation advances, but with a focus on performance and resilience.

How L.E.K. can help

Our teams advise energy leaders on where to invest, how to build resilient infrastructure and when to accelerate transition bets. L.E.K.’s 2025 Global Energy Study provides the data and insight; our consulting expertise helps clients translate these findings into decisions that create value today and secure a position for tomorrow.

For more details on the full study or to learn how these insights apply to your business, please contact our global energy team.