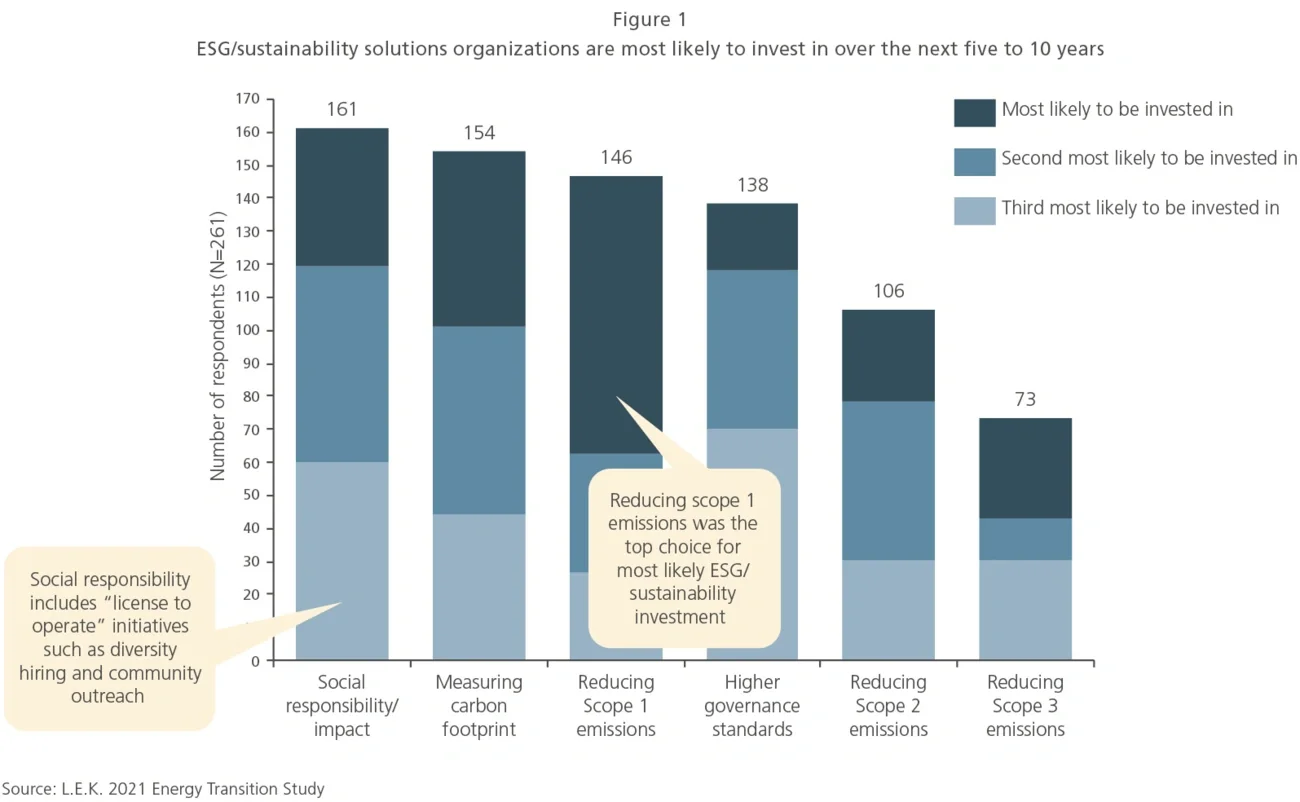

The most common choice is social responsibility and impact. This includes “license to operate” initiatives such as diversity hiring and community outreach, and a majority (62%) of respondents put this one on their top-three list. Oil and gas companies have a long history of supporting social impact across global footprints where community-building initiatives are an operational imperative. The study data suggests that through a continued oil and gas focus, social issues remain the top priority as well.

Reducing Scope 1 emissions is more likely than any other solution to be a number-one priority, and, while Scope 3 emissions appear less important today, momentum may be gaining. Although 56% of respondents identify reducing Scope 1 emissions as a top-three priority, most of that group put it at the head of their list. It’s also more of an issue for exploration and production (E&P) and oil-field services and equipment (OFSE), judging from these results: 24% of majors, 25% of nonmajors and 17% of OFSE companies identify Scope 1 emissions reduction as a priority. It doesn’t make the top three for any of the midstream and downstream companies or investor and financial entities represented in the survey. While Scope 3 emissions is a distant sixth overall for the most likely area to be invested in, it’s the fourth highest ranked among respondents’ top “most likely to be invested in” areas (see Figure 1). This difference may suggest there is a subset of companies that believe more effort must be invested in Scope 3 to mitigate the risk of being caught off guard if this becomes as important to investors and stakeholders as Scope 1 is suddenly today.

We have one more key finding to highlight from our energy transition study. While the oil and gas industry is largely moving in the same direction, there are contrarian views around prioritization, pace of change and technology. We’ll address those views in the next and final article of this series.