Why this matters now for productivity

A broker model can lift national productivity through five channels:

- Scale effects and reduced duplication: Consolidating fragmented services into shared ‘utility layers’ (i.e. common infrastructure, platforms, software and services) captures scale economies and reduces duplicated build and run costs.

- Life cycle optimisation: Under the right contract structures, private operators bring continuous improvement, specialised capability, life cycle maintenance discipline and sharper accountability for uptime and customer experience. This is a function of incentives, contestability and managerial focus, not ideology.

- Faster capital mobilisation: Well-structured concession/managed service pipelines attract long-dated private capital (super funds, infrastructure funds) and accelerate investment. Valuations and investor interest can increase further when transactions are structured to allow adjacent commercial upside (e.g. multi-tenancy, incremental capacity sales, value-add services) in alignment with policy settings and public interest, where applicable.

- Effective utilisation of existing assets: Private finance can boost productivity not just through new infrastructure but also by improving how existing assets are used. Asset recycling unlocks capital for higher-value projects, while better pricing (e.g. congestion charging) and private-sector expertise can improve efficiency, reliability and performance.

- Mission focus inside the government: The government can redeploy scarce public capital into other priorities that are non-contestable and concentrate on government policy, stewardship, regulation, risk management and assurance of equitable access. This capital redeployment could in turn be directed to other initiatives that either directly or indirectly help national productivity.

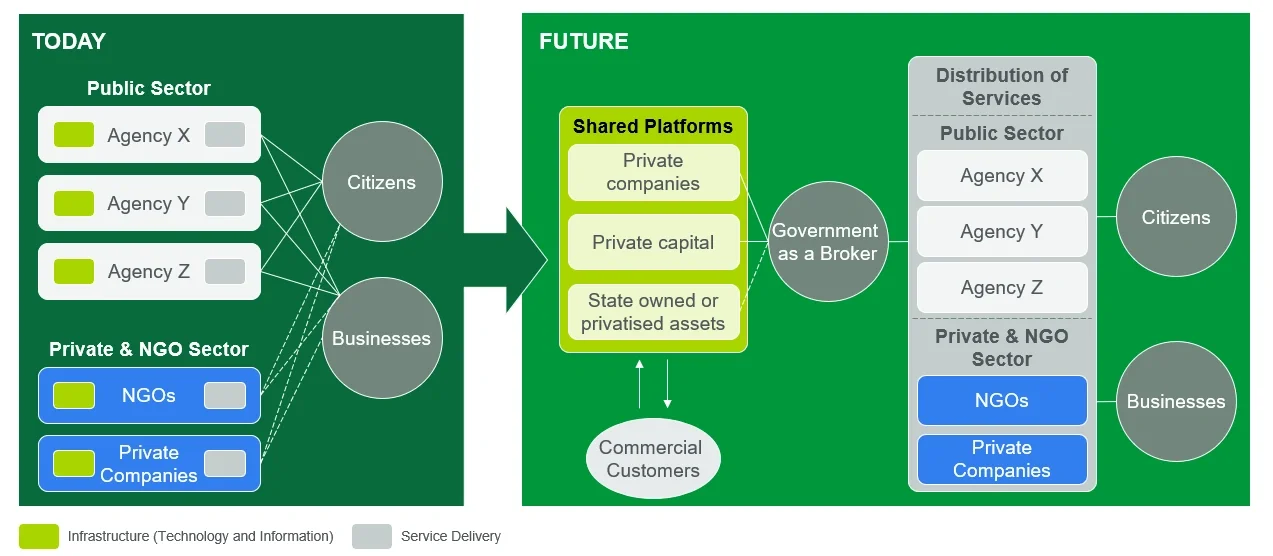

The opportunities are greatest where governments are sitting on asset portfolios with latent commercial and operational value and where underinvestment risks becoming a permanent drag on service outcomes and economic efficiency.

A carve-out pipeline beyond ‘traditional PPPs’

Australia already understands PPPs in transport and some social infrastructure. The next wave is likely to come from a broader pipeline of separable bundles, such as:

- Digital and operational utilities: Managed service or concession models with tight sovereignty controls to deliver shared platforms, transaction processing, identity, payments and shared service operations

- Property and precinct portfolios: Government estates bundled for life cycle upgrades and operations, where service outcomes can be specified cleanly

- Networks and maintenance programmes: Portfolio-based concessions where performance can be measured and enforced

- Specialist infrastructure: Where a layer is separated, scaled and professionally run on behalf of the government

The objective is to bundle assets to achieve investable scale, standardise contracting and build a repeatable programme rather than one-off deals.

The call to action

Australia’s productivity challenge will not be solved by a single reform lever, but a broker model is attractive for the government because it is actionable, scalable and aligned with the realities of fiscal pressure and rising service demand. The path forward is to identify a pipeline of carve-out and concession candidates, bundle them for scale and execute with a strong commissioning and assurance model.

Australia has examples that show this can work in specialist infrastructure such as broadcast transmission as well as international precedents that show how to apply the same logic to modern digital utilities, including data centre capacity and hosting. The opportunity is to apply the approach more broadly – redeploy capital, professionalise operations and lift the productivity of service delivery across the public domain. Brokering capital through repeatable concession/PPP programmes can mobilise private financing and operating capability while allowing the government to redeploy scarce public capital into genuinely non-contestable priorities.

Case study 1: Australia’s broadcast transmission

Broadcast transmission is a classic utility layer with high fixed costs, specialist engineering capability, strong economies of scale and natural multi-tenant economics.

The commonwealth created a legislative pathway for the transfer/sale of national broadcast transmission assets through the National Transmission Network Sale Act 1998. Over time, the market evolved towards specialist private ownership and operation, with BAI Communications (formerly Broadcast Australia) now operating a large national footprint of transmission sites and providing services to major broadcasters.

Two features make this a useful template for today’s productivity discussion:

- A specialist operator can run the asset base as an integrated portfolio, investing in resilience and maintenance with a whole-of-life lens rather than annual budget constraints.

- Multi-tenant economics allow the same physical infrastructure to support multiple users, spreading cost and lifting utilisation – a direct productivity mechanism for infrastructure.

Hence, Australia has already demonstrated the feasibility of carving out a non-core but essential infrastructure layer in a structure that supports professionalised operations and investment discipline.

Case study 2: The UK’s Crown Hosting model

Digital infrastructure is where the broker model can deliver outsized gains. A good reference point is the UK’s Crown Hosting initiative.

In 2015, the UK government established Crown Hosting Data Centres as a joint venture with Ark Data Centres to provide data centre capacity for government workloads that were not yet suited to the public cloud. The objective was to break the pattern of departments buying and renewing hosting in isolation, often on subscale, long-duration, difficult-to-exit contracts. The model sought to aggregate demand, industrialise pricing and service levels, and allow the government to transition legacy workloads in a structured way rather than as a series of bespoke renegotiations.

Australia’s own trajectory points in a similar direction. One strand is the growth of sovereign and high-assurance private data centre capacity serving the government. For example, the Department of Foreign Affairs and Trade’s partnership with Canberra Data Centres was framed explicitly as an uplift in information and communications technology capability and modernisation.

Case study 3: National Cancer Screening Register

Health registries are a prime example of ‘digital utility’ infrastructure. They sit behind essential public programs, combining data aggregation, workflow orchestration, provider interfaces and reporting at national scale. Australia’s National Cancer Screening Register (NCSR) illustrates the productivity and service upside of treating registries as shared infrastructure rather than fragmented, jurisdiction-by-jurisdiction systems.

In 2016, the Australian Government awarded Telstra Health the contract to implement and operate the NCSR, supporting the National Cervical Screening Program and the National Bowel Cancer Screening Program. The platform consolidated multiple legacy registers into a single national participant record and introduced more standardised digital channels for providers to access and submit screening information. The consolidation reduces duplication, scale supports stronger operating discipline and continuous improvement, and government can focus on stewardship, standards and assurance while a specialist operator runs the service under enforceable performance and privacy requirements.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC