Executive summary

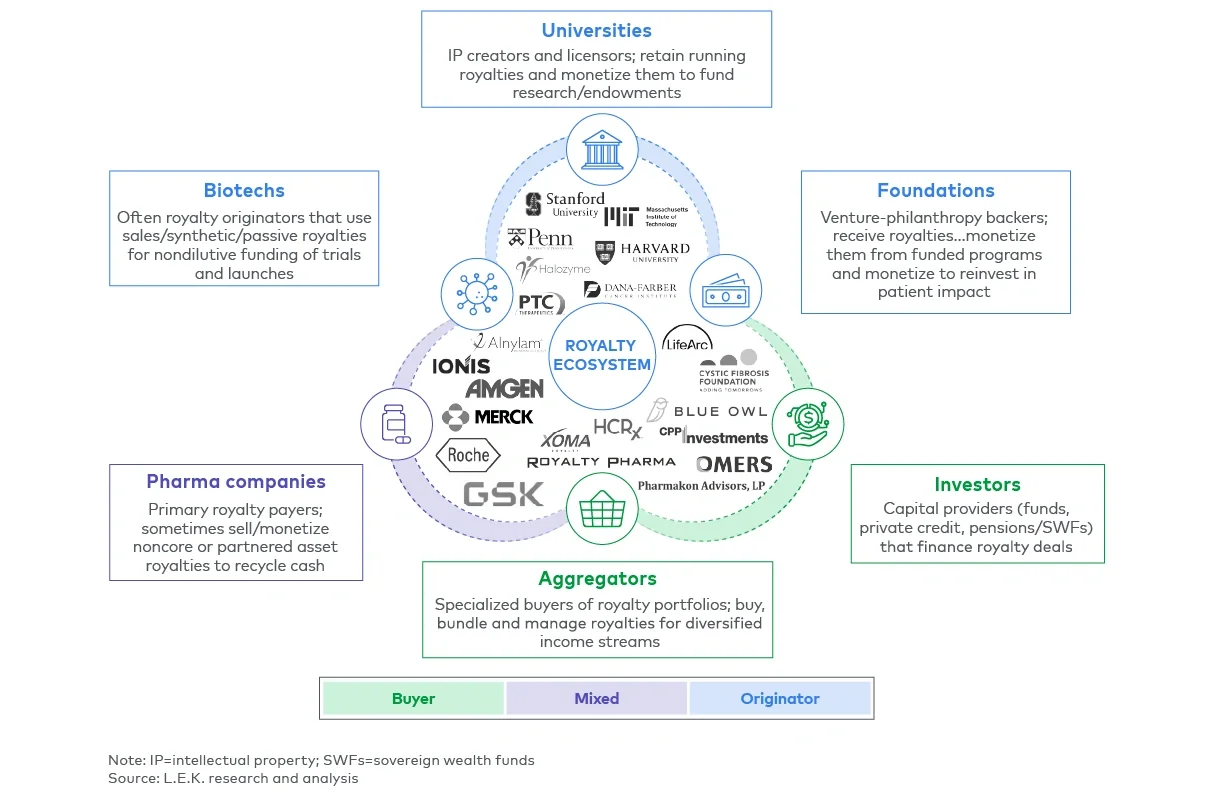

Royalty interests are more widely held than many executives realize. Beyond major pharmaceutical companies, a broad range of organizations possess valuable, often underrecognized, royalty positions. Emerging biotechs may hold royalties from outlicensed products or codevelopment arrangements. Universities and research hospitals often retain the rights to discoveries licensed to commercial partners.

Foundations such as the Cystic Fibrosis Foundation have monetized royalty streams to reinvest in research and patient programs. In addition, aggregators like XOMA and DRI actively acquire and manage diversified portfolios of royalty assets.

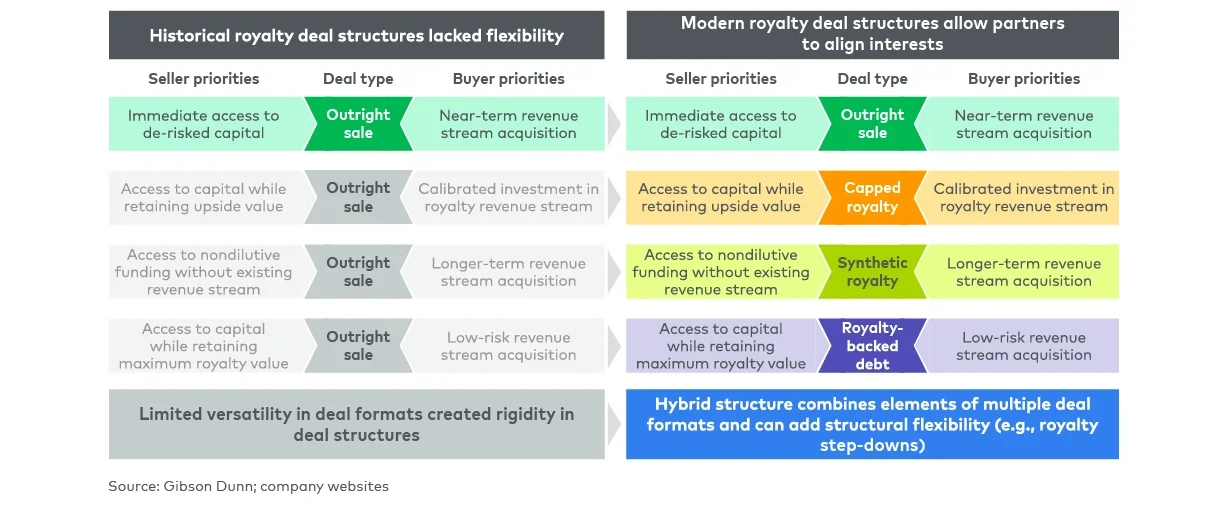

However, royalty-related financing remains an often misunderstood source of capital in the biopharmaceutical industry. Once viewed as an expensive last-resort option, nondilutive royalty funding has matured into a strategically flexible instrument that should be considered alongside more traditional equity and debt options.

As the market has matured, the range of royalty deal structures and execution pathways has expanded significantly. For management teams, understanding the pros and cons of royalty financing as well as how the varied range of royalty-focused structures best align with different strategic objectives has never been more important (see Figure 1).

L.E.K. Consulting has advised on nearly 100 royalty transactions over the past two decades. Our work has helped clients determine the fair value of their royalty assets, evaluate optimal structuring options and engage the right partners and processes to unlock value. In this edition of Executive Insights, we will share key learnings from our experience as well as considerations that should be top of mind for executives considering their capital formation options.