Our analysis highlights two primary characteristics that contribute to the commercial success of acquired assets: their strategic positioning within the lead indication and being first in class in their mechanism of action.

-

Assets that target patient populations in the early stages of the treatment pathway (e.g., first-line therapy) of their lead indication generally exceed expectations. For instance, Takeda’s Takhzyro disrupted the prophylactic standard of care in hereditary angioedema, becoming the preferred first-line treatment. Similarly, BMS’ Reblozyl represented a new approach to treating anemia in beta-thalassemia as an alternative or supplemental option versus red blood cell transfusions, which were a suboptimal standard of care.

-

Innovativeness is another key determinant of success. Assets with a novel, first-in-class mechanism often surpass expectations. Examples include Novartis’ Zolgensma and Roche’s Esbriet, both first-in-class lead assets acquired from biotech companies that significantly outperformed analyst projections. These pioneering assets saw both a rapid uptake and a higher-than-anticipated adoption level, which analysts had initially underestimated. On the other hand, “me-too” assets entering an already saturated market face more significant challenges in gaining traction and adoption.

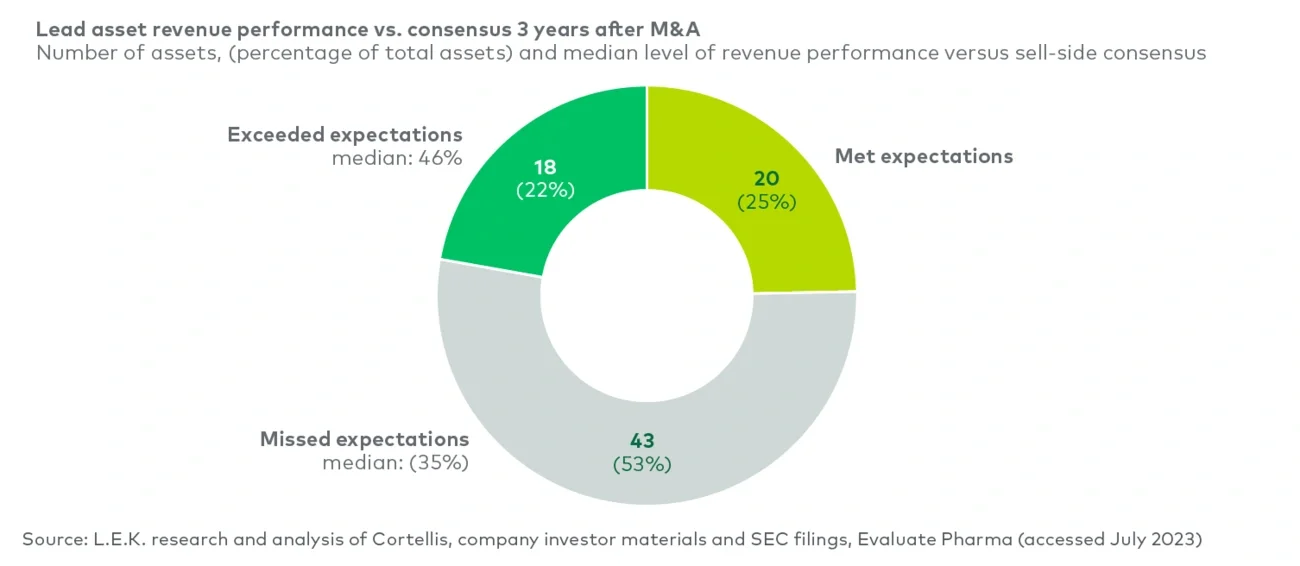

Surprisingly, there was no marked difference in the proportion of assets underperforming projections between those acquired at a clinical stage and those already on the market at the time of acquisition. It might be presumed that uncertainties in regulatory outcomes and product labeling for assets still in development could lead to less accurate prelaunch revenue projections.

We also examined the correlation between the disease indication of acquired lead assets and the buyer’s existing therapeutic footprint to determine the potential impact of established clinical and commercial proficiency on the accuracy of revenue projections and the overall performance of the product post-acquisition. In our analysis, we define an acquirer’s core therapeutic areas as those where they have established commercial capability, evidenced by the presence of at least one product already in the market, and a depth of clinical knowledge, evidenced by at least one asset in mid-to-late-stage development.

More than three-quarters of the M&A transactions evaluated in this analysis focused on a primary asset that targets a core therapeutic area of the acquirer. Lead assets integrated within an acquirer’s core therapeutic area generally fare better. About 50% of these assets meet or exceed pre-transaction consensus projections, while 63% of assets in noncore adjacent therapeutic areas fall short of pre-deal expectations. Furthermore, when lead assets outperform consensus, those targeting the acquirer’s core therapeutic areas tend to surpass expectations by a larger margin compared to those in adjacent areas. This pattern does not hold true in terms of launch timing of acquired lead assets — they are similarly delayed in both assets targeting core and adjacent therapeutic areas.

Unleashing the full potential of M&A

Despite the challenging funding landscape faced by biotech companies, they remain at the forefront of biomedical innovation and continue to contribute about two-thirds of the industry’s clinical-stage pipeline.

This extensive biotech innovation pool offers a significant range of attractive M&A prospects for pharmaceutical companies. Over 130 publicly traded biotech companies, each with a market capitalization ranging from $1 billion to $30 billion today, are poised to become potential acquisition targets within the next two years, excluding the recent trio of acquisitions of Ambrx, Harpoon and Calypso early in this year. These companies hold valuable assets that are either already in the market or in advanced stages of development, with major clinical milestones expected before the end of 2025, making them appealing for strategic acquisitions.

For biopharmaceutical executives aiming to navigate this M&A landscape successfully, it is essential to focus on the following five strategic priorities:

-

Establish defined M&A objectives: To ensure sustained growth, pharmaceutical companies must regularly refresh their R&D pipeline and existing in-line product mix. This involves internal portfolio prioritization and external strategic acquisitions. Senior leaders must set distinct goals regarding the scale, frequency and timing of M&A needs for their business development teams. These objectives should focus on establishing criteria for disease indication selection for acquisition, assessing the expected revenue impact and timing of acquisitions, and appraising the degree of novelty of assets involved in these transactions. With these guidelines, M&A practitioners can then construct detailed business development roadmaps, outlining an optimal sequence of acquisitions needed to fill internal growth gaps.

Business development leaders must consistently ensure that their actions are in sync with the company’s broader strategic vision. Such alignment helps avoid the frequent problem of reevaluating a deal’s strategic rationale during the advanced stages of due diligence.

Establishing and following clear, specific objectives from the beginning enable companies to conduct their M&A activities in a strategically sound and efficient manner, leading to successful deal closures. This strategy also promotes seamless acquisition integration and optimizes the value obtained from each transaction.

-

Enhance value with in-depth insights: In the world of mergers and acquisitions, it is imperative for deal makers to conduct a thorough evaluation of potential acquisition targets, paying close attention to the ramp of projected revenue and anticipated launch timelines, especially within the first years following the acquisition. This time frame is crucial as it is frequently marked by variances between the anticipated investor returns and the actual post-deal performance.

To ensure a realistic assessment, deal makers should adopt a comprehensive approach that includes both internal market insights and external benchmarks. This should involve an analysis of the past performance of similar assets in comparable markets, considering factors like pricing and access barriers, competitive dynamics, and operating investment requirements to win. In doing so, they should also recognize the potential for revenue uplift when an acquired asset is integrated into the expansive network and the deep-rooted expertise of a leading pharmaceutical company. While our analysis did show that many acquired assets fall short of expectations, high-quality assets tend to thrive within a larger, more scaled commercial organization, benefiting from its unencumbered infrastructure. Conducting this level of in-depth and balanced analysis is important for unlocking greater performance and value from promising assets while de-prioritizing those M&A candidates with poor and risky prospects.

-

Understand the risk of unrelated diversification: Pharmaceutical companies continually seek to refine and expand their therapeutic footprint to drive sustainable growth. Diversifying revenue streams has its advantages, but assessing the value of M&A targets that venture into new or unrelated therapeutic areas poses unique challenges. Our analysis shows that acquired assets tends to perform worse the more distant they are from the acquirer’s existing operational expertise, current sales force channels and established provider relationships. Deal leaders need therefore to engage with external advisors who possess up-to-date expertise in the target’s disease areas. These specialists can provide invaluable insights, helping construct fair and precise valuation estimates, and uncover even the smallest potential synergies.

Additionally, deal makers must factor in the possible depreciation in value of acquired assets after integration. This entails recalibrating the expected growth of these assets, particularly in situations where key talents from the acquiree, who were essential to the target’s success, leave the company. Conducting a comprehensive risk assessment in this context allows for a more judicious decision-making process. It helps in weighing the advantages of diversification against the risks associated with expanding into new therapeutic areas.

-

Uphold objectivity and be willing to walk away: In the demanding final phase of deal evaluation, where diverse stakeholders including bankers and legal advisors are involved, it is imperative for deal leaders to maintain both accuracy and objectivity. They should avoid the trap of using misleading accuracy or engaging in false precision to justify and close a deal.

Despite the noticeable increase in acquisition premiums over recent years (rising from an average of 59% before 2015 to 94% after 2018, as per our analysis), it is critical for acquirers to avoid overpaying. A meticulous, unbiased assessment is key, coupled with a strategic focus on uncovering potential commercial upsides and significant synergies. By adopting this approach, decision-makers can ensure that their investment choices are not merely a response to the prevailing trend of high acquisition costs but are grounded in a thorough understanding of the target’s true potential value.

-

Cultivate superior M&A capabilities: Executives in the biopharmaceutical industry need to go beyond investing in deal sourcing and evaluation. It is critical that they substantially increase their resources and refine their processes to attain mastery in deal integration, a key to post-merger operational excellence. Proper acquisition integration is vital to avoid delays in launch and to adeptly handle the operational complexities that arise post-merger. This encompasses a wide array of integration tasks, such as defining governance and decision rights along the M&A process, effectively communicating across teams, identifying and addressing potential issues early on, and ensuring a seamless blending of cultures and systems between the two companies. By doing so, companies can not only enhance the effectiveness of their M&A activities but also maximize the value and growth opportunities presented by each acquisition.

In the increasingly competitive M&A landscape, the frequency and magnitude of transaction experience are becoming key elements that set apart potential buyers. A consistent track record in deal-making markedly bolsters a company’s proficiency in M&A. Regular engagement in acquisitions, even at a modest pace of one transaction every two years, has the potential to develop and evolve an organization into a proficient and systematic serial acquirer.

When implemented successfully, these five strategic priorities will empower M&A professionals to more effectively and efficiently identify, assess and integrate deals, thereby securing a competitive advantage in the market. By concentrating on developing strong and scalable M&A capabilities, acquirers will not only streamline the acquisition process but also guarantee maximum value extraction from each transaction.

The authors would like to thank Jonathan Fischer and L.E.K.’s Information Resources Center for their important contributions to this article.

For more information, please contact lifesciences@lekinsights.com.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2024 L.E.K. Consulting LLC

Endnotes

1The VanEck PPH index was used as reference. This analysis excludes Pfizer-Seagen and Shire-Baxalta in Year 3, and excludes Actavis-Forest in all years due to data limitations.