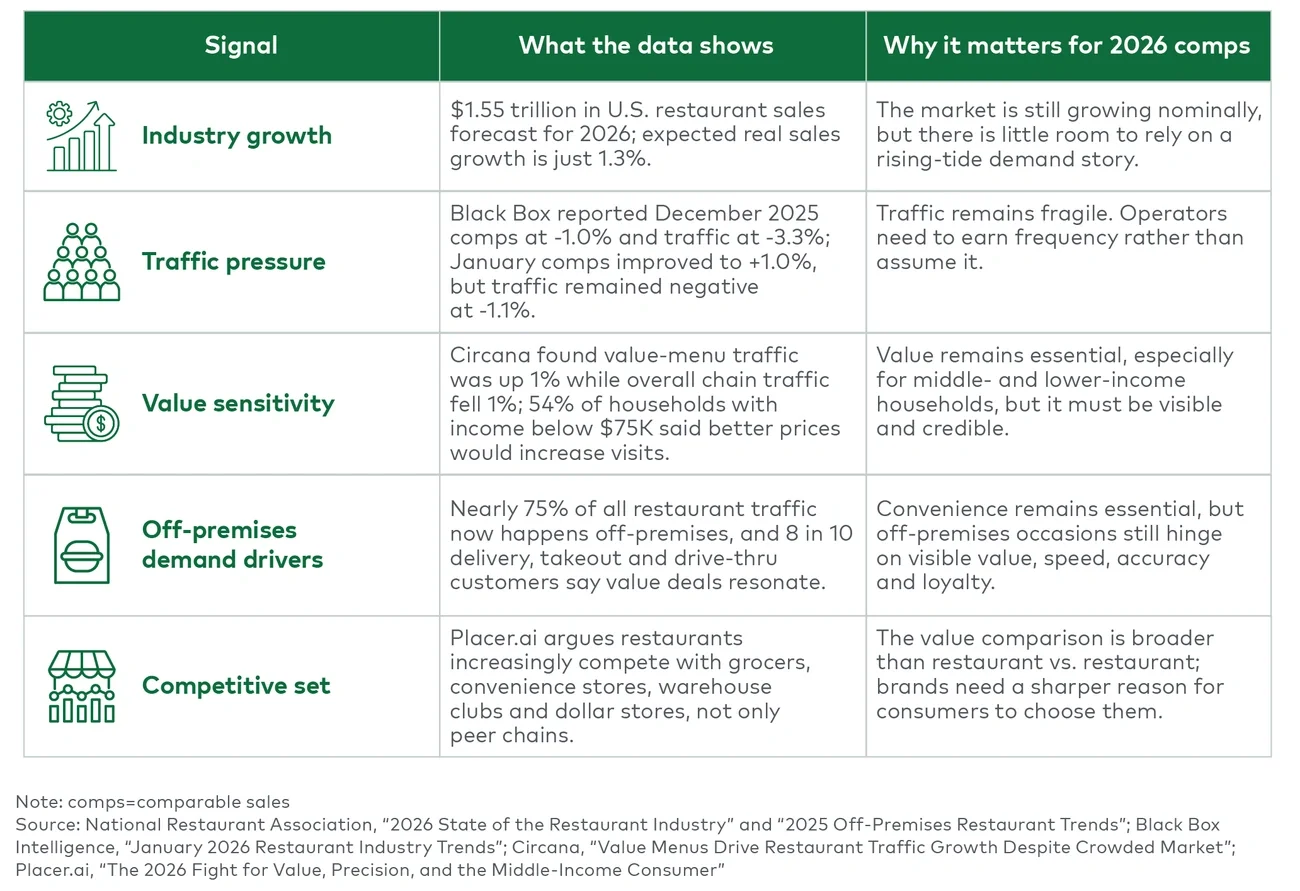

Price-led growth has run its course

Price increases are no longer driving restaurant growth, and in many cases, they are now suppressing it. In 2026, comparable-sales (comps) performance has shifted back to traffic and frequency, forcing operators to rebuild the guest value equation from the ground up.

The National Restaurant Association expects only 1.3% real sales growth in 2026. Black Box data shows traffic remained negative in both December 2025 and January 2026. The industry continues to grow nominally, but the easy levers are largely gone.

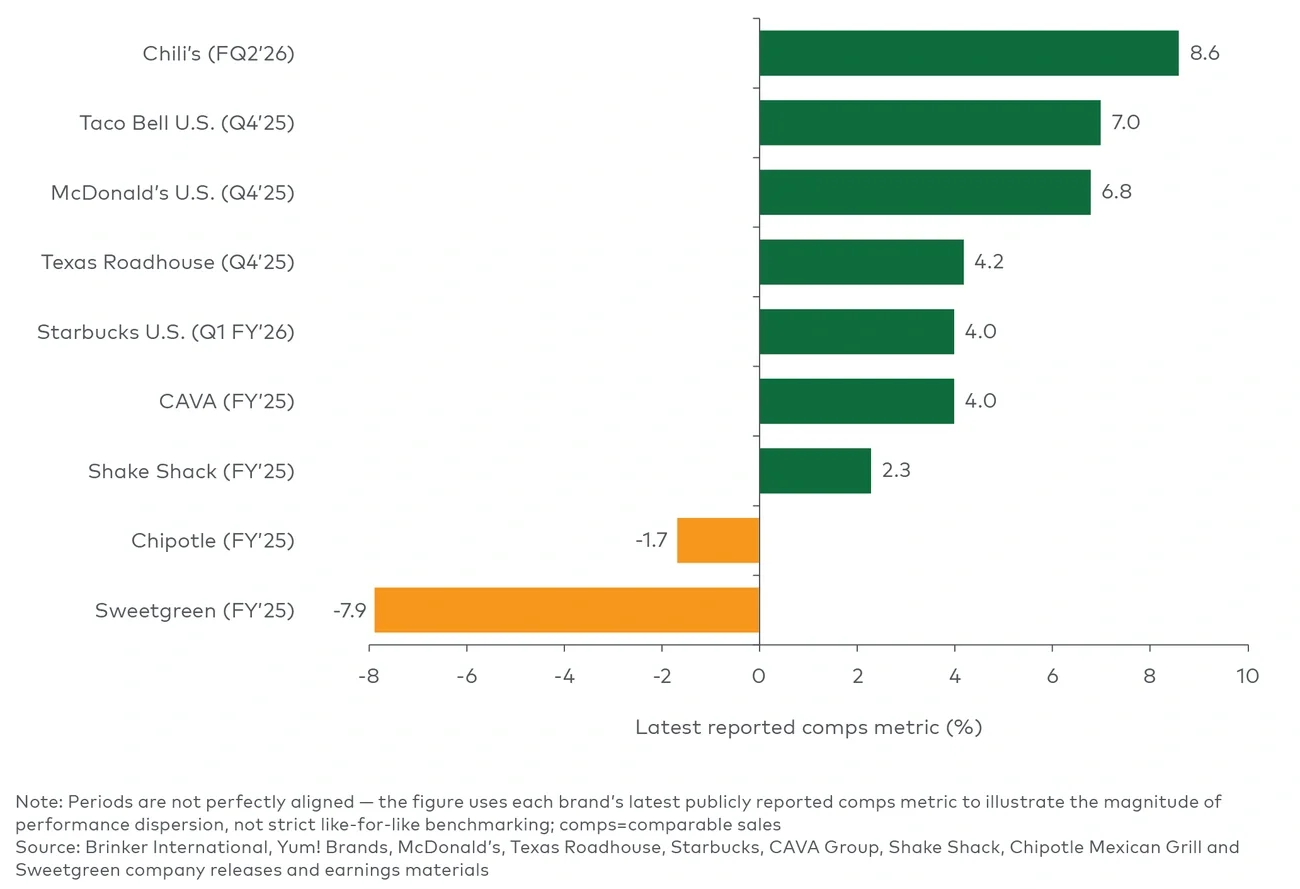

In this environment, pricing is no longer a dependable engine of top-line growth. In some cases, it may now be weighing on traffic and, by extension, comps. Yet the market is not moving in lockstep. A growing set of restaurant brands is outperforming despite the same macro conditions. That widening spread suggests the next phase of comps growth will be driven less by market tailwinds and more by how effectively each brand rebuilds its value equation, especially when serving middle- and lower-income consumers (see Figure 1).