Beyond these clinical gaps sits an equally consequential commercial requirement: providing patients with frictionless access to the medicines they need. That will require channel strategies that leverage telehealth and direct-to-consumer (DTC) platforms, enabling patients to start therapy more easily, stay on treatment longer, and choose the payment pathway that best fits their needs. Winners will also need to secure market access with insurers, increasingly through portfolio-level contracting leverage that can drive preferred placement. Strategic inclusion of obesity-related comorbidities into product labels may further reduce access friction, as coverage tied to cardiometabolic and other obesity-related risks may prove more durable than coverage for weight loss alone. The expected availability of generic semaglutide in the early 2030s will only intensify these pressures.

So what — implications for market participants

For incumbents:

The magnitude-of-weight-loss arms race may be nearing its end as the primary battleground for the injectable class. Differentiation will increasingly depend on treatment protocols that support persistence, options for treatment-experienced patients, and the ability to build frictionless access from initiation to ongoing therapy. Oral Wegovy’s DTC launch and LillyDirect’s telehealth-integrated dispensing model signal that channel strategy is becoming a core competitive asset, enabling patients to start therapy more easily and choose between insurance-based and self-pay pathways. Market access will also be central: portfolio-level contracting may be needed to secure preferred placement, while obesity-related comorbidities can help reduce coverage friction where weight-loss-only indications face resistance. As generic semaglutide approaches in the early 2030s, incumbents with the strongest combination of clinical lifecycle management, contracting leverage and omnichannel reach will be structurally advantaged.

For challengers and emerging biopharmas:

Winning with a single undifferentiated obesity asset will become increasingly difficult. Emerging companies should focus on a clearly defined unmet need, with precise positioning and a clear source-of-business thesis that makes the asset strategically relevant to partners or acquirers. Larger challengers will need to start with a differentiated beachhead asset and build from there, adding the evidence base, access capabilities, channel infrastructure and portfolio breadth required to compete at scale. As the basis of competition expands beyond efficacy to include market access, channel presence and lifecycle management, entrants must be prepared to make the substantial commercial investment required to challenge entrenched incumbents.

For financial sponsors and acquirers:

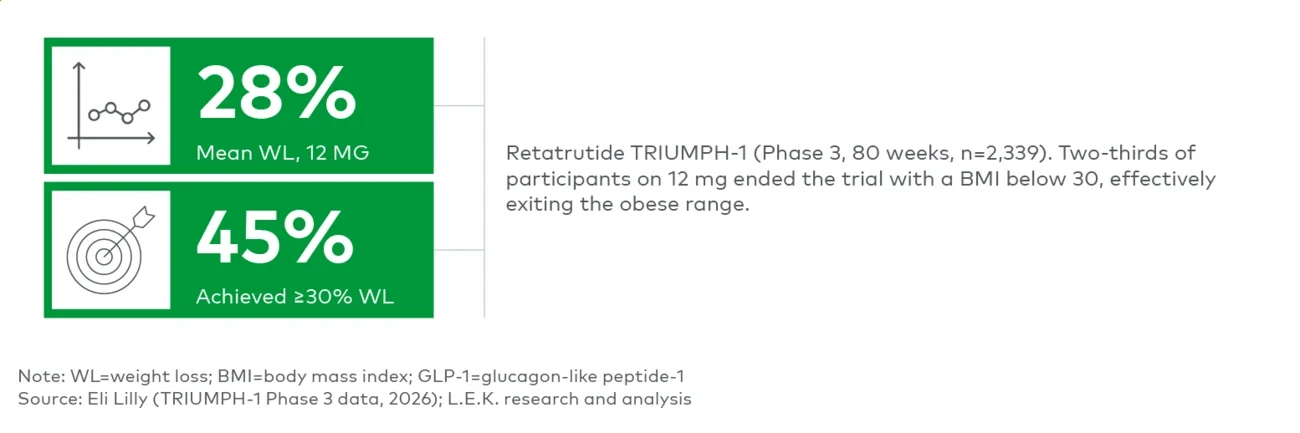

Valuation frameworks built around peak weight loss magnitude require recalibration. With the efficacy ceiling now set at 28%, durable value creation will depend less on incremental weight loss and more on the ability to address persistent clinical unmet needs (tolerability, convenience, personalization, maintenance, refractory obesity and weight-loss quality) in ways that translate into real-world adherence, payer relevance and chronic care scalability. Assets with demonstrated tolerability advantages, validated oral formulations, credible maintenance strategies or mechanistic rationale in refractory settings may merit premium scrutiny. Platform companies in telehealth, digital therapeutics and patient support that can serve as the access layer for AOM therapy at scale also warrant attention. Single-asset obesity stories without a clear clinical differentiation thesis and channel strategy will face increasing headwinds.

For payers and health systems:

The clinical case for coverage of AOMs is now increasingly difficult to dispute from an efficacy standpoint. Going forward, the policy debate will center on access, adherence infrastructure and cost-effectiveness in the maintenance phase, not on whether the drugs work. Managed care organizations that develop population management frameworks for obesity now will be better positioned than those that treat it as a one-line formulary decision.

For further insights, see our recent piece exploring how AOMs are changing DTC pharmaceutical platforms.

Contact us for more information.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC