The payments industry is entering a period of structural change in which multiple forces are reshaping economics, distribution and operating models. The foundations of how money moves, how value is created and how risk is managed are being rearchitected simultaneously. Intelligent and agentic commerce is reshaping discovery, conversion and operations as software is increasingly mediating decisions that were once made by humans. Embedded ecosystems are reorganizing how financial products are distributed and consumed. Real-time and programmable money are compressing cash cycles and altering segment-level economics. Trust is evolving from a control function into a potentially differentiated, monetizable layer. And legal and regulatory shifts are increasingly reshaping the economic boundaries of the system.

What makes this moment distinctive is not the presence of these forces individually, but the way they interact. Decisions made in one domain increasingly constrain or amplify options in others. As a result, payments strategy is becoming less about optimizing isolated initiatives and more about designing an enterprise that can adapt, scale and compete across interconnected shifts.

Payments leaders are increasingly turning their attention from simply improving their organizations toward architecting enterprises capable of expanding into new segments, scaling through partners, monetizing trust, and operating with reliability and control at real-time speed. Doing so requires a clearer view of where strategic pressure is building and where uncertainty is highest.

This anchor publication from L.E.K. Consulting introduces the CEO Strategy Matrix, a framework designed to help executive teams navigate this complexity. The matrix surfaces where core strategic imperatives intersect with structural market forces and where unresolved questions are emerging that demand chief executive officer (CEO)-level attention.

The paper does not attempt to provide a single definitive answer across the matrix — as with any thoughtful strategy, the path each firm chooses to navigate the matrix will be unique to its own point of departure and capabilities. Instead, we lay out the landscape and explore a set of intersections where we see growing strategic tension and leadership uncertainty. These areas will be the focus of continued research and follow-on analysis in the months ahead as we test how firms are responding and where competitive advantage is beginning to form.

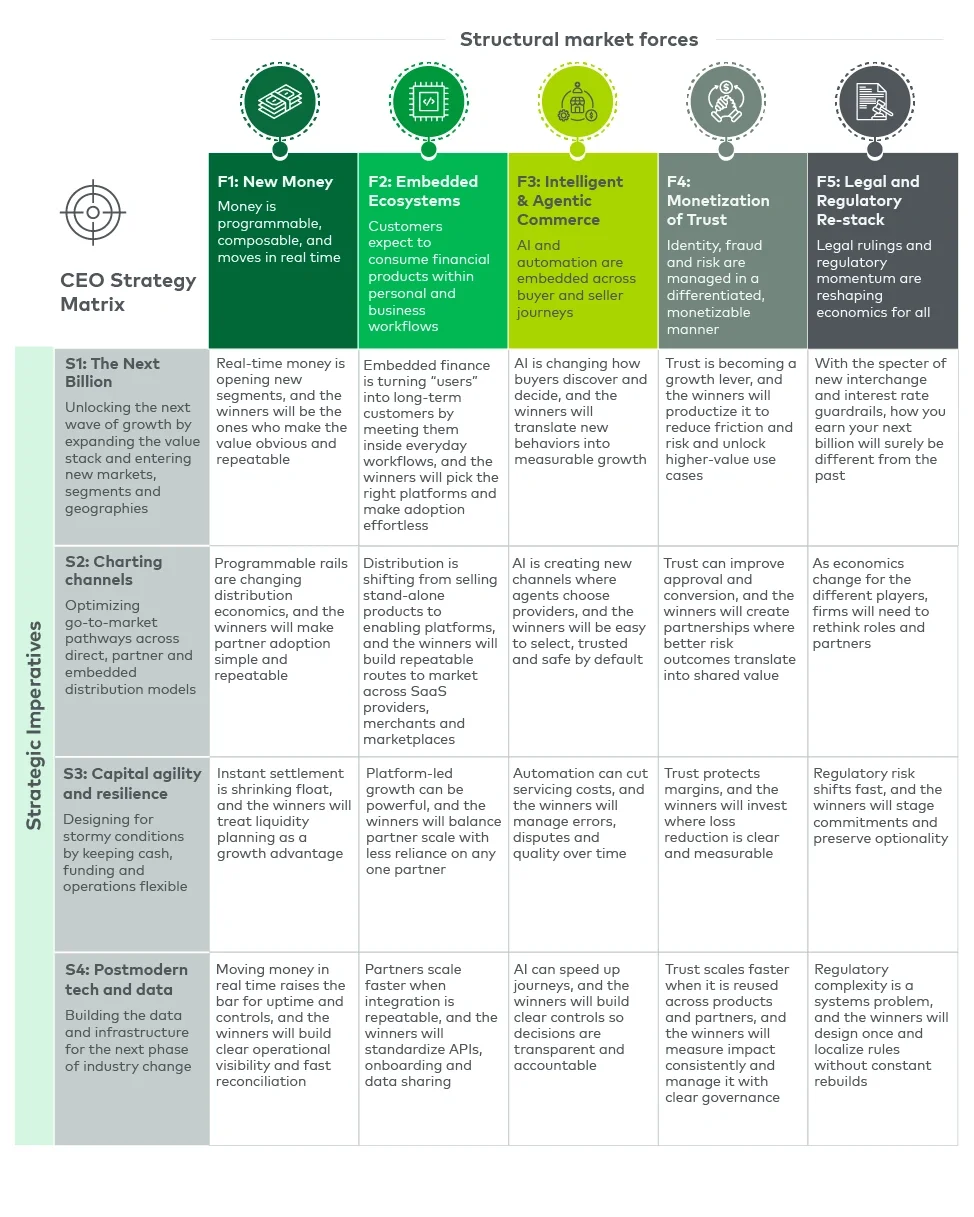

Introducing the CEO Strategy Matrix

We built the CEO Strategy Matrix as a way to translate broad market forces into an actionable executive agenda. The matrix explores the intersection of five market forces and four strategic imperatives to highlight where CEO-level trade-offs are concentrating. Each intersection represents a distinct set of strategic questions. At any given moment, only a subset of intersections will exert meaningful pressure on leadership teams, and these priorities will vary by business model, geography and starting position.

In this anchor paper, we highlight five of the intersections where early signals point to the greatest opportunity for durable advantage and the most consequential strategic choices facing CEOs’ teams today. These sections are intended to frame the questions, tensions and enterprise design considerations that CEOs and their leadership teams are beginning to confront. They also establish the agenda for subsequent research, which will deepen the analysis and surface clearer points of view as evidence emerges.