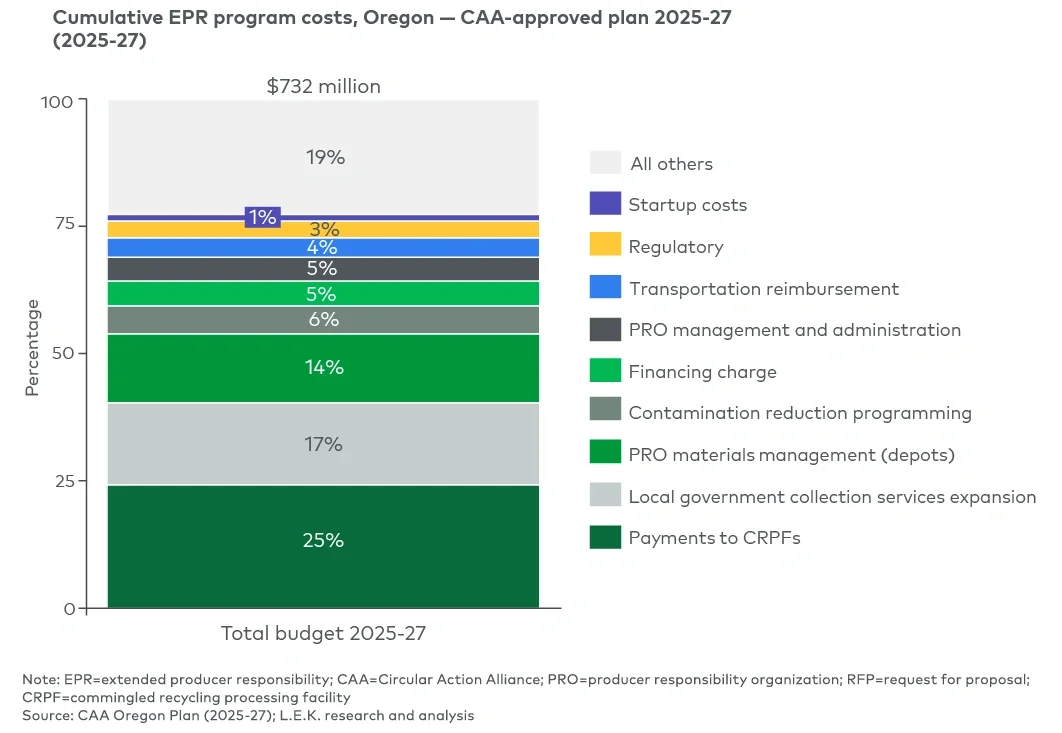

For local governments and service expansion, CAA funding has been budgeted based on a comprehensive statewide survey conducted in 2024, which identified system needs and allowed the submission of funding requests across operations and education, containers, trucks, depots and reload facilities. Requests were ranked across six levels of priority, with full funding schedules for 2025-27 outlined in the approved CAA plan. For transportation reimbursement, a standardized hourly rate is used to cover materials transported more than 50 miles from depots to CRPFs, processors or responsible end markets. While funding allocations for the 2025-27 period have been defined, future budget rounds will provide opportunities for service providers and municipalities to gain incremental investment as system performance targets increase.

The level of funding outlined in the CAA plan represents a step change for the sector. In Oregon, the estimated $70-per-resident allocation in 2027 is significantly higher than other established benchmarks, such as Belgium’s long-running EPR scheme operating through Fost Plus PRO, which committed approximately $26 per resident in the organization’s 2024 budget. More than half of that budget was invested in the collection, sorting and post-sorting of residual streams. The impact of such funding on waste collection and processing activity is clear, with the EU-wide plastic packaging recycling rate increasing from 25.2% in 2005 to 40.7% in 2022 under EPR regulations. The CAA plan for Oregon aims for an even greater increase in recycling volumes, with statewide targets of 25% by 2028, 50% by 2040 and 70% by 2050.

Beyond the direct funding allocated to waste collection, processing and recycling expansion, given the need for detailed data tracking, LCAs and compliance oversight, EPR frameworks’ granular reporting requirements and complex eco-modulated fee structures also drive positive outcomes for enabling service providers. Services that can provide material flow transparency, identify pathways to fee reduction and enable circular innovation and technologies that connect information from production through collection and recycling are particularly important, as they allow producers and regulators to monitor compliance in real time.

Importantly, the infrastructure and service implications of EPR extend beyond traditional recycling. Emerging U.S. programs increasingly recognize recycling and refill systems and composting as integral components of the broader materials management system. For example, Oregon’s producer-funded Material Impact Reduction and Reuse Program provides grants and loans to support reusable and refillable products, repair and lifespan extension initiatives, pilot projects and technical assistance. Similarly, Minnesota’s statute defines eligible infrastructure investments to include equipment and facilities that enable recycling and composting. Additionally, California’s SB 54 needs assessment evaluates both existing and required recycling/refill and composting infrastructure to inform producer budgets and implementation plans. As a result, EPR programs may direct capital not only toward sorting and recycling infrastructure but also toward the systems that enable recycling models and composting pathways where collection systems and end markets are in place.

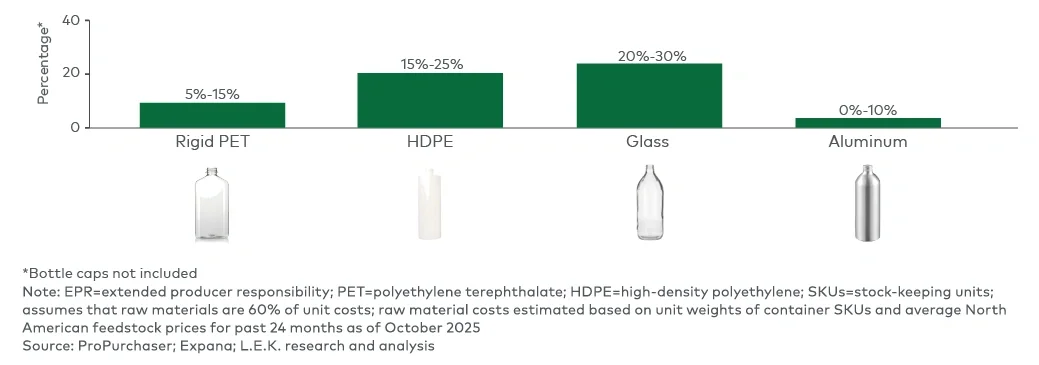

EPR regulations also generate upstream effects as producers look to minimize their fee exposure through packaging choices. Converters are under growing pressure to deliver lower-impact packaging that reduces system costs and aligns with emerging compliance expectations. In Oregon, for example, switching to materials with lower fee rates (e.g., from rigid plastics to paper) can cut base EPR fees by more than half. Illustrative CAA modeling suggests that changing detergent packaging from an HDPE container, PP cap and PE label to just an HDPE film pouch would reduce base fees by 55%, while further packaging improvements supported by LCAs would achieve a 10%-20% additional reduction through eco-modulated bonuses.

These financial incentives can influence material mix shifts, prompting raw materials suppliers to shift their focus toward recycled feedstocks, bio-based alternatives and recovery of secondary materials. The rise of recycling business models further strengthens this trend by reducing the need for new inputs altogether, as refillable and reusable packaging often qualifies for reduced EPR fees under eco-modulated frameworks. Germany offers a useful example of the scale of potential change if recycling systems become mainstream, with approximately 35% of beer and water bottles now sold in refillable form.

For consumers, the effects of EPR are felt more indirectly. While producers may pass through part of their additional costs (fees, reporting, compliance, packaging redesign, etc.) to product pricing, evidence suggests that these impacts are modest relative to overall product costs and are frequently diluted across the supply chain. A comparative study of CPG products in different Canadian jurisdictions commissioned by the Oregon DEQ, for example, found net-neutral price differences for packaging and printed paper products between EPR and non-EPR environments. Using a basket of 17 common CPG products as the assessment point, EPR fees were found to represent up to 2.3% of individual product retail prices and there was limited consistent correlation between the magnitude of EPR fees and retail price changes.

Oregon’s fee levels and retail prices are broadly similar in magnitude to those seen in mature Canadian programs, indicating that the Canadian evidence provides a reasonable directional proxy for U.S. schemes. A York University study on the potential impact of EPR on New York state estimates a 4%-6.5% modeled total impact on “basket of goods” pricing (packaged goods), which translates into an additional $35-$60/month in grocery costs for the average family of four. While U.S. EPR programs are still in their early stages, the eventual impact on consumer prices is expected to be moderate and to vary by product type.

Given the impact that EPR regulations are expected to have across the packaging and waste value chain — namely, creating cost and regulatory burdens along with opening new pools of available capital — it is important that companies take a strategic approach to addressing these new regulations.

To learn more, please contact us.

Note: Sources are cited once, at their first point of reference only.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC