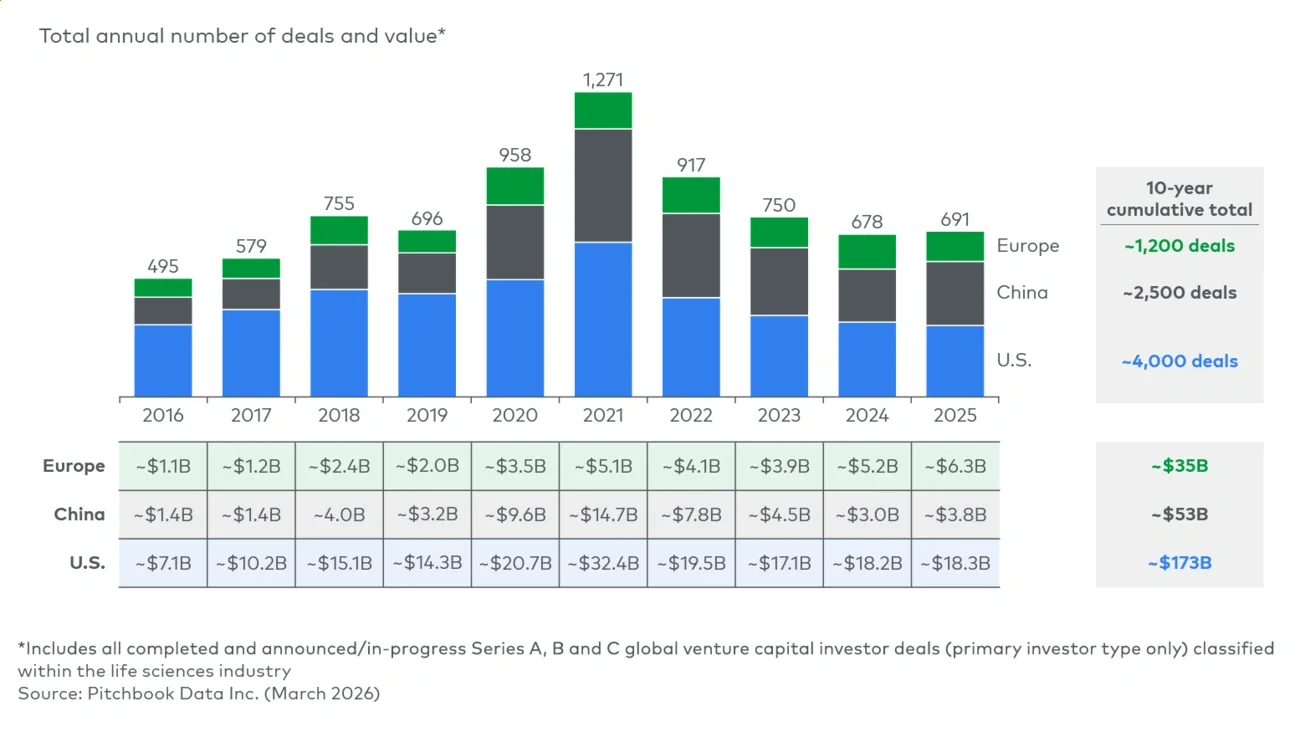

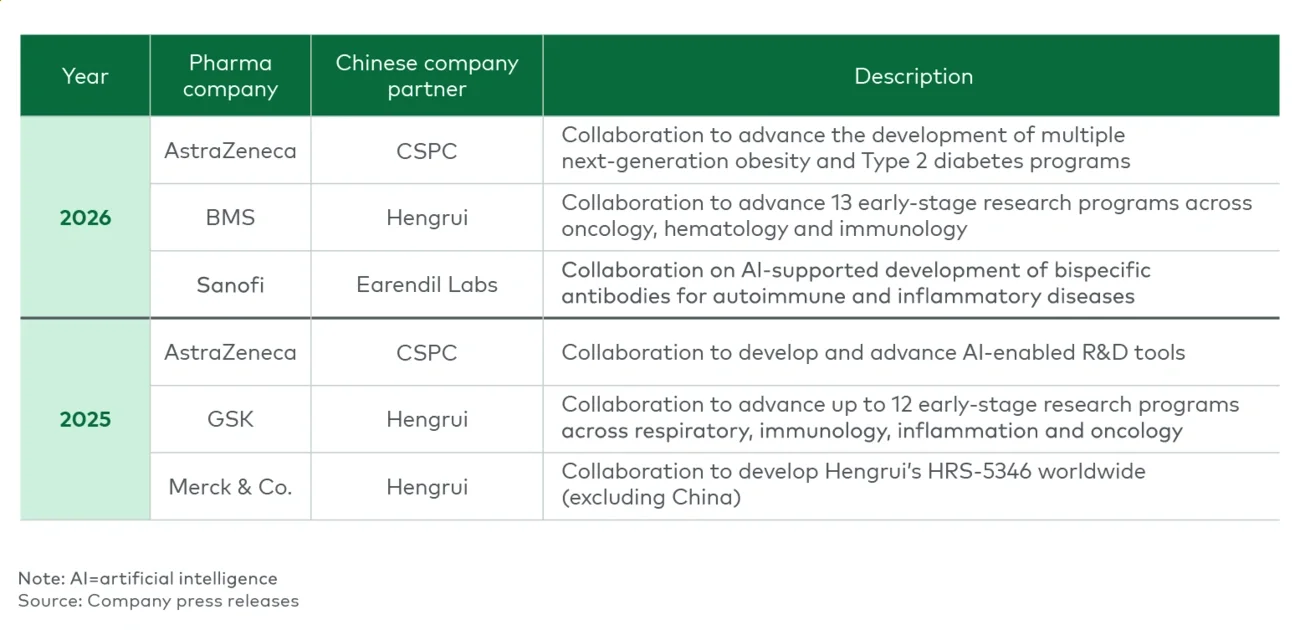

In a market where the pace and volume of innovation are accelerating, broader partnerships can help organizations build more-durable access to emerging science while reducing dependence on the success of any single program. Deeper engagement with Chinese biotech ecosystems may improve visibility into emerging targets, translational research capabilities, clinical development infrastructure and high-performing local talent networks. Over time, this can strengthen sourcing capabilities, accelerate early-stage development timelines and create a more embedded position within one of the fastest-growing centers of global biopharma innovation.

China’s expanding clinical trial infrastructure and efficient development environment also create opportunities to run faster, lower-cost early-stage studies that can de-risk novel biology before transitioning to U.S. or global development. Companies may increasingly look to China not only for asset licensing but also for translational research partnerships, platform collaborations and early proof-of-concept generation.

For biotech companies

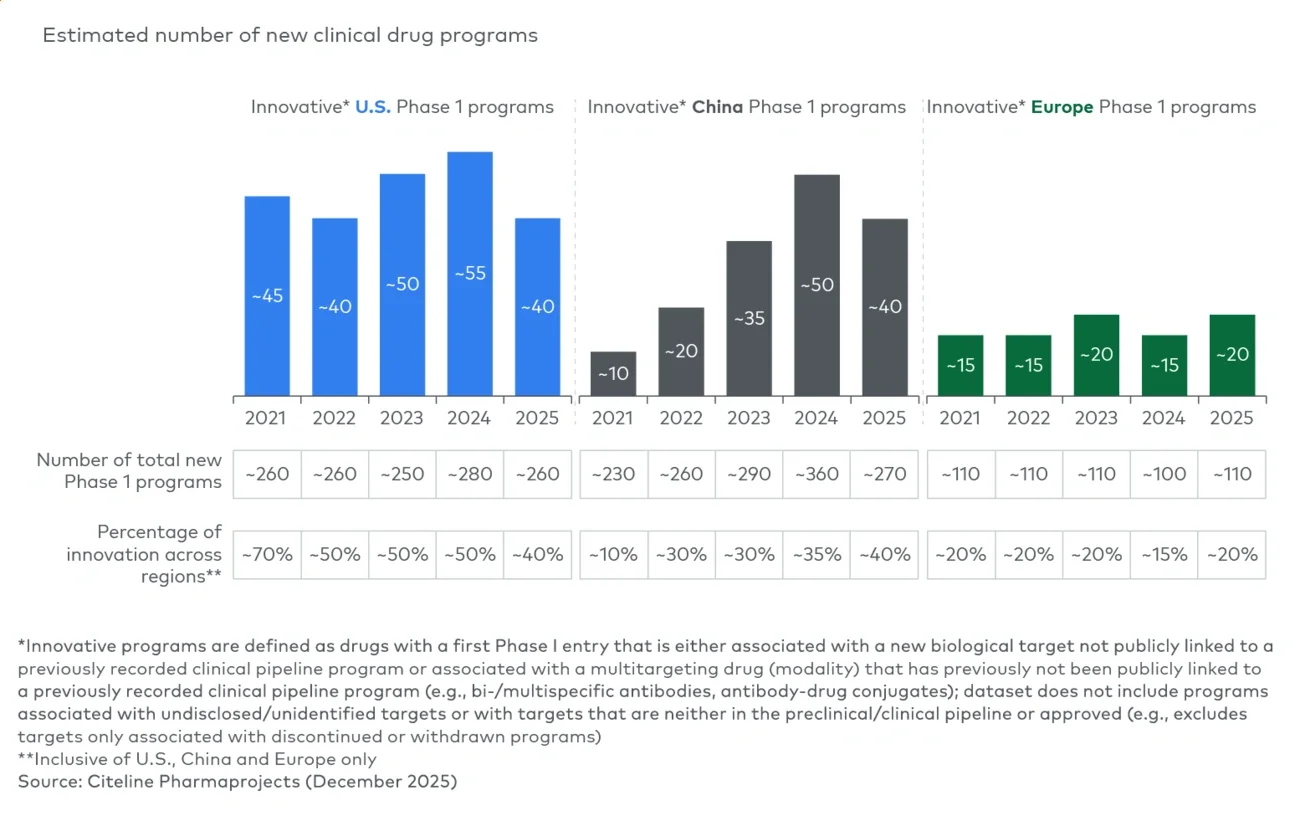

For U.S. biotech, China’s rising innovative output reinforces the need to refocus on the differentiated science that has historically defined the U.S. life sciences ecosystem. China is likely to sustain high volumes of innovative Phase I activity, supported by growing access to global licensing and partnership opportunities. As a result, U.S. companies pursuing incremental or target-following strategies may face increasing pressure in both early-stage funding and future market competition. Maintaining leadership will require continued investment in novel biology, alongside regulatory reforms that accelerate early clinical development, such as shorter time-to-Investigational New Drug application timelines and expanded pathways comparable to China’s Investigator-Initiated Trial model.

For European biotech, the implications are similar but more acute. Europe’s contribution to innovative Phase I activity has remained relatively stagnant over the past five years, with its global position falling further behind both the U.S. and China. Reversing this trend will likely require stronger investment environments, faster regulatory pathways and more coordinated support for early-stage innovation.

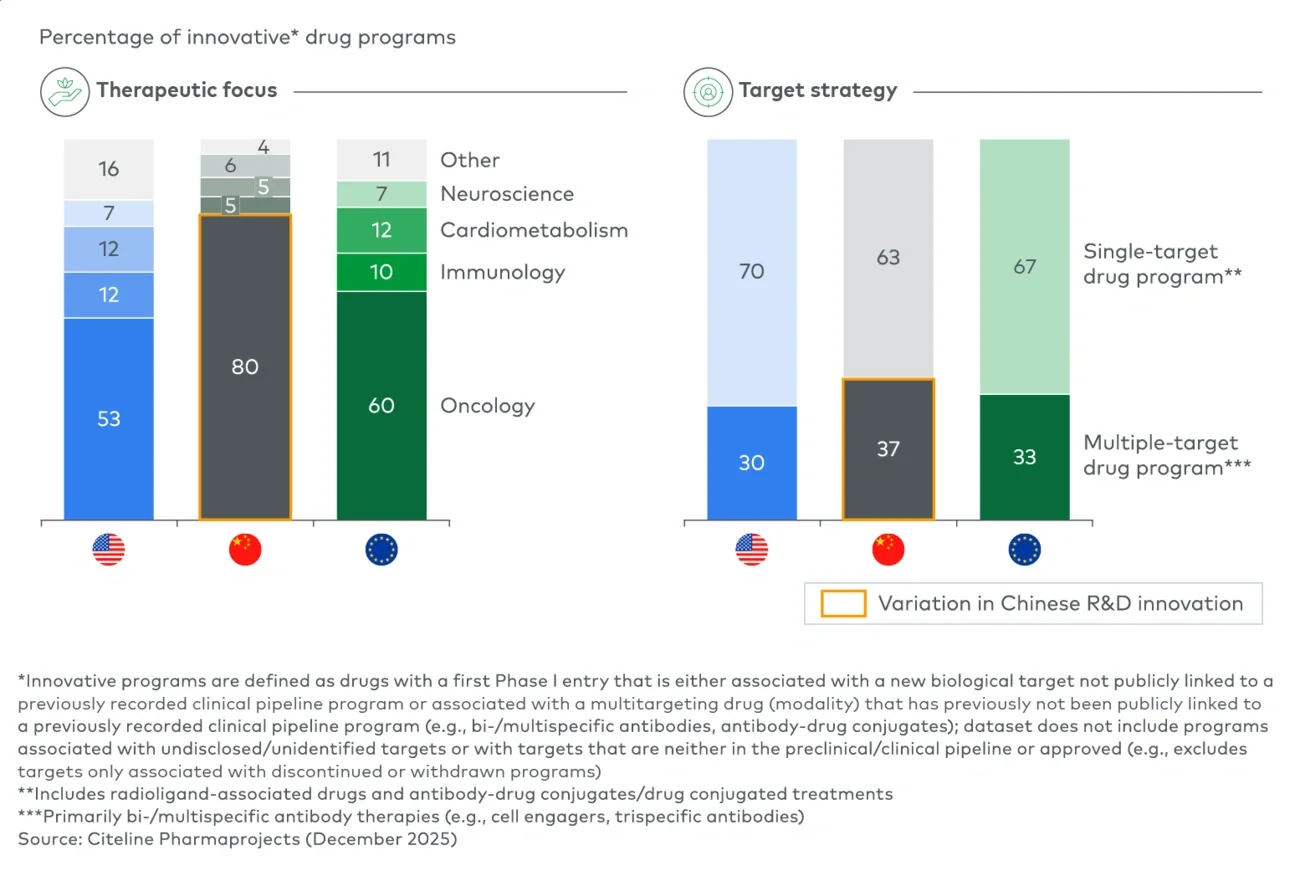

For Chinese biotech, the next challenge is converting early-stage innovation leadership into globally successful commercial products. China has rapidly evolved from a fast-follower market into a credible source of first-in-class programs, but sustaining that position will require stronger late-stage development capabilities, global regulatory expertise and commercial infrastructure. Continued ecosystem maturation, supported by venture funding, pharmaceutical partnerships and broader investment, will also be critical. At the same time, China’s concentration in oncology creates a strategic need for greater diversification into other therapeutic areas to reduce crowding and broaden long-term innovation opportunities.

Beyond these organizational considerations, China’s focused expansion toward more innovative oncology asset R&D creates a second-order consideration for the global biopharma ecosystem: balancing the growing therapeutic category crowding against the incremental improvements and natural competitive pressure associated with newer, next-generation therapies. With the right diligence, this level of therapeutic area crowding will support greater scientific validation of the most clinically feasible targets, enable a consistently higher bar for therapeutic success and best-in-class products in a competitive market, and support the need to consistently pursue the development of the most meaningful medicines. This can be beneficial to all life sciences stakeholders, ranging from the patients receiving better medicines to physicians having more drug options all the way to investors and biopharma organizations who can more confidently invest in more de-risked, clinically meaningful biology.

Conclusions

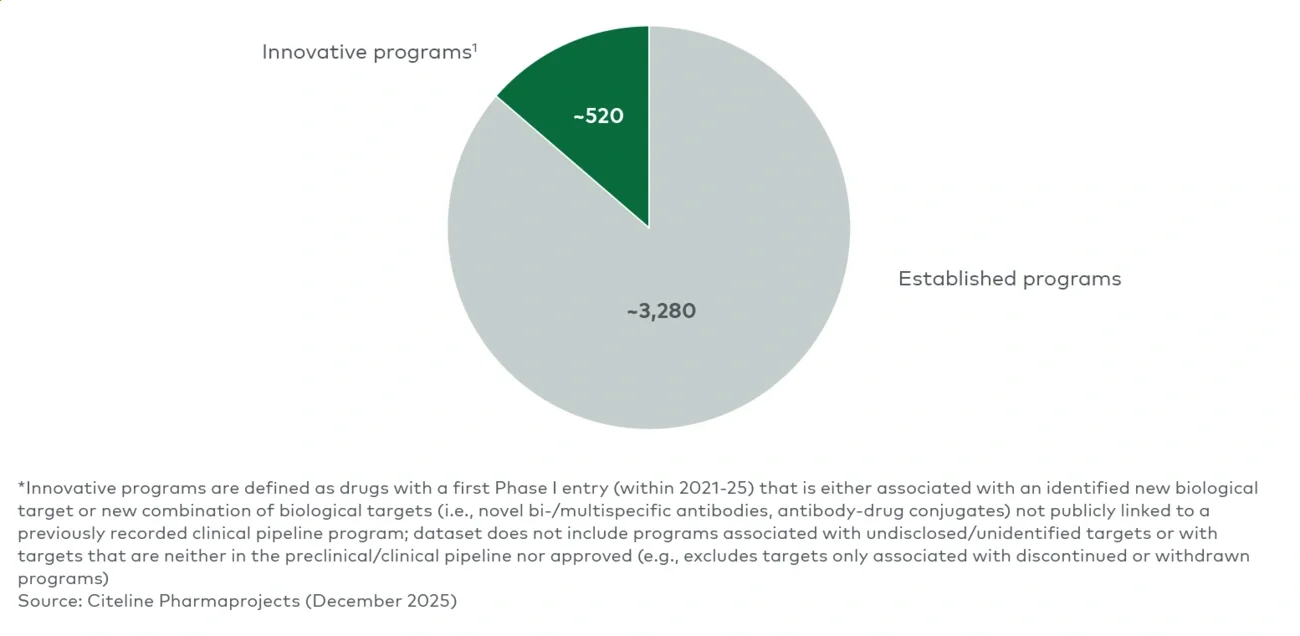

Taken together, the data makes clear that global biopharma innovation is no longer primarily centered in the West. China has established itself as a major source of novel clinical biology, reshaping how the industry sources, evaluates and competes around innovation. At the same time, the rapid growth in innovative asset volume, particularly in oncology and antibody-based, is increasing the risk of therapeutic crowding and asset commoditization across global pipelines.

As the innovation landscape becomes more multipolar, success will increasingly depend on balancing exposure across China, the U.S. and Europe while remaining selective about where to play. Organizations will need to prioritize therapeutic areas and modalities with durable differentiation and avoid overconcentration in crowded target classes. Broader partnerships with Chinese biopharma companies may also become increasingly important, providing not only access to emerging assets but also deeper insight into how leading Chinese organizations rapidly identify, develop and advance innovation.

Ultimately, competitive advantage will depend less on access to innovation alone and more on the ability to identify differentiated science, build the right strategic partnerships and translate innovation into durable clinical and commercial value.

We can help biotech and biopharma organizations navigate this evolving R&D landscape by:

- Mapping global mechanism and modality landscapes to identify differentiated opportunities and avoid overcrowded categories

- Prioritizing clinical-stage BD and M&A opportunities based on scientific differentiation, competitive intensity, development risk and return on investment

- Designing balanced China/U.S./Europe sourcing strategies that align external innovation with portfolio priorities

- Assessing when to pursue single-asset deals versus broader platform or multiasset collaborations with scaled Chinese partners

- Developing R&D strategies that optimize portfolio size, therapeutic focus and long-term commercial positioning

Additional L.E.K. reading

- Advancing Innovation and Global Reach: The Next Chapter in China’s Clinical Trial Development (November 2025)

- Is Biopharma Doing Enough to Advance Novel Targets? (May 2025)

- Oncology BD&L: Winning in an

- Increasingly Competitive Environment (September 2024)

For more information, please contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC