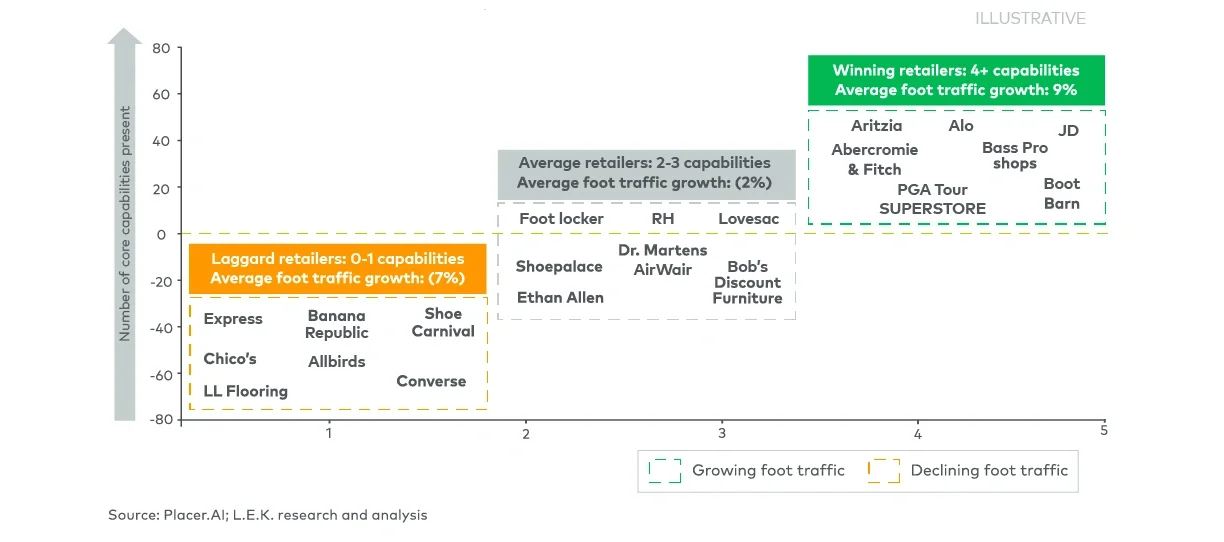

Nearly all retail growth over the past decade has come from online channels. There is no tailwind for brick-and-mortar sales. Retailers cannot compete on legacy or retail fundamentals alone. Retailers must clearly define their role in the consumer trip and consistently deliver against the capabilities that matter most. Winning retailers are those that differentiate through strategy and focused execution, while others are losing relevance and falling out of the consideration set.

Consumers are taking fewer trips to physical stores and narrowing the set of retailers they do consider. Ecommerce sales are growing roughly two to three times faster than total retail sales, fundamentally reshaping how consumers shop. As a result, shoppers are prioritizing a smaller group of trusted physical retail destinations that can meet their needs efficiently, rather than visiting multiple stores. A small set of retailers is capturing a disproportionate share of consumer visits, while others fall out of the consideration set. Across approximately 130 major U.S. retailers, the 10 highest-traffic retailers account for roughly three-quarters of total visits (around 23 billion annual visits).

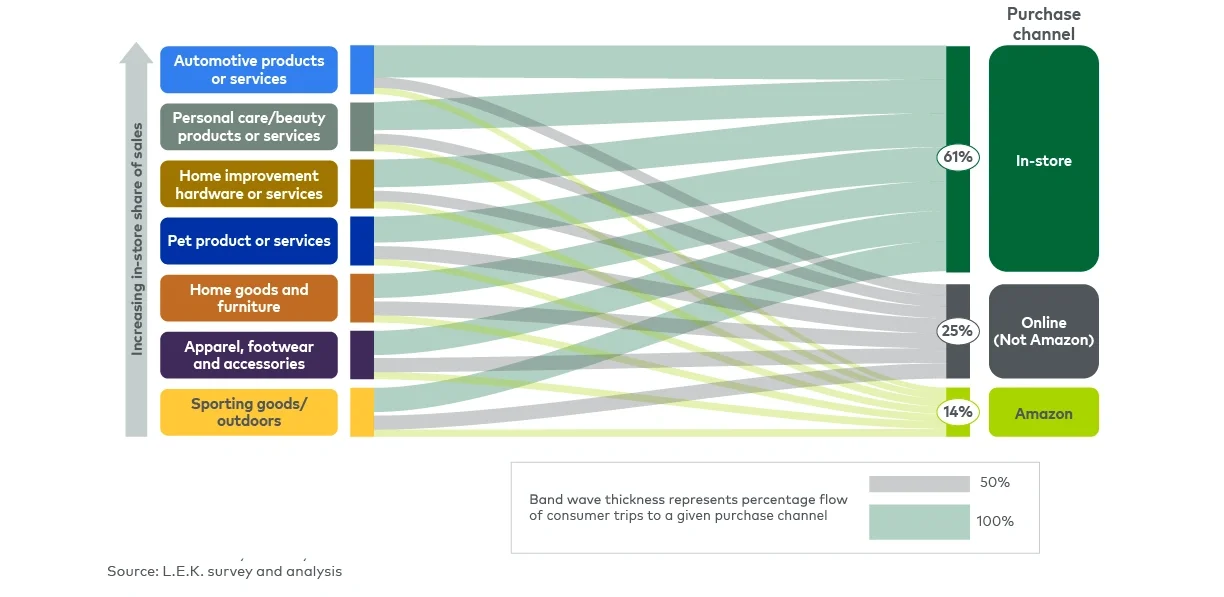

This shift is being accelerated by the continued rise of online-first players, most notably Amazon, as well as the growing advantage of mega-scaled retailers like Walmart and Target, which are capturing an increasing share of retail spend across categories. As consumers default to online channels for convenience, price transparency and speed, other retailers are accounting for a smaller share of trips (see Figure 1).