Implications for investors and boards

For investors, the central diligence question is shifting from “Does the company have AI features?” to “Does the company have the right to win in an AI-enabled, hybrid build-versus-buy world?” That right to win should be tested across both defence and offence.

On defence, investors should assess which product modules are easiest for customers or new entrants to replicate, where the system is protected by regulatory or integration barriers, and whether pricing is exposed to AI-driven productivity gains. On offence, they should assess the vendor’s ability to capture a new module technology acceptance model (TAM), become the AI marketplace or orchestration layer, monetise data services and support client-side innovation without losing control of the platform. The strongest HCIT assets are likely to combine mission-critical installed bases with modern integration architecture, credible AI governance, strong customer support, specialty workflow depth and a clear roadmap towards higher levels of automation. This combination is likely to command a premium, while closed, slow-moving products with weak APIs and limited AI readiness may face increasing multiple pressure.

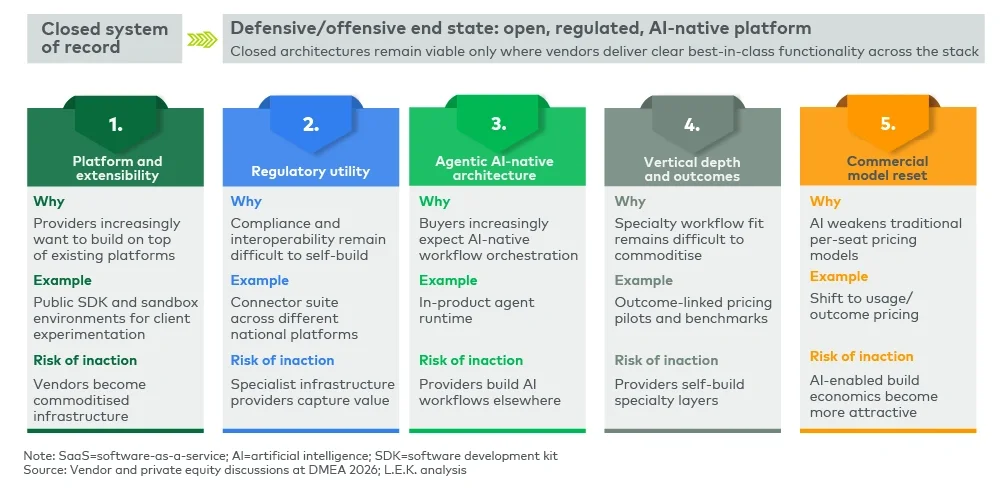

HCIT moats are shifting, not disappearing

AI will not replace HCIT systems of record overnight. The healthcare environment remains too regulated, fragmented, risk-sensitive and workflow-specific for a rapid displacement cycle. However, AI will change where value is created and captured. The edge of the stack will move faster; the core will remain protected but must become more open, more intelligent and more extensible.

For HCIT companies, the opportunity is to convert the threat into a platform strategy. By enabling customers to innovate on top of trusted systems, vendors can retain the system-of-record moat while expanding into AI workflow modules, marketplaces, data services and governance. By resisting openness, they risk encouraging customers to build around them.

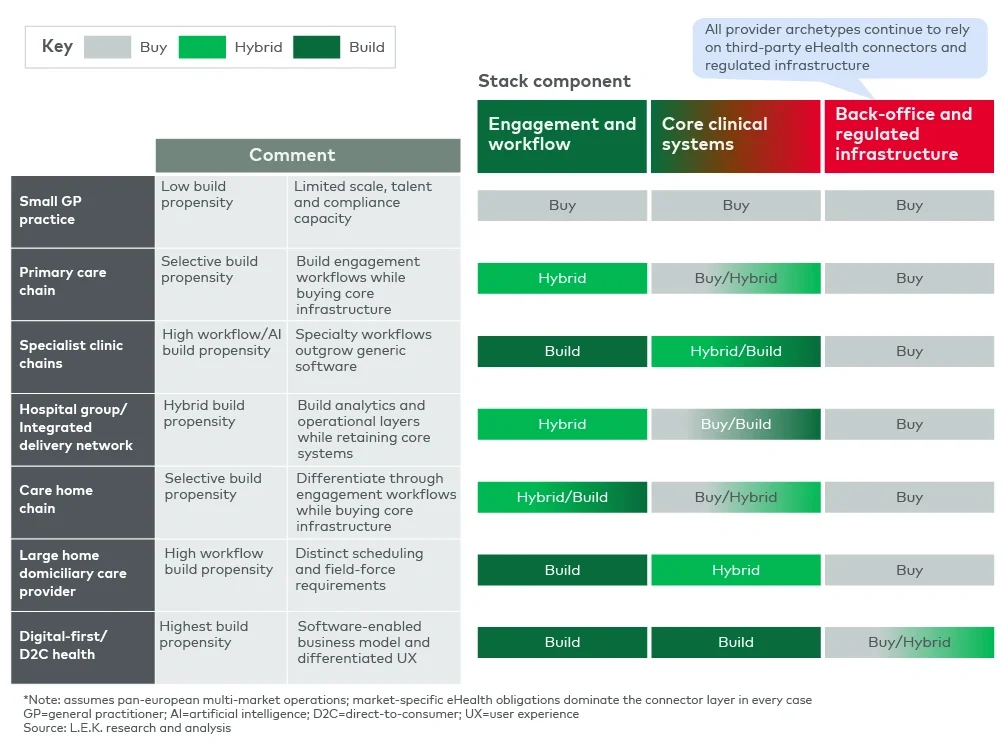

For larger healthcare services providers, the rational answer will increasingly be hybrid: build the differentiating workflow and AI layer, buy the regulated plumbing and integrate both around a stable system of record. The winners on both sides will be those that understand that AI has not eliminated healthcare software moats; it has redefined them.

How L.E.K. Consulting can help

L.E.K. helps HCIT companies, healthcare services providers and investors assess how AI changes product strategy, competitive advantage, build-versus-buy decisions and value creation. Our work spans AI opportunity assessment, product and platform strategy, commercial model redesign, healthcare data strategy, regulatory and interoperability roadmaps, and investor diligence.

For HCIT companies, this includes identifying AI-driven TAM expansion, mapping build-risk exposure by module and customer segment, designing AI-native platform strategies and developing a prioritised autonomy roadmap. For healthcare services providers, it includes determining which workflow and AI capabilities should be built, bought or partnered and how to do so without compromising compliance, safety or implementation speed.

To discuss how AI could reshape your healthcare technology strategy, platform roadmap or build-versus-buy decisions, contact us.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting