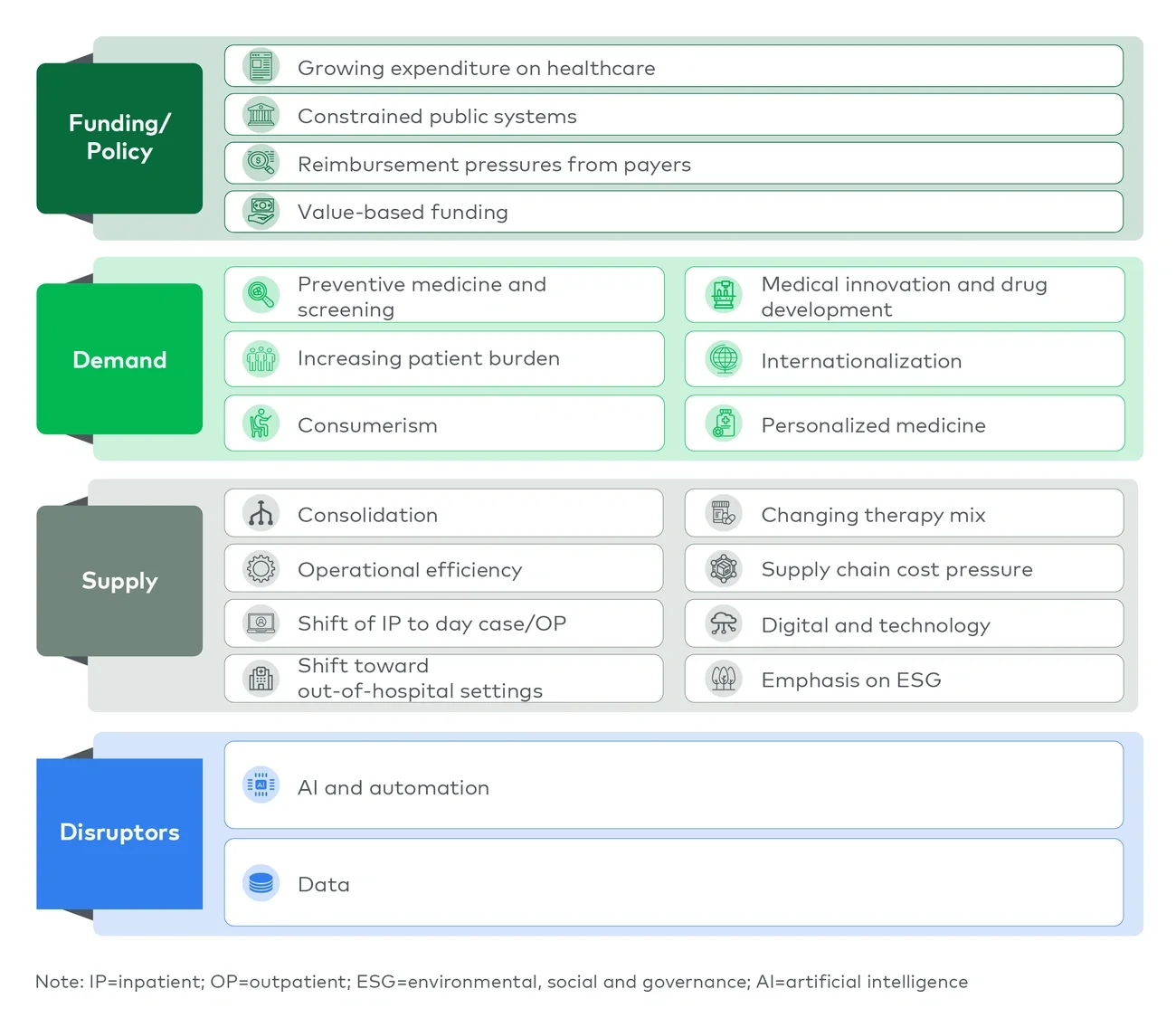

The landscape is shifting from volume growth to pathway control

Across the GCC, healthcare systems are moving away from hospital-centric models toward integrated, multisite care pathways. Policymakers are prioritizing access, prevention and efficiency, which is changing how and where care is delivered.

- In the UAE, this shift is reinforced by the strategic will to have stronger primary care gatekeeping, preventive programs and digital infrastructure

- In Saudi Arabia, it is driven by health clusters, expanding private participation and new delivery formats

Globally, this transition is already well advanced. Across The Organization for Economic Co-operation and Development (OECD) markets, a growing share of procedures is delivered in outpatient or day-case settings, reflecting a structural shift away from inpatient care toward more efficient sites of care. Many procedures that were historically hospital-based are now routinely delivered on a same-day basis.

As a result, demand is no longer passively captured. It must be actively managed across the patient’s journey. Providers that rely on episodic hospital demand risk losing share to those that control referral flows and outpatient access.

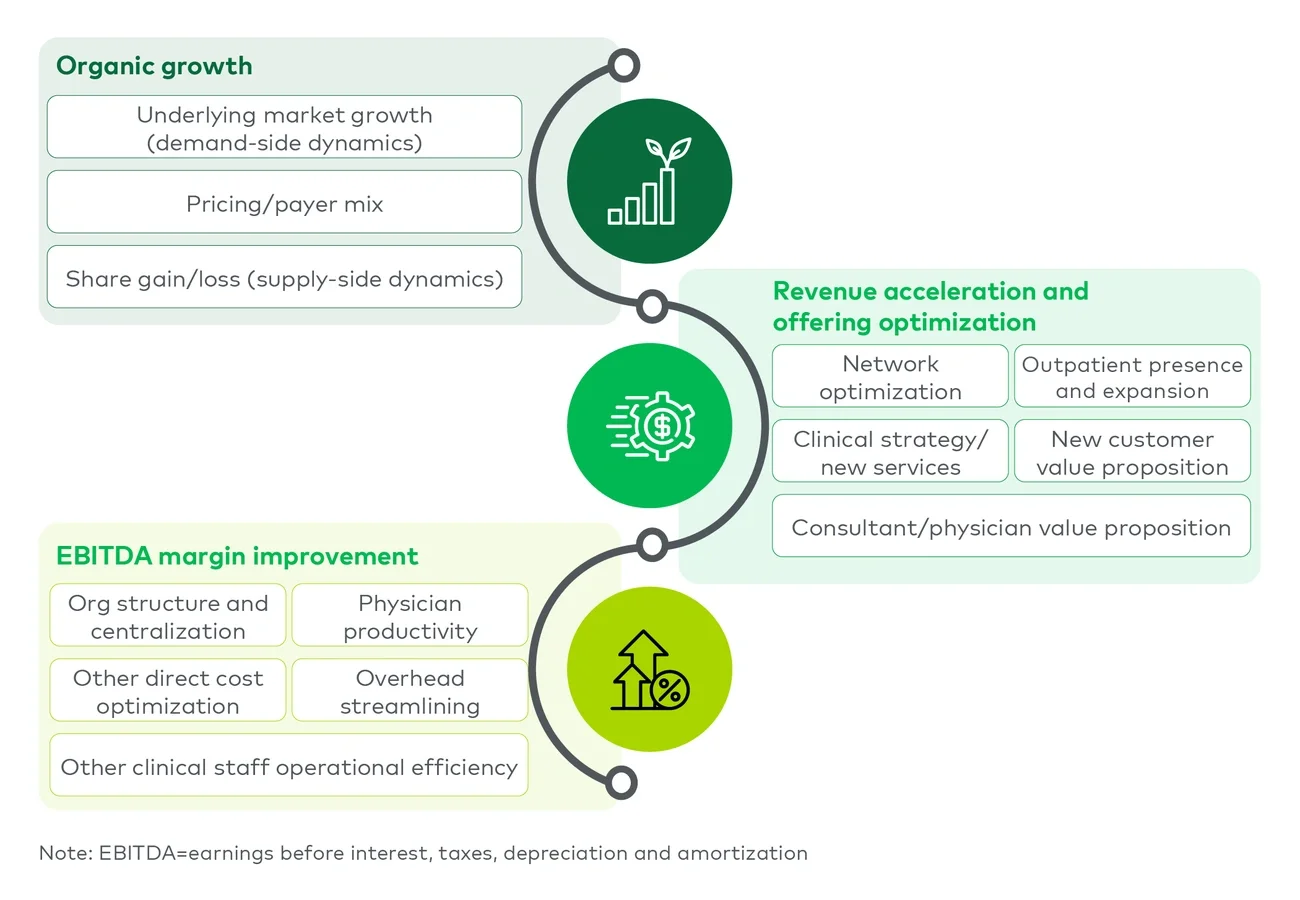

Value creation rests on three linked agendas (see Figure 2)

1. Targeted organic growth, not undifferentiated expansion

Value creation begins with a precise understanding of where attractive growth exists across specialties, care settings, payers and patient cohorts.

- Not all growth is equally valuable

- Winning providers align structural demand with clinical capability, market white space and economic returns

In practice, this often means prioritizing:

- Elective surgery and chronic disease pathways

- Women’s and family health

- Outpatient expansion and other nonhospital areas such as long-term care

Across the GCC, this requires moving beyond capacity-led strategies toward networked service deployment that connects care settings and reinforces patient retention.

2. Local access and site-of-care optimization as demand capture levers

Local access is increasingly central to both growth and referral control. Policymakers are encouraging models that improve convenience and reduce pressure on acute care hospitals.

This is accelerating the importance of:

- Primary care and polyclinics

- Day surgery and diagnostics

- Community-based care formats

Equally important is optimizing the settings mix across the care pathway. Hospital infrastructure should be reserved for high-acuity, complex care, while lower-acuity procedures, diagnostics and interventions are increasingly delivered in outpatient or community settings. This shift is supported by global evidence showing that many procedures can be safely delivered outside of hospitals with comparable or improved outcomes and lower costs.

A significant share of demand continues to leak to competitors or major urban centers due to gaps in accessibility, trust or service breadth. Providers do not need full tertiary capability locally, but they must offer a compelling proposition for routine and secondary care supported by clear escalation pathways.

3. Earnings before interest, taxes, depreciation and amortization (EBITDA) margin improvement through operational discipline

Sustainable margin improvement is not driven by cost cutting alone. It requires systematic operational excellence embedded within clinical delivery.

Key levers include:

- Organizational design and staffing optimization

- Theater utilization and facility productivity

- Revenue cycle and claims management

- Procurement and shared services

- Automation of administrative processes

A critical component of this agenda is improving the utilization of hospital infrastructure. One important shift is from inpatient to day-case delivery models. For example, in Australia, tonsillectomy day cases increased from 266 in 1993 to 11,199 in 2022, while inpatient volumes remained substantial, increasing from 33,481 to 46,794. This lifted the day-case share from 0.8% to 19.3%, demonstrating how activity can be rebalanced without reducing overall demand.

Leading organizations treat operational performance as a core enabler of both growth and clinical quality rather than as a stand-alone efficiency initiative.