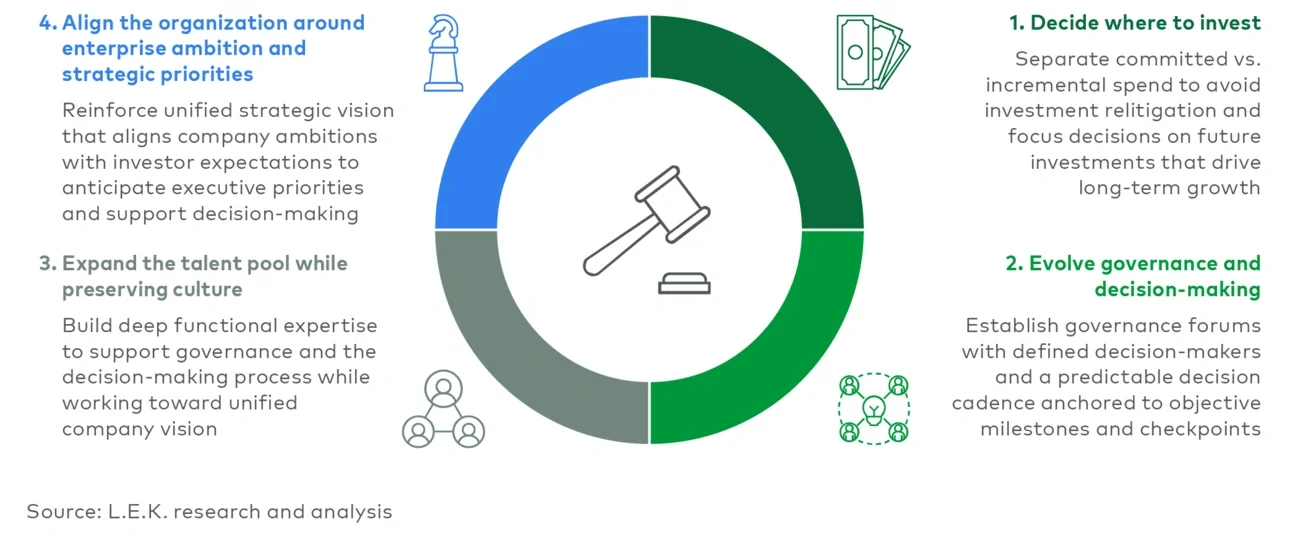

2. Evolve governance and decision-making

As organizations scale and decision complexity intensifies around a first launch, governance must evolve. Decision rights should be explicit so teams understand who proposes, who challenges and who decides. A standing governance forum aligned with the corporate calendar should oversee enterprise, portfolio and functional investments to ensure timely decisions, coordination, and structured escalation to the executive team or board when needed.

A predictable decision cadence that is anchored to the annual plan, a midyear strategic refresh and portfolio checkpoints tied to major readouts help with management of decisions that run on different timelines. Funding should be linked to objective milestones (e.g., completion of investigational new drugs, trial readouts, launch progress, profitability acceleration). Equally important to continually strengthening the next cycle are post-investment reviews that capture what was funded, what happened and what was learned.

As the organization grows, the mid-layer becomes vulnerable: Roles narrow, responsibilities fragment and connection to senior leadership can erode. Clarifying ownership for each critical investment decision and empowering midlevel leaders as active contributors helps prevent this disconnect. While most companies can enhance investment rigor without altering reporting lines, a targeted structural review is prudent to ensure no barriers impede decision quality and to preserve clear pathways for midlevel leaders to access senior governance bodies and escalate issues when needed.

3. Expand the talent pool while preserving culture

The transition from an entrepreneurial R&D environment to a more specialized commercial organization requires shifting to a different talent profile. The early-stage “generalist athlete” who is comfortable wearing multiple hats and navigating ambiguity becomes less scalable as operational complexity increases. To support launch and growth, companies must recruit specialists with deeper functional expertise, often from larger, more structured organizations.

This diversification of talent can introduce risks. New hires may bring a bias toward process over outcomes, consensus-driven decisions, or a focus on building hierarchical teams rather than enabling speed and agility. The right balance blends the adaptability and ownership orientation of the original biotech culture with the functional depth of experienced leaders from scaled organizations. Achieving this balance requires thoughtful selection, structured onboarding and clear expectations about how decisions are made and how work gets executed in scaling the enterprise.

At the center of successful talent expansion is cultural stewardship. The cultural hallmarks seen across many of our biotech clients, such as confidence in the science, resilience through setbacks, openness to risk-taking, adaptability to shifting competitive and capital conditions, and deep patient focus, must not diluteas the company grows. These traits often empowered the company to achieve its first approval. Codifying the principles that define “how we win,” reinforcing them through hiring, development and recognition, and role-modeling them at the top ensure the organizational culture remains a catalyst rather than a casualty of scale. Vertex, for example, grounds its organization in four value principles — commitment to patients, innovation as lifeblood, fearless pursuit of excellence and the primacy of “we” — that guide performance and decision-making across the enterprise.

4. Align the organization around enterprise ambition and strategic priorities

As companies transition from R&D to the commercial stage, execution quality depends on how clearly the organization understands where the company is headed, why it matters and how each function contributes. With growth come specialization and added layers, increasing the risk that teams become siloed or lose connection to the enterprise ambition and goals.

Sustaining alignment requires grounding employees, especially the mid-layer, in the company’s long-term ambition, its strategic priorities and the few critical value drivers that shape its success. Before launch, this alignment forms naturally around the shared goal of first approval. Post-launch, as responsibilities diversify and operating complexity rises, the mid-layer becomes the pivotal conduit that keeps the enterprise narrative alive and ensures day-to-day decisions reinforce (rather than dilute) strategic intent.

Investor expectations should serve as a valuable orienting signal, a way to understand the external factors that shape long-term value creation. These expectations provide a clear lens on what matters most for sustainable growth, including revenue trajectory, expense discipline and the pathway to profitability, and midlevel leaders in particular must understand how they intersect with the company’s strategy. Leaders’ ability to internalize these signals and translate them into enterprise choices helps the organization anticipate executive priorities and supports more consistent, forward-looking decision-making.

Next steps: A brief self-diagnostic

Taken together, these four actions create an enterprise model that scales with spend, complexity and organizational growth. To determine where recalibration will deliver the greatest impact, leadership teams can reflect on the following questions:

Investment discipline. Do we maintain a complete, cross-functional view of both committed and incremental investment opportunities, supported by a unified assessment framework

Comparability and prioritization. Are investment decisions informed by a consistent set of metrics tailored to investment type, enabling transparent trade-offs across functions

Governance and decision rights. Are decision rights (i.e., who proposes, who challenges, who decides) explicit, codified and consistently applied across enterprise, portfolio and functional investments? Do we operate against a predictable corporate planning cadence (e.g., annual plan, midyear refresh, milestone-based checkpoints) that keeps decisions moving

Talent and culture. Have we struck the right balance between early-stage entrepreneurial talent and specialized hires from larger organizations while actively preserving the cultural attributes that drove our initial success?

Enterprise alignment and investor expectations. Do teams across all levels, not just the executive suite, understand the enterprise ambition, strategic roadmap and evolving investor expectations, and how their decisions influence the company’s long-term value drivers?

Midlevel empowerment. Are midlevel leaders sufficiently empowered, connected to enterprise strategy and able to escalate insights and risks to senior governance bodies?

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC.