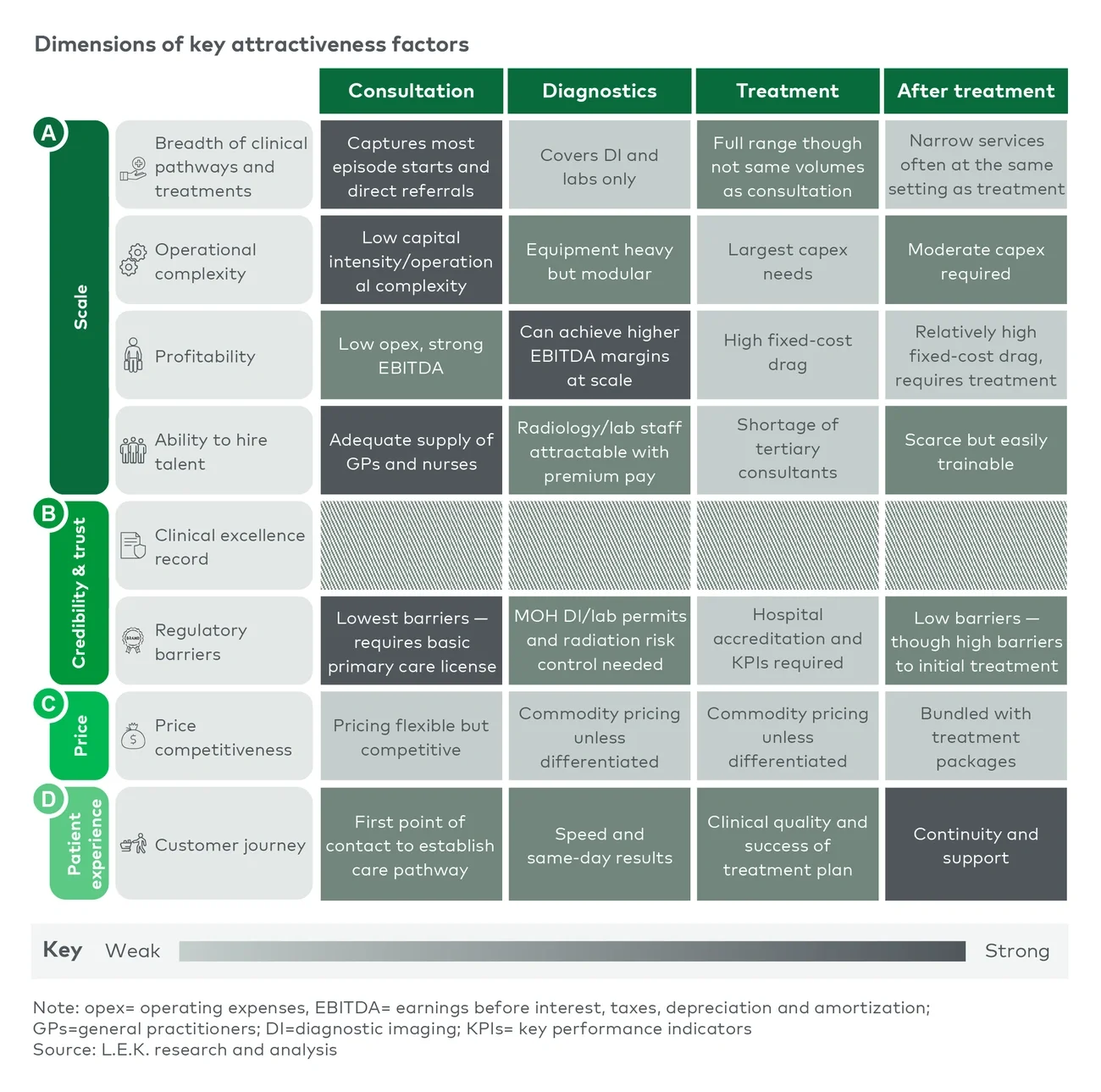

Consultation offers the lowest capital intensity and operational complexity, the lightest licensing requirements, an adequate supply of general practitioners and, critically, control of the point where most care episodes begin and referrals are made. Diagnostics is equipment heavy but modular, can achieve higher EBITDA margins at scale and can attract radiology and laboratory staff with premium pay. Treatment carries the largest capital expenditure needs, hospital accreditation requirements and a shortage of tertiary consultants, while posttreatment services are typically bundled with treatment and rarely stand alone.

The economics compound on both sides of the ledger. Ownership generates new revenue beyond premiums, through consultation fees and diagnostic imaging and laboratory services, while shared administrative infrastructure lowers cost to serve. It also closes the data loop: An insurer with real-time clinical data, not just claims data, can monitor billing integrity directly, identify at-risk members early and intervene before an episode escalates into an expensive admission. Cost recovery alone justifies attention: With fraud, waste and abuse running at up to 10%-12% of claims, even partial recapture inside an owned network moves the loss ratio more than most repricing cycles.

The sequencing matters as much as the selection. Consultation first secures the referral engine, and then diagnostics captures the spending that those consultations originate. An insurer that owns both controls the entry point of the pathway and the single richest source of clinical data, before committing a riyal to a hospital bed.

Global payers have already proven the playbook

None of this is untested. Bupa in the United Kingdom expanded from private medical insurance into own-brand hospitals, dental clinics and a digital general practice through decades of acquisition. Sanitas, Spain’s second-largest health insurer, has invested over EUR1 billion since 2021 in hospitals and its Blua digital primary-care platform. CVS Health became a payer-provider by acquiring Aetna in 2018 for USD69 billion, rolled out 1,200 HealthHUBs and in 2023 bought Oak Street Health and Signify Health to tighten vertical control. UnitedHealth Group’s Optum arm now spans more than 90,000 physicians alongside urgent-care and home-health provision. Optum has since grown into a substantial contributor to UnitedHealth Group’s operating earnings, evidence that provision can become a profit engine in its own right rather than a cost-control appendage. Kaiser Permanente, fully integrated since the 1940s, remains the standing proof that payer-provider alignment lowers hospitalization rates and cost to serve.

The honest caveat is that none of these journeys was frictionless. Integrated payers abroad have drawn regulatory scrutiny, provider resistance and periodic member backlash. The lesson for Saudi insurers is not that integration is easy; it is that the model works when the entry point, the governance and the pace are chosen deliberately.