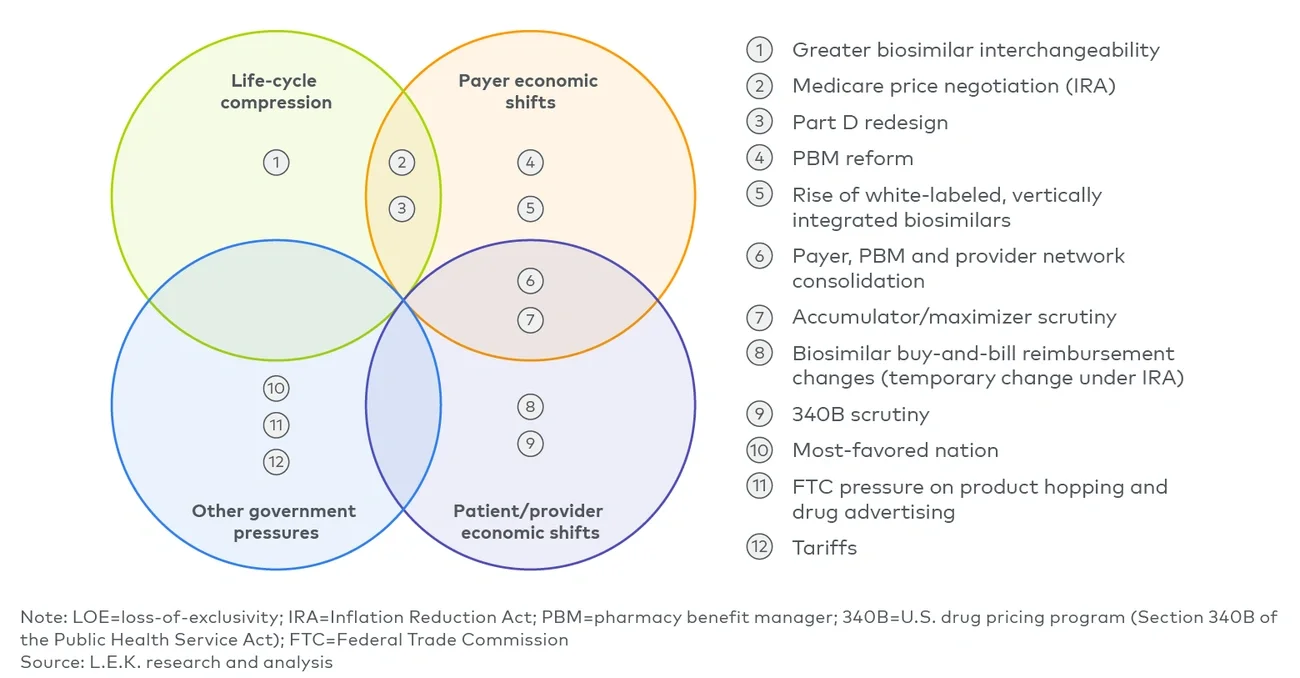

All pharmaceutical franchises must come to an end. Between 2025 and 2030, over $300 billion in prescription (Rx) drug revenues are expected to lose exclusivity. Traditional loss-of-exclusivity (LOE) strategies — including product/patent hopping, authorized generics and brand-for-generic contracting — are well known. However, several emerging trends and policies have added pressure to the drug life-cycle and/or the ability to effectively implement such strategies (see Figure 1).

Executive Insights

Not Dead Yet: OTC and DTC Approaches in Creating Value for Late-in-Life-Cycle Pharmaceuticals

Not Dead Yet: OTC and DTC Approaches in Creating Value for Late-in-Life-Cycle Pharmaceuticals

May 26, 2026

Key takeaways

Pharmas are facing substantial losses of exclusivity (LOE) over the next few years coupled with ongoing pressures from policies and trends in the U.S. healthcare ecosystem.

With the introduction of the additional condition for nonprescription use (ACNU) pathway, over-the-counter (OTC) approaches are expanding as a life-cycle management tool.

The direct-to-consumer (DTC) channel has accelerated due to anti-obesity competition and Most-Favored-Nation policy, providing a new marketplace for late-in-life-cycle product sales.

Biopharmas should carefully plan for LOE, adding OTC and DTC levers as potential tactics for consideration.

Figure 1

Policies and trends impacting LOE strategy

Image

As pricing policy, payer economics and patient purchasing channels evolve, biopharmaceutical companies need to evaluate whether selected mature assets can preserve value through self-care migration via over-the-counter additional condition for nonprescription use (OTC-ACNU), targeted cash-pay access through manufacturer direct-to-consumer (DTC) platforms or both.

Over the past approximately 12 months, two new significant programs have launched, with the potential to expand value creation from late-in-life-cycle drugs:

- OTC-ACNU, a new option for converting Rx drugs to OTC, which went live in 2Q2025, though no OTC products have been approved through it yet

- DTC platforms, with TrumpRx launching in February 2026 following manufacturer platforms (2024-present) and Most-Favored-Nation (MFN) dealmaking (September 2025-January 2026)

In this edition of L.E.K. Consulting’s Executive Insights, we discuss OTC-ACNU and DTC as potential life-cycle management tools for preserving value.

ACNU: A new option for Rx-to-OTC conversion

In the U.S., medications can be acquired through two routes: Rx and OTC. Rx drugs are dispensed by pharmacies, leaving patient oversight and counseling responsibilities to the clinicians who write the scripts. OTC drugs are sold directly to consumers with standardized “Drug Facts” labeling and usage instructions. They are safe and effective for self-directed use when taken as labeled. Typically, these are high-volume drugs for mass consumption, indicated for non-life-threatening diseases and made available at relatively low price points.

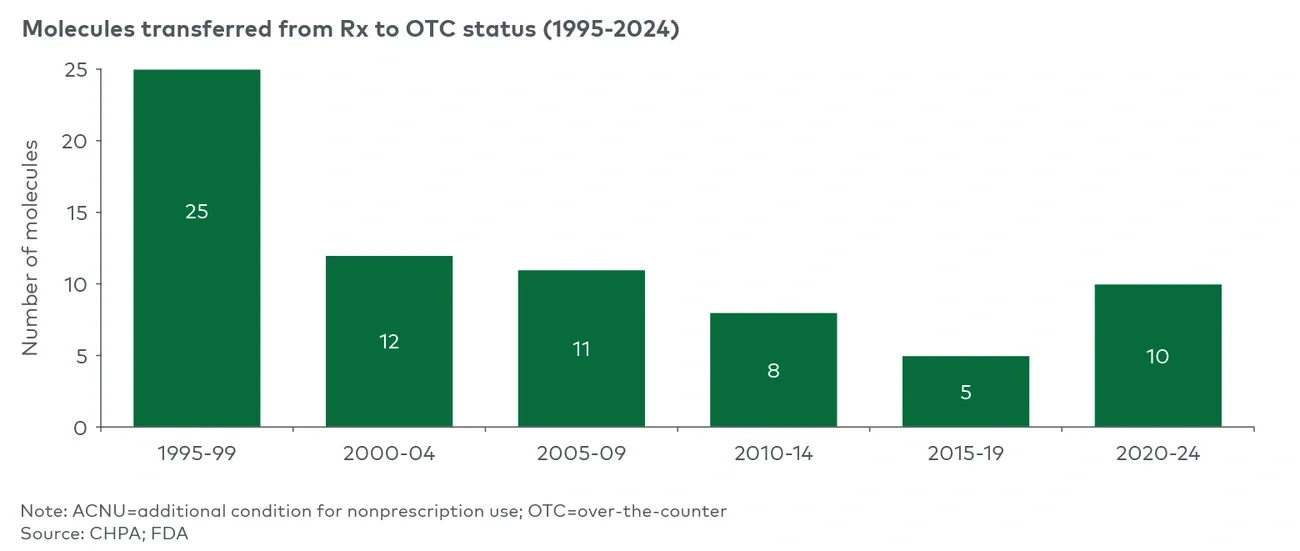

Rx drugs can be converted to OTC, which may help expand their market while adding three years of market exclusivity if supported by the proper clinical studies and filings. After declines since the mid-1990s, there has been recent growth in Rx-to-OTC conversions, which may reflect evolving Food and Drug Administration (FDA) openness to OTC conversions (see Figure 2).

Figure 2

ACNU poised to accelerate a recent reversal in Rx-to-OTC decline

Image

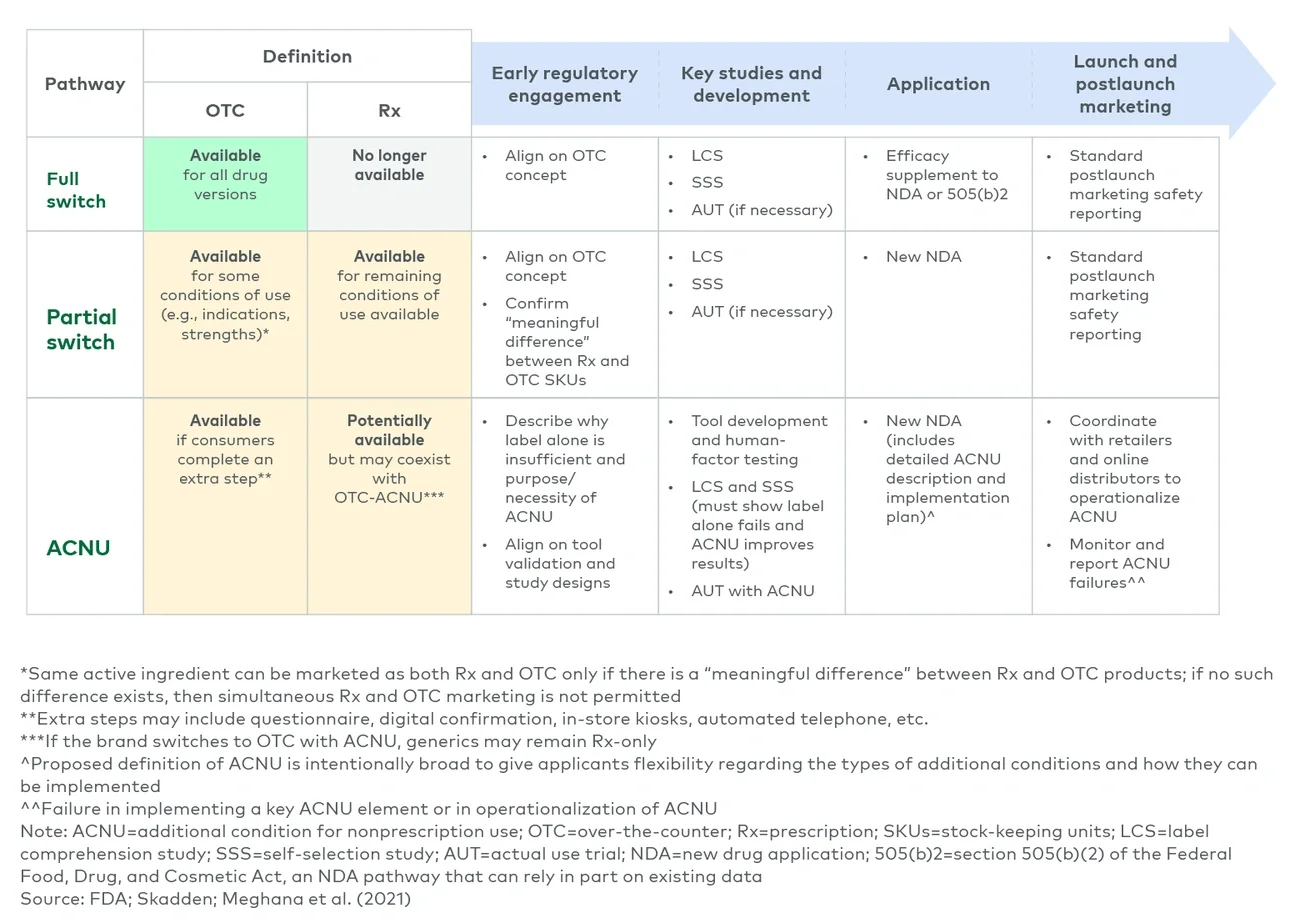

Traditionally, Rx-to-OTC conversions could be executed through a “full switch” or a “partial switch” (designating certain conditions of use to be OTC or Rx), but were limited to drugs that were clearly safe and appropriate for self-selection and self-use.

At the end of 2024, the FDA announced a new option for Rx-to-OTC conversions when paired with ACNU (see Figure 3). This option aims to expand the set of drugs appropriate for OTC use. Previously, OTC designation was focused on drugs that could be safely used based solely on consumer-friendly labeling. ACNU introduces an extra step for self-selection, such as a questionnaire, a required digital video or an automated telephone response system. Unlike traditional pathways, ACNU products can exist as both Rx and OTC, allowing for greater flexibility across patients and providers.

Figure 3

ACNU introduces a new “third way” to OTC use

Image

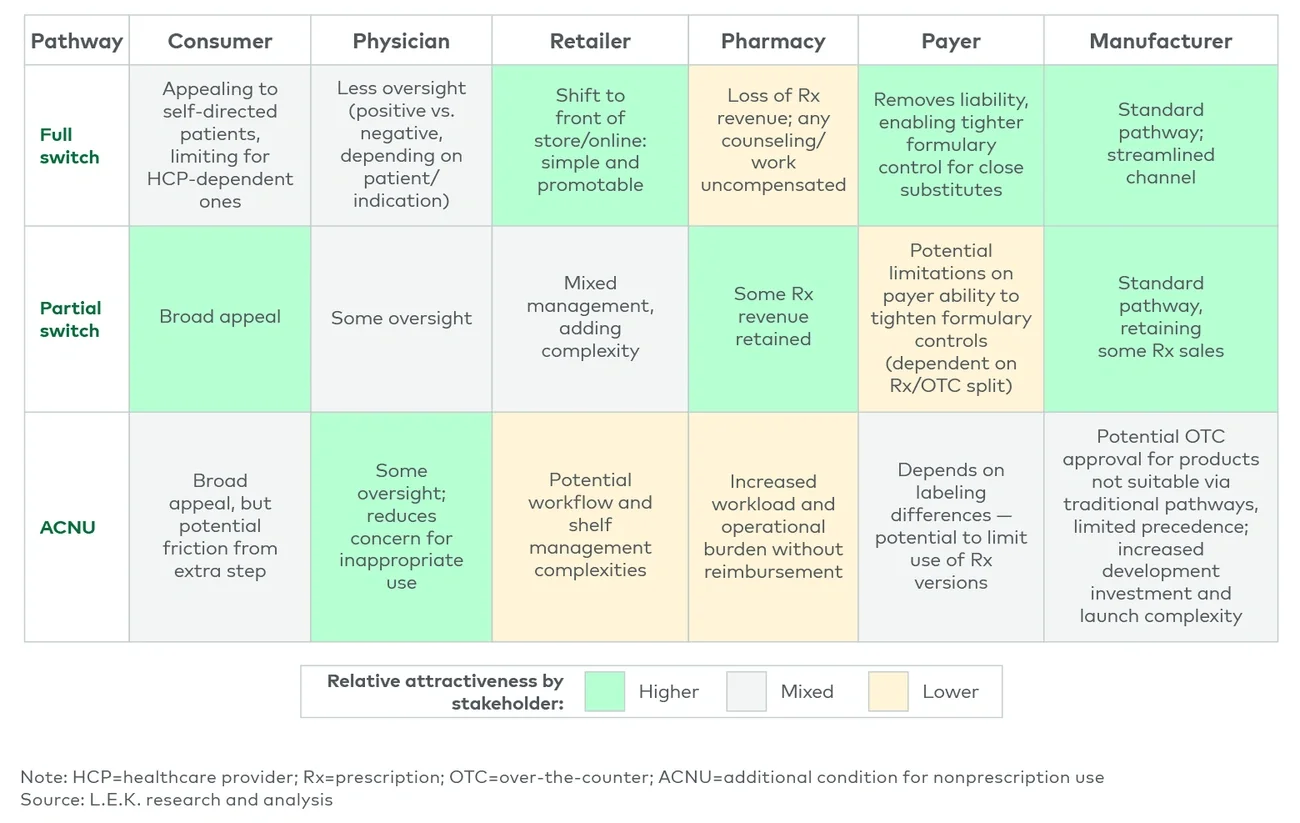

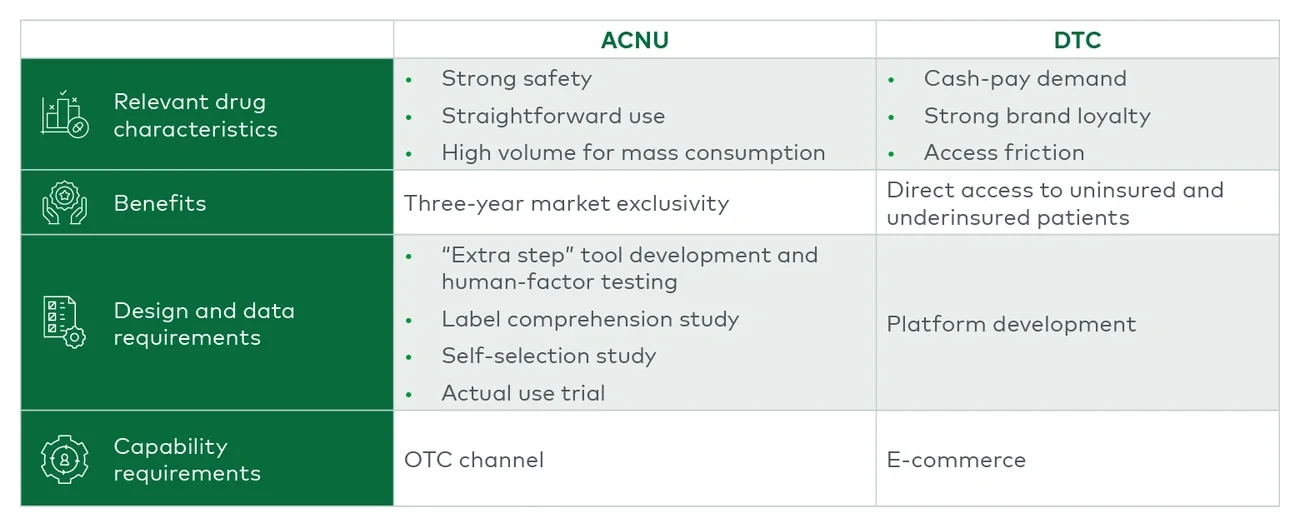

This differs from the partial switch OTC path, which allows for Rx and OTC sales with meaningful differences (e.g., indications, strengths). The ACNU definition is intentionally broad, allowing manufacturers flexibility in tailoring the extra step. This flexibility may prove important as manufacturers balance clinical risk, user experience and preferences across stakeholders (see Figure 4).

Figure 4

Pathway selection must balance the motivations of stakeholders across the value chain

Image

While still an emerging pathway with limited precedent and operational uncertainties, ACNU may make OTC conversion more feasible for patient-directed care across a broader set of drugs (e.g., statins, asthma inhalers, migraine medications). With less prescriptive ACNU guidance, there remains significant operational questions open for the initial pathway approvals to tackle. Manufacturers willing to invest in the required studies and market-shaping activities may benefit from extended exclusivity and a new purchasing channel.

For assets with strong safety profiles and straightforward patient use, ACNU may expand the drug life-cycle beyond the Rx years.

TrumpRx: A central platform for DTC sales

The expansion of telehealth, accelerated by the COVID-19 pandemic, together with the strong demand for anti-obesity medications prompted several manufacturers to launch their own DTC platforms. Lilly announced LillyDirect in early 2024, offering a digital pharmacy coupled with access to telehealth and in-person providers and educational information; it’s focused on patients with obesity, migraine and diabetes. Notably, it offers patients the option to self-pay at a discount to list price, outside the traditional insurance benefit. Other manufacturers followed suit, launching their own platforms, including PfizerForAll and NovoCare Pharmacy, through early 2025.

An executive order issued in May 2025 increased focus on DTC, making it one of the four pillars of the Trump administration’s MFN pricing policy. After receiving letters from the administration, 17 pharmas struck deals addressing each of the MFN pillars.

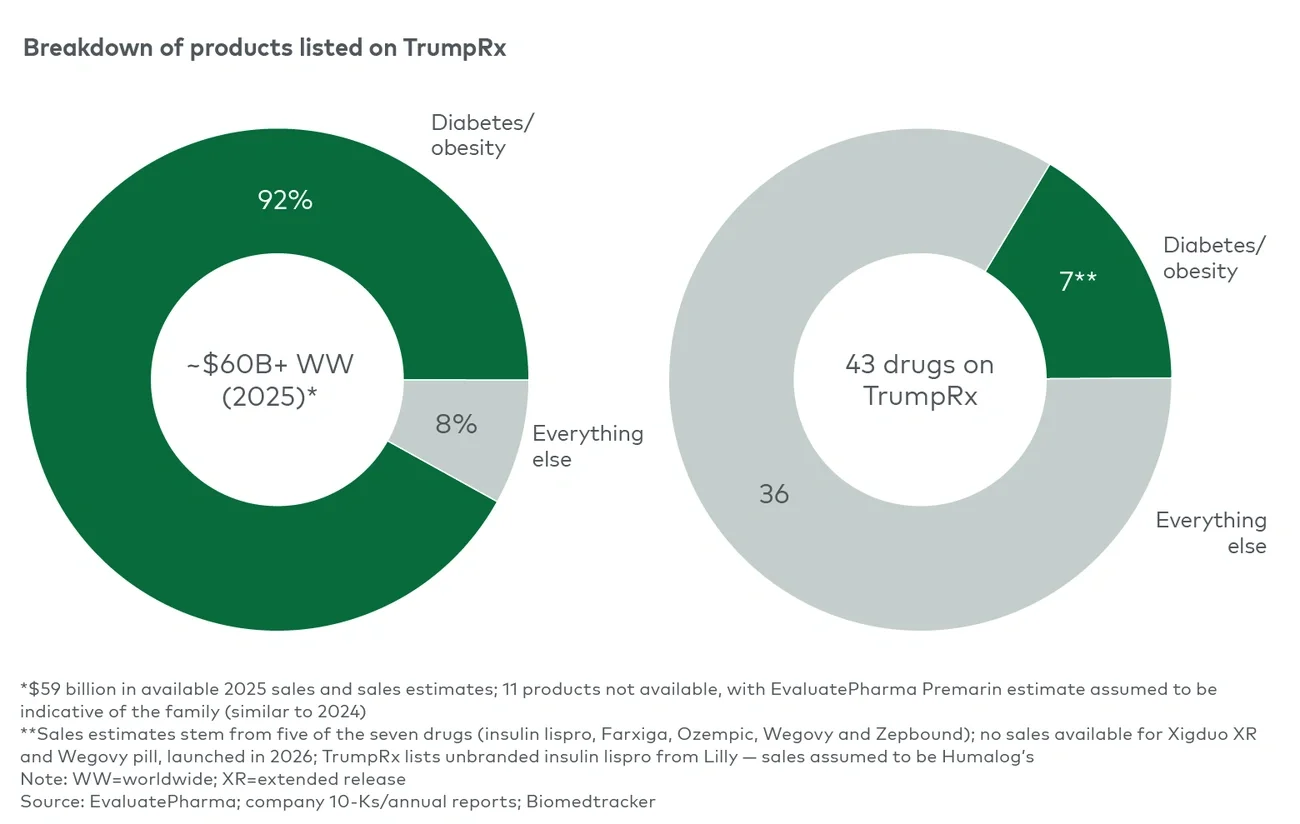

TrumpRx launched on Feb. 5, 2026, with 43 drugs from five manufacturers. The site advertises MFN pricing through GoodRx-powered pharmacy coupons or pass-throughs to manufacturer sites. Diabetes and obesity are the clear centerpiece of the initial portfolio, with the roughly seven indicated drugs representing over 90% of the estimated 2025 worldwide revenues associated with the portfolio (see Figure 5).

Figure 5

The initial Trump Rx “portfolio” sales are primarily in diabetes/obesity

Image

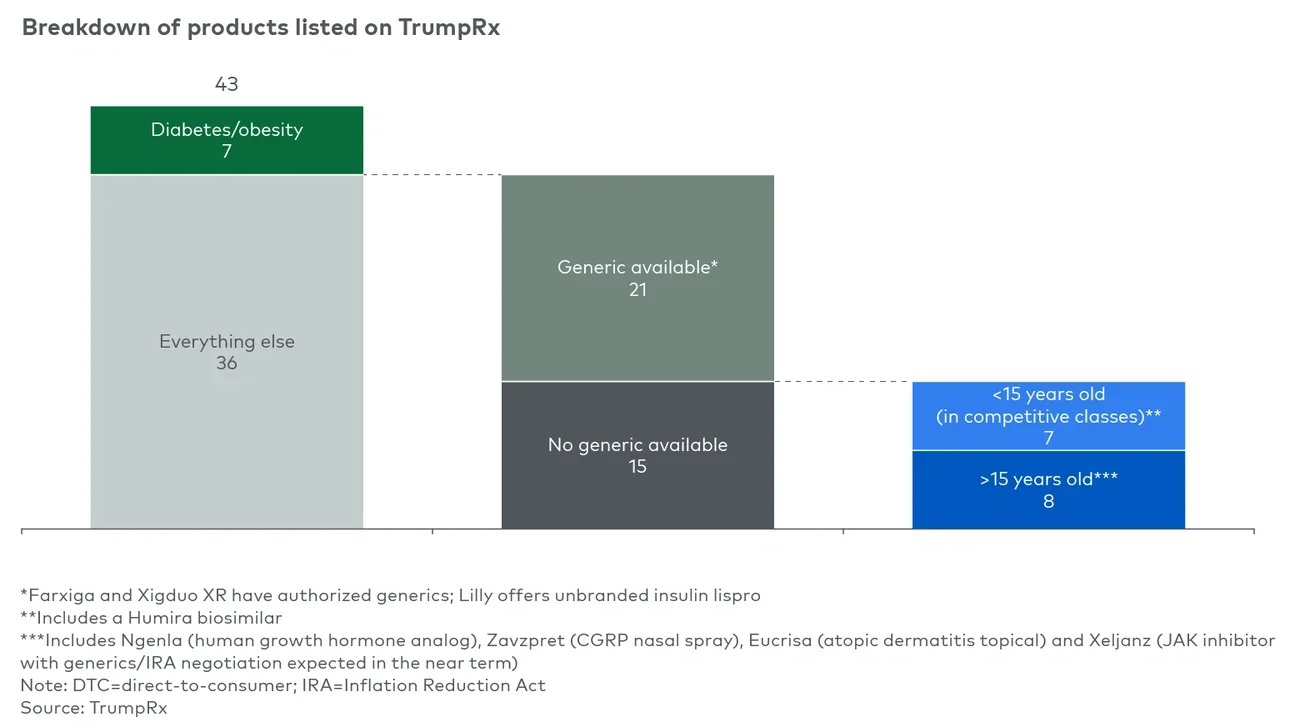

Many of the remaining products appear older, with about 80% of these drugs genericized or more than 15 years old and others in competitive classes (see Figure 6). Likewise, brands added to TrumpRx later and brands mentioned for DTC in MFN deals and not yet on TrumpRx largely share similar characteristics: They’re at or nearing the end of their life-cycle or in a competitive class.

Figure 6

Trump Rx is primarily enhancing DTC opportunities for late-in-life-cycle products

Image

For most patients, DTC and TrumpRx are unlikely to be transformative — patients can access their medications or generic equivalents through insurance with a lower out-of-pocket cost. However, this provides a consolidated channel for patients who are uninsured or underinsured or who might prefer branded options. It allows manufacturers to cut out some of the traditional drug channel intermediaries, enabling the discount pricing.

For assets with cash-pay demand, brand loyalty or access friction, DTC may create a targeted late-life-cycle channel even if it does not reshape access for the broader market.

Next steps for biopharmas

Both ACNU and TrumpRx are live, and precedents are still being set, for biopharmas with assets approaching LOE in the next two to five years. Strategic decisions being made over the next 12 to 24 months will determine which companies capture value from these channels and which cede it to generics and intermediaries by default. In planning for LOE, biopharmas should consider the full suite of strategic levers. OTC-ACNU and DTC platforms, such as TrumpRx, serve as two newer methods with different requirements for execution.

Image

If you are evaluating strategies for capturing value for mature and late-in-life-cycle products, including OTC, DTC or other LOE defense strategies, please contact us. For more information on DTC strategies, please see our recent article on the topic. We have also published on consumer health OTC considerations, please see our recent article.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC

Related insights

You might also be interested in these insights.

English