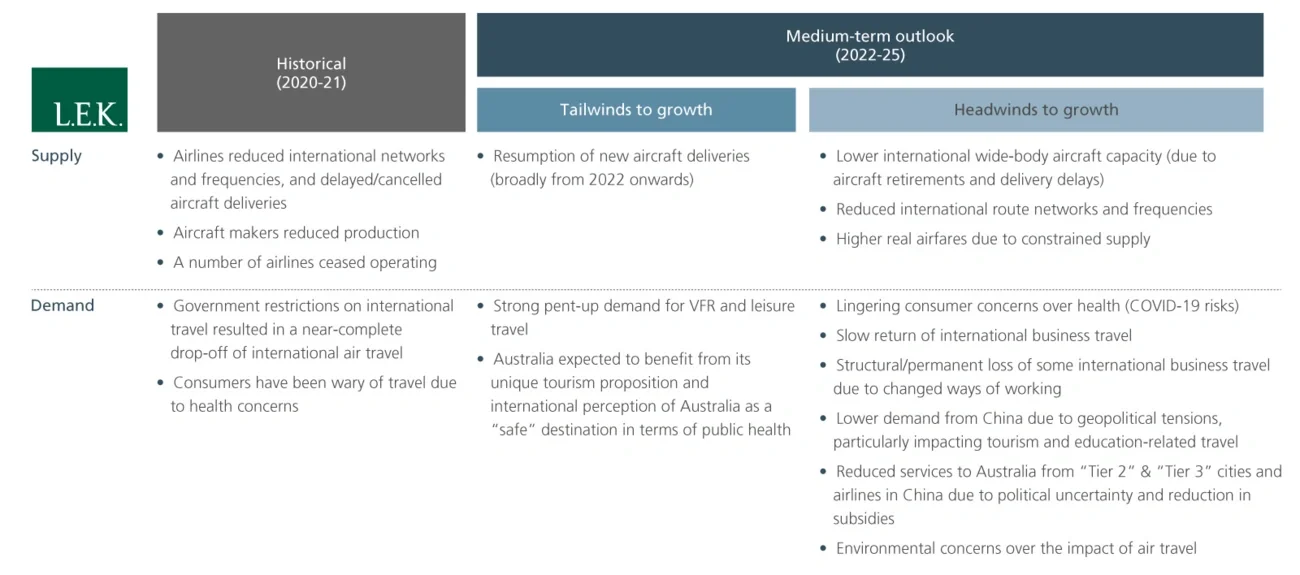

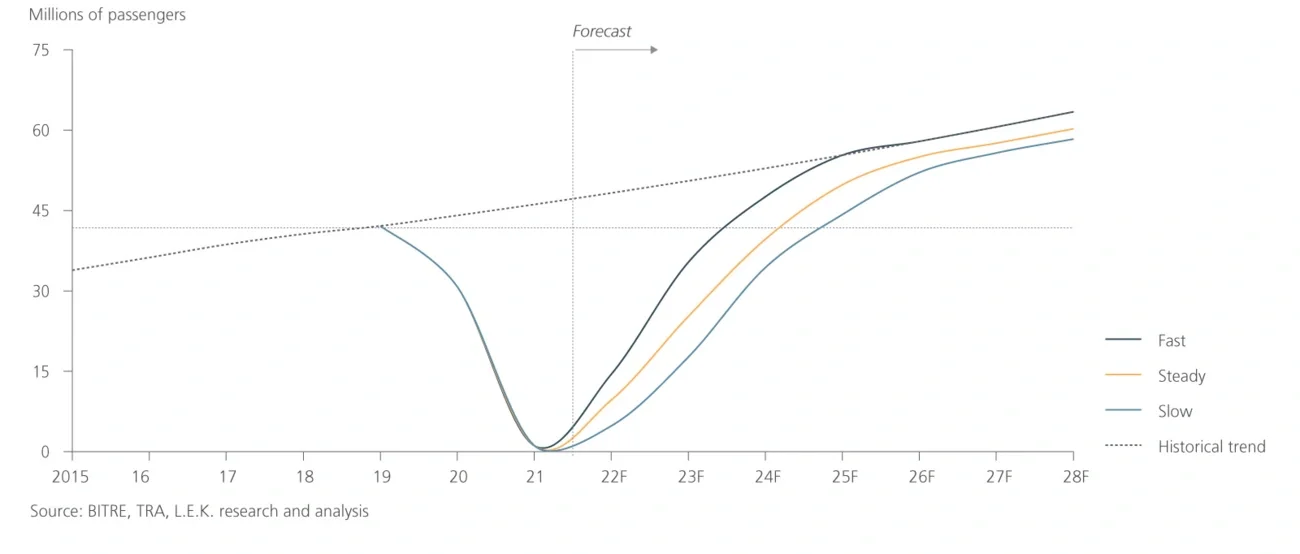

Demand for air travel

There is evidence of significant pent-up demand for international air travel to and from Australia, particularly for visiting friends and relatives (VFR) and leisure travel. Consumer research indicates the outbound traveller segment will be first to return as the Commonwealth and state/territory governments relax restrictions on Australians travelling overseas.

A recent L.E.K. consumer survey indicated that most Australians, particularly VFR travellers and younger cohorts, plan to take more international trips post-COVID-19 than they did pre-COVID-19, in part to “make up for lost time”. However, in the near term some traveller segments (e.g. older travellers) may delay a return to international travel due to health concerns and the greater complexity/cost of travel.

Inbound visitation to Australia will be slower to return, but the key underlying macro demand drivers (e.g. GDP, population growth, VFR travel to Australia, interest in Australian holidays) are expected to remain supportive of growth. Traveller surveys continue to indicate strong interest in visiting Australia as a unique location that has developed a reputation as a “safe” — albeit restrictive — destination during the pandemic.

The speed of recovery for international inbound visitor traffic will be dependent on government restrictions on entry and quarantine, and we assume that full vaccination will be an entry requirement for non-Australian citizens/residents.

VFR will be the first inbound market to return, followed by inbound leisure/holiday travel. Amongst Australia’s largest VFR and leisure markets, New Zealand, the UK, the US, China, Singapore and Japan have made good progress with their vaccination programs, with between 50% and 80% of their populations vaccinated. However, the likes of India, Vietnam and the Philippines have lagged behind, suggesting that reopening to these markets will take longer.

International business travel will be slower to return and will be dependent on corporate/business decisions on budget, employee health and safety, and on the risk of being caught out by changing government travel restrictions. It will also be driven by the return of conventions and other large-format gatherings.

Business surveys suggest that there could be a medium-term structural impact on international business travel as a result of changed ways of working (i.e. videoconferencing), as well as a near-term impact based on business risk assessments related to health and changing border restrictions.

There is also a potential medium-term structural impact related to Australia’s political relationship with China, with broad implications for the VFR, leisure, business and education traveller segments.

Supply of aviation capacity

From a supply-side perspective, the international capacity of Australian carriers was materially reduced during the pandemic. Virgin removed all 11 wide-body aircraft from its fleet (B777s and A330s), although the airline can continue to operate short-haul international flights to New Zealand and parts of Asia with its fleet of 737-800s. Qantas currently has c.11% fewer wide-body aircraft in its fleet versus in January 2020, driven by early retirement of six B747s. At present, Qantas has announced plans to reactivate only five of its 12 A380s in 2022, with two of the 12 to be retired and the remaining five to remain in storage. Like Virgin, the Qantas Group (inclusive of Jetstar), has narrow-body aircraft (B737s and A320s) that can serve New Zealand and parts of Asia.

The bigger supply risk to the Australian international market is the potential loss of frequency, capacity and destinations provided pre-COVID-19 by international carriers, which account for the majority of international capacity to and from Australia. International airlines will return services to Australia as travel restrictions ease, but they will likely operate with lower frequencies and capacities in the near term across all Australian destinations.

There is also a risk of reduced services to Australia from “tier 2” and “tier 3” Chinese cities facilitated by Chinese airlines due to political uncertainty and reduction in subsidies.

Constrained aviation capacity in the short- to medium-term will likely lead to higher real airfares, which could act as a drag on demand for international air travel.

However, in a positive sign for aviation capacity, airlines — both international carriers and the Qantas Group — should see a resumption of new wide-body aircraft deliveries in 2022, which will begin the process of returning fleets to their pre-COVID-19 sizes.

The figure below summarises these impacts: