The findings suggest that sustainability is increasingly being implemented through wider packaging redesign rather than through isolated material substitution. Companies are using packaging changes to address multiple objectives simultaneously, including circularity, functionality, consumer experience and stock-keeping unit flexibility, reinforcing packaging's growing role as a platform for differentiation and portfolio agility.

Importantly, many of these decisions involve tradeoffs that packaging teams are still working through. Recyclable or mono-material formats can introduce higher costs or weaker barrier performance in certain applications, while innovative formats may prove difficult to scale consistently across large portfolios and multiple geographies.

As a result, the competitive advantage is increasingly rests with companies that can balance sustainability ambition with operational feasibility and commercial discipline.

Regulation is making execution the differentiator

Regulatory pressure is accelerating this transition, with sustainable packaging increasingly becoming a baseline expectation rather than a point of differentiation. Across Europe, measures such as the Packaging and Packaging Waste Regulation and recycled-content requirements under the Single-Use Plastics Directive are tightening expectations around recyclability, recycled content, packaging minimisation and labelling requirements.

However, the commercial implication extends beyond compliance alone. The challenge for brand owners is increasingly about execution capability: translating sustainability commitments into practical decisions across materials, suppliers, packaging formats and rollout sequencing while maintaining product performance and controlling costs.

The survey findings also suggest that sustainability expectations themselves are evolving. Brand owners increasingly define sustainable packaging not only through recyclability but also through broader system-level measures such as lower greenhouse gas emissions, renewable energy use and supplier environmental practices.

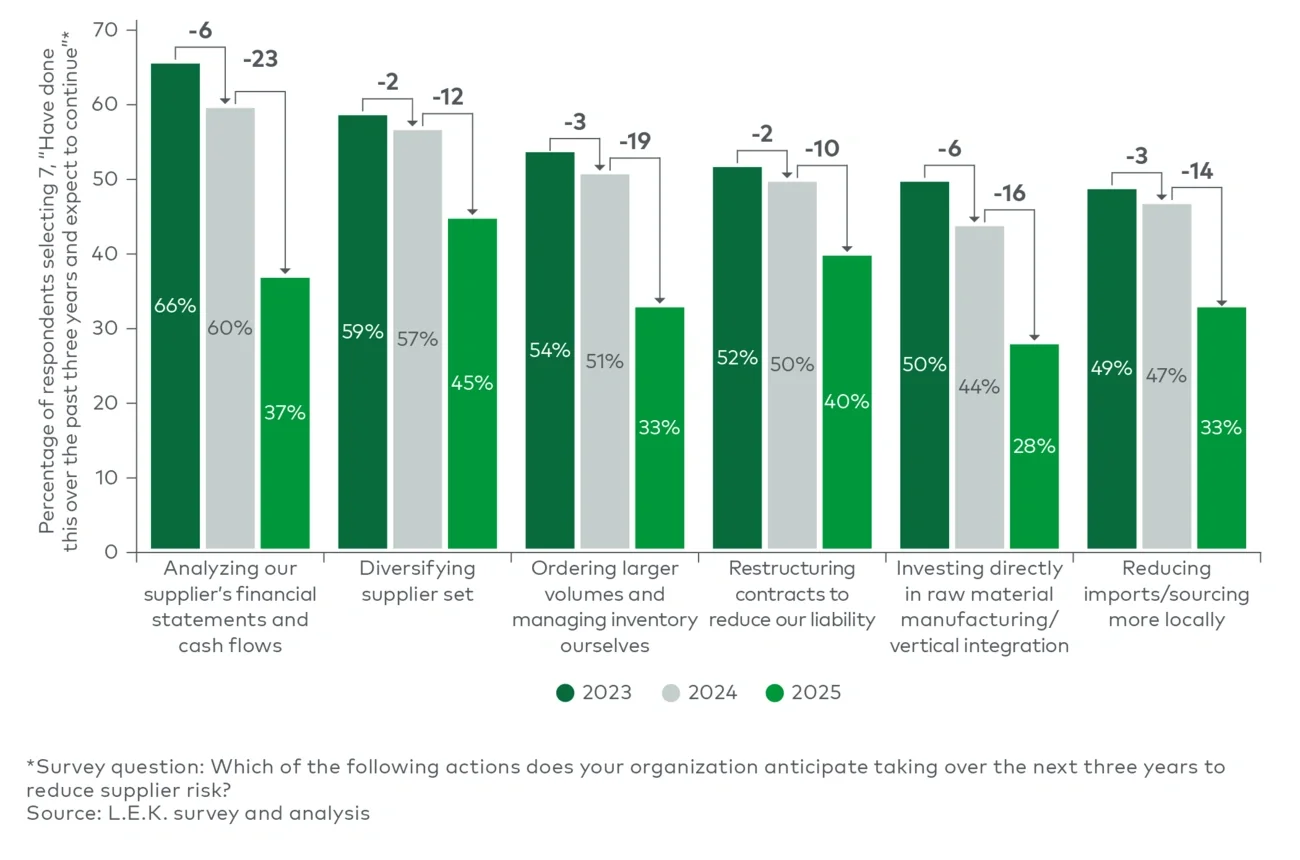

At the same time, economic constraints remain significant: 41% of respondents cite inability to absorb or pass through higher packaging costs as the main barrier to further sustainable packaging adoption. This tension between sustainability objectives and commercial realities is likely to remain a defining feature of packaging strategy over the coming years.

Three strategic priorities for packaging suppliers

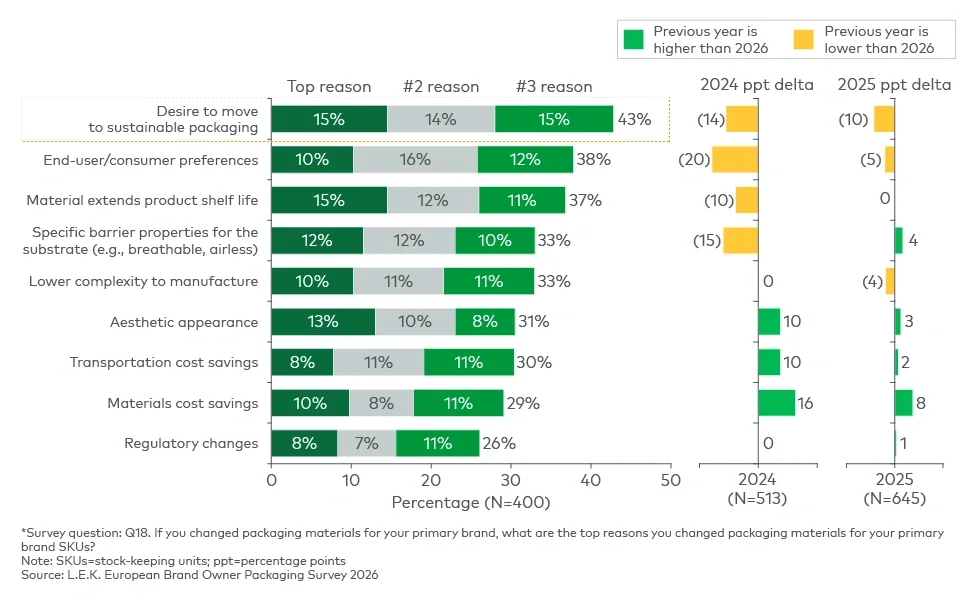

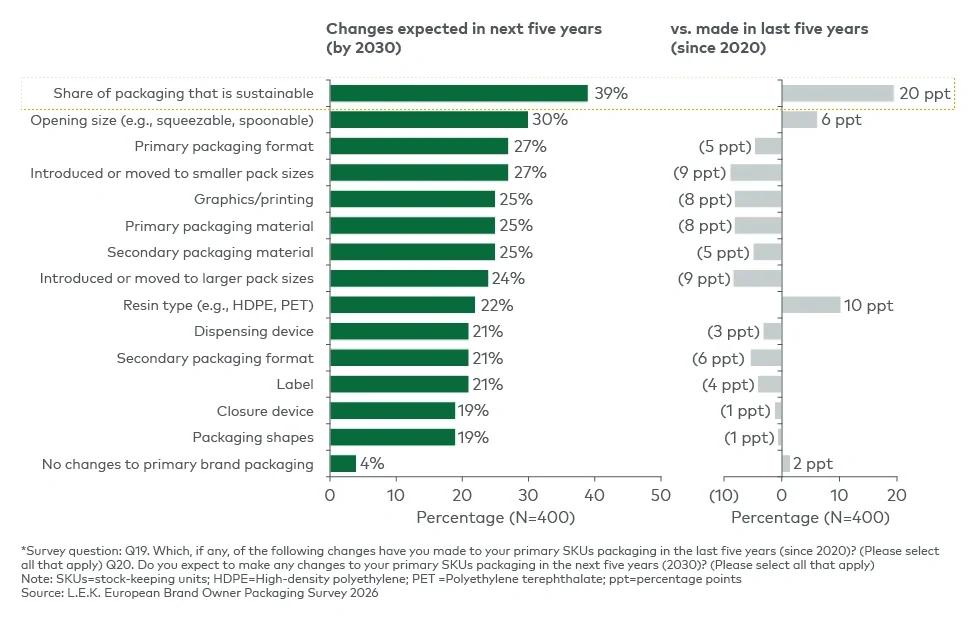

The survey findings suggest that sustainability is no longer being addressed primarily through standalone packaging projects. Instead, it is becoming a broader redesign challenge that affects sourcing, pack architecture, compliance and consumer interaction simultaneously.

For packaging suppliers, three strategic priorities are emerging.

1. Scale circular-ready packaging without adding unnecessary complexity

As sustainable packaging becomes a baseline expectation, suppliers can differentiate by helping customers scale circular-ready solutions across portfolios without significantly increasing operational complexity.

This includes:

- Simplifying structures and substrates where feasible without compromising product protection

- Supporting recyclable and mono-material designs that remain commercially viable at scale

- Developing packaging solutions that can adapt to evolving reuse and refill requirements where economically practical

The challenge is increasingly about repeatability and manufacturability, not simply innovation in isolation.

2. Secure access to sustainable materials and resilient supply chains

Although sustainability has regained strategic momentum, supply security and cost management remain critical concerns for brand owners.

Suppliers that can secure reliable access to recycled and alternative materials, manage supply volatility and demonstrate credible emissions progress are likely to strengthen their competitive position.

Key priorities include:

- Expanding qualification pathways for alternative resins and fibre grades

- Building stronger recycled-feedstock partnerships and sourcing models

- Improving transparency around emissions, renewable energy sourcing and material traceability

As sustainability requirements tighten, material availability and compliance credibility are increasingly becoming sources of competitive differentiation.

3. Make sustainability commercially visible to consumers

The survey findings suggest sustainability gains greater traction when paired with tangible improvements in usability and consumer experience.

Packaging suppliers can support this by helping brands:

- Improve openability and dispensing convenience while maintaining material efficiency

- Introduce right-sized formats that reduce excess packaging

- Simplify disposal and recycling guidance through clearer labelling and pack communication

- Strengthen substantiation and traceability to reduce greenwashing risk

For many brands, sustainability is becoming most effective when consumers can see and experience the benefit directly, rather than encountering it only through marketing claims.

Sustainability is becoming an execution challenge, not just an ambition

European brand owners are increasingly moving beyond sustainability commitments to implementation at scale. Over the next several years, competitive advantage is likely to depend less on headline sustainability targets and more on the ability to execute consistently across sourcing, design, compliance and consumer experience.

For packaging suppliers, the opportunity increasingly lies in helping customers scale sustainable packaging solutions that are operationally viable, commercially credible and compliant by design.

This article follows the first article in the series, which examined the return of selective growth across the European packaging market. In the next article, we explore how US tariffs and trade uncertainty are reshaping packaging sourcing, supplier strategies and regional manufacturing footprints across Europe.

To discuss how these sustainability trends apply to your business, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting