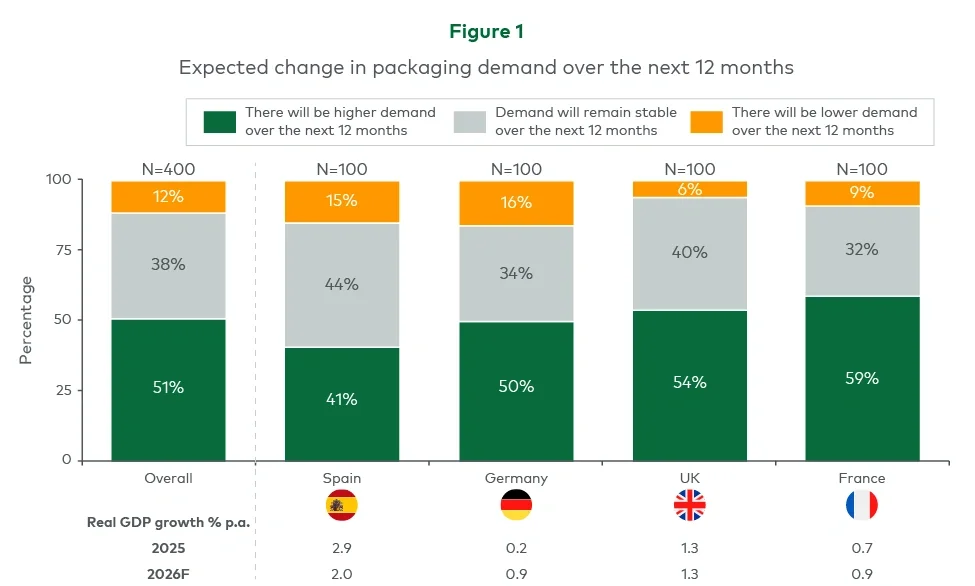

The recovery is also uneven across geographies. France and the UK show relatively stronger momentum, while Germany and Spain remain more cautious. These differences reflect broader economic divergence as well as variation in category mix and consumer demand resilience.

Demand recovery is underway, but remains constrained

The current demand outlook reflects a market transitioning from volatility to stability. The sharp fluctuations seen during recent years, driven by pandemic effects, supply chain disruption and inflation, have largely subsided. However, the underlying growth profile remains modest.

Two factors are shaping this environment. First, macroeconomic conditions continue to weigh on consumption in several key markets. Second, overcapacity across parts of the packaging value chain is limiting the extent to which volume growth translates into improved utilisation and pricing.

As a result, the near-term outlook is best characterised as stabilisation rather than expansion. Growth is returning, but at a measured pace and with limited visibility on sustained acceleration.

Category growth is diverging

Demand expectations vary significantly by end market. Beauty and personal care is the standout category, with 68% of brand owners expecting demand to increase over the next 12 months. Beverage and healthcare, pharma and wellness also remain relatively robust, both at 55%. At the other end of the spectrum, food and foodservice is more subdued at 45%, while household and pet food appears weakest, with only 33% expecting growth.

These differences reflect underlying category dynamics. Higher-growth segments tend to combine innovation intensity, premiumisation opportunities and stronger consumer demand resilience. More mature categories, particularly those exposed to price-sensitive consumers, face slower recovery and greater pressure on volumes.

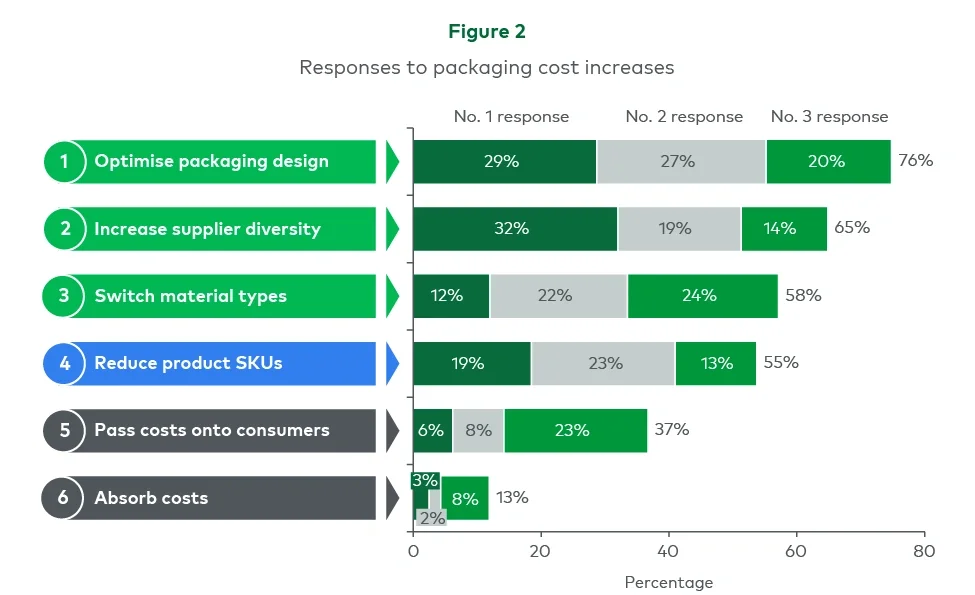

Beyond category dynamics, cost pressures continue to shape packaging decisions, even as demand stabilises. Around 69% of European brand owners expect packaging costs to increase over the next year, reinforcing the persistence of inflationary pressure across materials and supply chains.

However, the primary response is not to absorb or pass through these increases, but to adjust packaging itself. Most respondents prioritise packaging design optimisation, alongside actions such as supplier diversification and material substitution (see Figure 2).

While cost pass-through remains part of the toolkit, its effectiveness is increasingly constrained. Consumer pricing has risen materially in recent years, outpacing income growth in many markets. As a result, retailers are under pressure to maintain price competitiveness and are pushing cost increases back through the value chain.

This design-led approach marks a clear distinction from the US, where brand owners are more likely to rely on pricing actions. In Europe, packaging is increasingly treated as a controllable lever within the cost base, with less reliance on pass-through as the primary mechanism for managing cost increases.