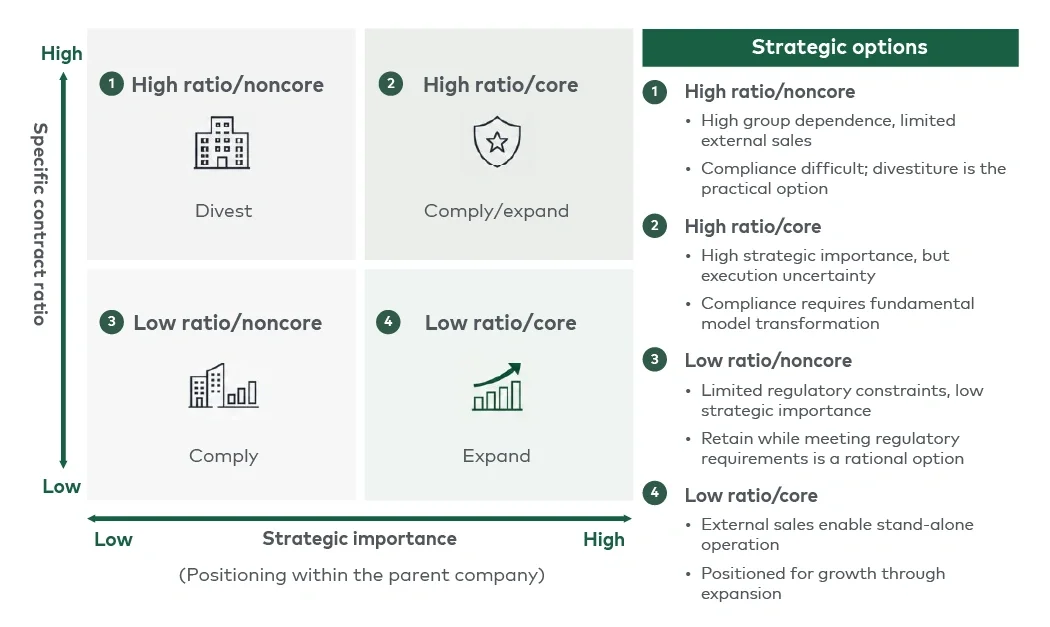

4.3. Option C: Expand — Position the agency as a growth platform

Under this option, the in-house agency is repositioned not as an internal support function but as a growth business. This involves expanding insurance provision to external clients and scaling the platform through acquisitions and integration of other agencies, while meeting regulatory requirements.

This path requires a transition from a group-centric model to one that actively serves external clients. It may involve acquisitions, integration efforts and talent development. While resource intensive, it offers potential not only for compliance but also for long-term growth of the agency business.

4.4. How to choose among strategic options

In-house agencies have multiple strategic options — comply, divest or expand — but these are not equally feasible for all companies. The critical question is not which option is theoretically optimal, but which is realistically executable.

Feasibility depends on regulatory requirements and on structural characteristics unique to in-house agencies, particularly in the following areas:

Ability to transfer people (not just contracts)

- In divestitures, the transfer of personnel is a central issue. Many in-house agencies rely on staff who simultaneously perform roles within the parent company, making full transfer difficult. This often results in situations where contracts transfer but personnel do not sufficiently follow.

- Even where staff are transferred, discrepancies may arise between prior workload and posttransfer expectations (e.g., full-time deployment), leading to inefficiencies or mismatches in staffing levels and threats to business viability.

- Therefore, securing dedicated personnel aligned with contract volume is a prerequisite for a viable stand-alone business.

Ability to develop external customers

- Both comply and expand strategies require growth in external business. However, in-house agencies are typically built around internal demand and often lack external sales capabilities, including sales infrastructure, brand recognition and incentive systems.

- Developing these capabilities requires more than incremental changes; it entails building a new commercial function and effectively transforming the business model.

Timing relative to regulatory implementation (investment and lead time)

- Organizational restructuring, talent reallocation and capability building require a long time. Given regulatory timelines, the range of feasible options is constrained by the time available.

- Furthermore, uncertainty around future regulatory changes increases investment risk, particularly for options requiring long-term commitments.

Ability to separate intertwined plans (treatment of group life insurance)

- Group life insurance, often embedded within HR and payroll, is difficult to separate from the parent organization. Even when externalizing the agency, the insurance plan itself typically remains with the parent, requiring a separation between system governance and insurance placement.

- The feasibility and design quality of this separation directly affect not just employees but also relationships with insurers and counterparties, thereby influencing the viability of strategic options.

In practice, while all options are theoretically viable, feasibility varies significantly by company. For many, externalization, including divestiture, emerges as the most practical path.

Given these constraints, it is important to determine the optimal direction for the company by considering both the level of the specific contract ratio and the strategic importance of the agency.

5. Emergence of a buyer’s market: Strategic opportunities for private equity and platform players

The impact of regulatory tightening is becoming increasingly visible, particularly as changes to the specific contract ratio make it difficult for agencies reliant on intragroup transactions to remain compliant. As a result, reviewing business models or pursuing externalization is becoming a realistic option.

Although in-house agencies vary in size and capability, they hold valuable assets, such as corporate client relationships, specialized talent and insurer ties, that are often underutilized on a stand-alone basis but can gain value through consolidation.

With more firms likely to consider externalization, and clear potential for value creation through integration, this creates a meaningful opportunity for investors and platform players.

5.1. Key buyer groups

Private equity (buyout funds)

An increase in carve-out opportunities creates favorable conditions for roll-up strategies. By acquiring and integrating multiple agencies, buyers can drive efficiency through shared back-office functions, compliance frameworks and information technology platforms, while expanding into external markets. Given the fragmented nature of Japan’s insurance distribution market, the potential for value creation through consolidation is substantial.

Domestic independent agencies and platform players

These players focus on expanding their customer base and enhancing portfolio quality. Relationships with large corporate clients held by in-house agencies are difficult to replicate through organic growth and represent high-value assets.

They may also seek to strengthen risk management capabilities, deepen sector expertise or enhance global service capabilities, while maintaining continuity with existing customer relationships.

Global independent agencies and platform players

Leveraging global networks and specialized expertise, these players pursue acquisitions to strengthen their presence in Japan and enhance service offerings. In-house agencies can be integrated into existing platforms to generate additional value.

The distinction from domestic players lies less in capability than in their approach, emphasizing globally standardized service delivery and expansion into specialized domains.

5.2. Key success factors in acquisitions

Even where acquisition opportunities arise, success depends on postacquisition value creation. Key factors include:

- Activation of customer base and service expansion

Deepening engagement within existing corporate relationships and expanding service offerings is a practical path to revenue growth. - Integration of back-office functions

Consolidating fragmented administrative functions (policy management, compliance, finance) improves efficiency and reduces costs. - Digitalization and productivity enhancement

Digitizing processes across sales support, customer management, quoting, contracting and claims can significantly improve productivity. - Smooth stakeholder transition

Successful carve-outs depend on maintaining relationships across employees, customers and the parent company. In Japan, employment continuity, stable working conditions and service continuity are critical, making transparent, trust-based transition design as important as the postacquisition operating model for execution and value creation.

It is also expected that group life insurance programs will remain with the parent company, limiting the acquisition scope primarily to nonlife agency functions.

Conclusion: The importance of acting now

The in-house agency landscape is at a structural inflection point driven by regulatory change. Previously tolerated business models are now being reassessed based on the in-house groups’ ability to operate as independent agencies.

Companies face three strategic options — comply, divest or expand — none of which can be pursued passively. Each requires deliberate, strategy-aligned preparation, and given the regulatory timelines, delaying decisions is not viable.

As restructuring accelerates, market conditions may shift, with more sellers potentially impacting deal dynamics and transaction terms.

Ultimately, the priority is to define the in-house agency’s role within the broader portfolio, shaping compliance, competitiveness and resource allocation. Deciding whether to retain, externalize or scale is no longer optional — it is a proactive strategic imperative.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC