Introduction

Oncology is the single largest therapeutic area for global pharmaceutical sales, accounting for c.18% of all prescription drug sales in 2023 – a substantial increase from c.13% in 2018. This growth, exceeding 10% p.a. over the past five years, has been driven largely by innovative drug launches and expanding treatment accessibility. High unmet patient needs and substantial commercial potential continue to attract a breadth of biopharma organisations. Companies outside the top 10 oncology players now generate c.45% of all oncology revenues, up from c.30% five years ago, with small and mid-sized biopharmas carving out niches in specific tumours or treatment modalities.

Oncology thrives on innovation given the degree of unmet needs across tumour types. As a result, it dominates the global drug development pipeline, representing c.40% of all assets in clinical development. Biopharma companies of all sizes compete for the most innovative assets at all stages of drug development. Regardless of their internal capabilities, leaders in oncology rely on external innovation to supplement their internal R&D or as a sole source of pipeline assets.

In our recent Executive Insights focused on biopharma M&A deals, we observed that oncology represents the most significant area of M&A dealmaking. Oncology also dominates biopharma business development and licensing (BD&L), accounting for c.50% of global deal volume. Growing oncology pipelines provide a rich set of BD&L targets, with emerging biopharma now spearheading c.60% of all oncology trials, compared with 33% a decade ago. Reduced public market valuations mean many biotechs require BD&L proceeds to lengthen their cash runways in order to invest in further groundbreaking innovation.

In this Executive Insights, we review the past five years of BD&L dealmaking in oncology and outline what it takes for small to large biopharma organisations to win in this increasingly competitive space. We have considered all global oncology deals between 2019 and 2023, including M&A, licensing, collaborations and co-promotions, and excluded deals for non-pharmaceutical products (e.g. companion diagnostics, manufacturing agreements).

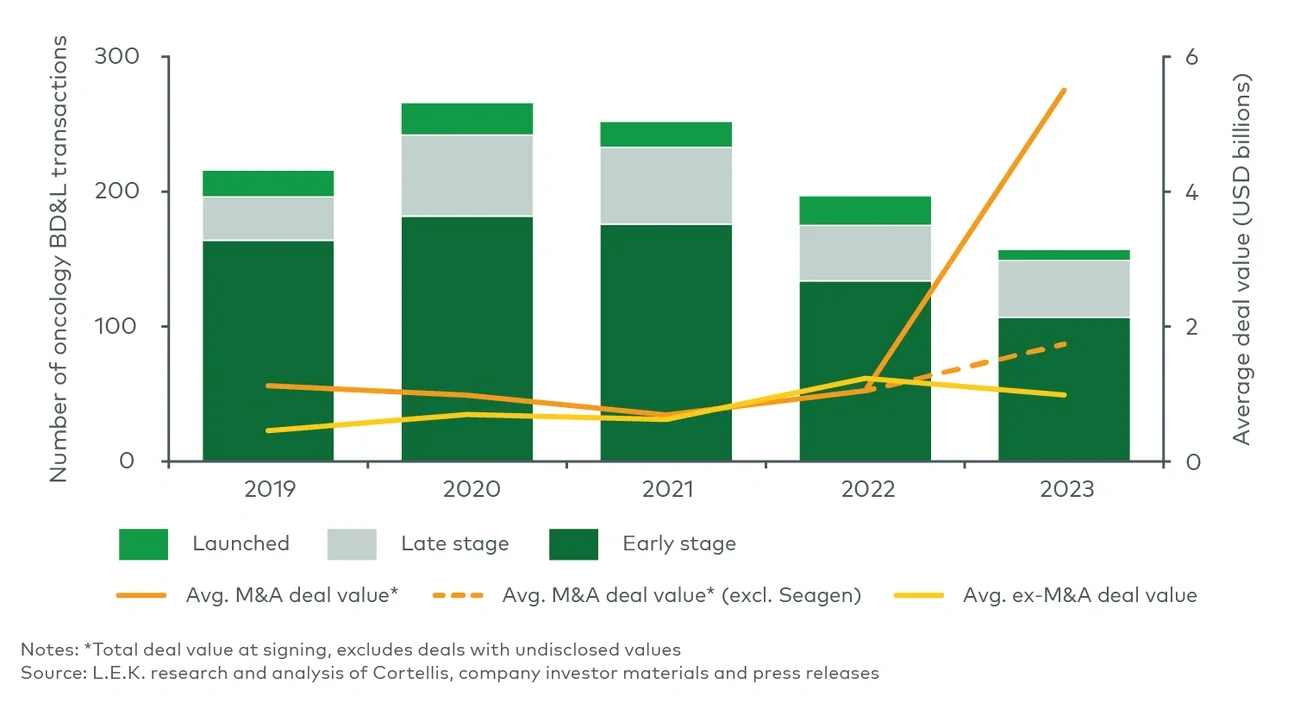

A shift towards late-stage dealmaking

Oncology BD&L transactions peaked in 2020, coinciding with the highest levels of broader biotech funding, deals and initial public offerings. While the total number of BD&L transactions has decreased since 2020, larger transactions have remained resilient, particularly those of late-stage and launched assets. The average oncology M&A deal value in 2023 was higher than any of the previous four years, and 1.8x the 2019-22 average, even when the contribution of Pfizer’s $43bn acquisition of Seagen is excluded from the analysis (see Figure 1).