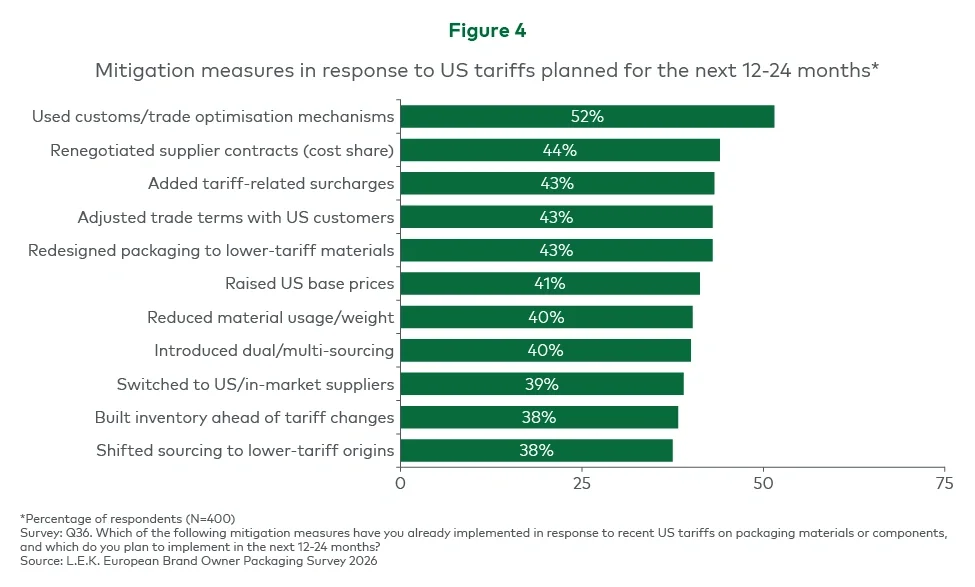

As shown in Figure 4, the most prominent planned measure over the next 12 to 24 months is the use of customs and trade optimisation mechanisms (52%). This suggests organisations are looking to manage tariff exposure through stronger classification discipline, origin planning and structured customs approaches rather than relying solely on supplier moves or inventory buffers.

Commercial levers also remain important. Just behind this, planned actions cluster around formalising cost pass-through and risk sharing across the value chain. Renegotiating supplier contracts (cost share) (44%) leads this group, while tariff-related surcharges (43%), adjusted trade terms with US customers (43%) and raising US base prices (41%) point to a more explicit and repeatable approach to recovering tariff-driven cost increases.

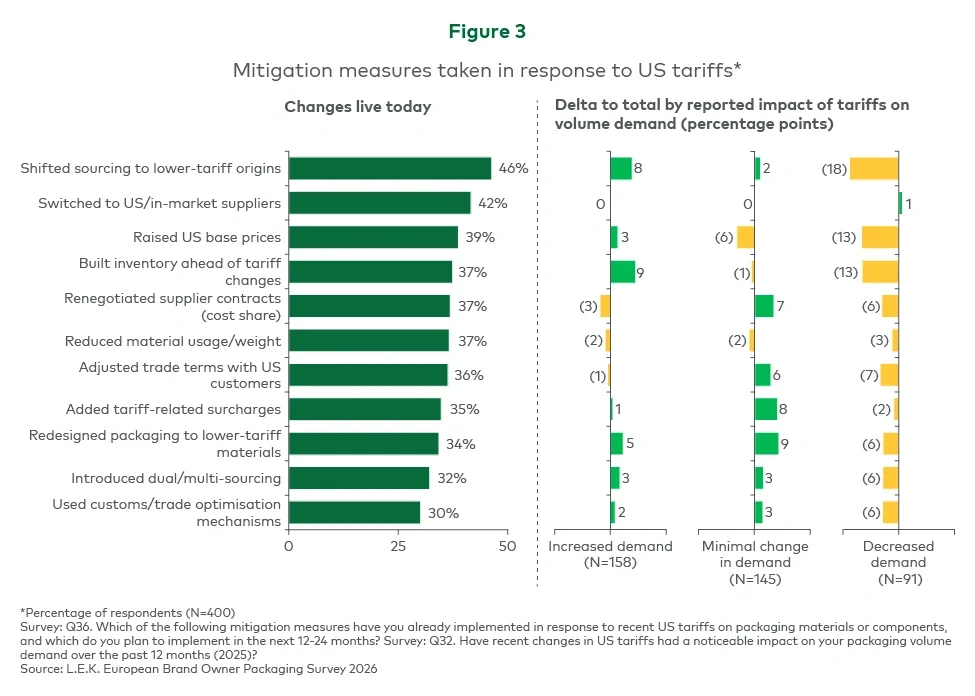

However, the ability to recover tariff-related costs is unlikely to be uniform across the market. Companies operating in premium or highly differentiated categories may retain greater pricing flexibility, while more price-sensitive segments are likely to rely more heavily on sourcing changes, redesign and supplier negotiations to protect margins.

Notably, packaging redesign to lower-tariff materials, cited by 43% of respondents, sits alongside these commercial levers, reinforcing that mitigation is increasingly being addressed at the pack specification level, not just through procurement.

Taken together, the pattern is clear. The next phase of response is less about isolated tactical moves and more about embedding tariff resilience into business as usual. The prominence of trade optimisation highlights an intent to build institutional capability, while the similar weighting of commercial levers and redesign suggests brand owners expect continued volatility and are putting in place both the contractual tools and the packaging changes needed to manage it over time.

Looking ahead: Tariffs are driving structural shifts in packaging strategy

US tariffs are pushing brand owners towards a more resilient operating model for US-bound packaging. That means more regionalised supply and in-market sourcing; more disciplined cost recovery through pricing, surcharges and contract clauses; and greater use of packaging design levers such as lightweighting and material substitution to reduce exposure and widen sourcing options. At the same time, mitigation itself can create short-term volume spikes, particularly when inventory is built ahead of changes or suppliers are transitioned, so planning needs to account for both structural shifts and pull-forward demand.

Over the next several years, competitive advantage is likely to depend increasingly on the ability to build flexibility into sourcing, packaging design and supplier networks before disruption occurs rather than reacting once costs and trade conditions change.

This article builds on earlier discussions in the series on the return of selective growth across the European packaging market and the shift from sustainability ambition to operational execution. In the next article, we examine how AI and digital tools are being applied across packaging value chains, including where they are creating practical value and where adoption remains limited.

To discuss how tariff exposure could affect your packaging strategy, sourcing model or supplier base, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting