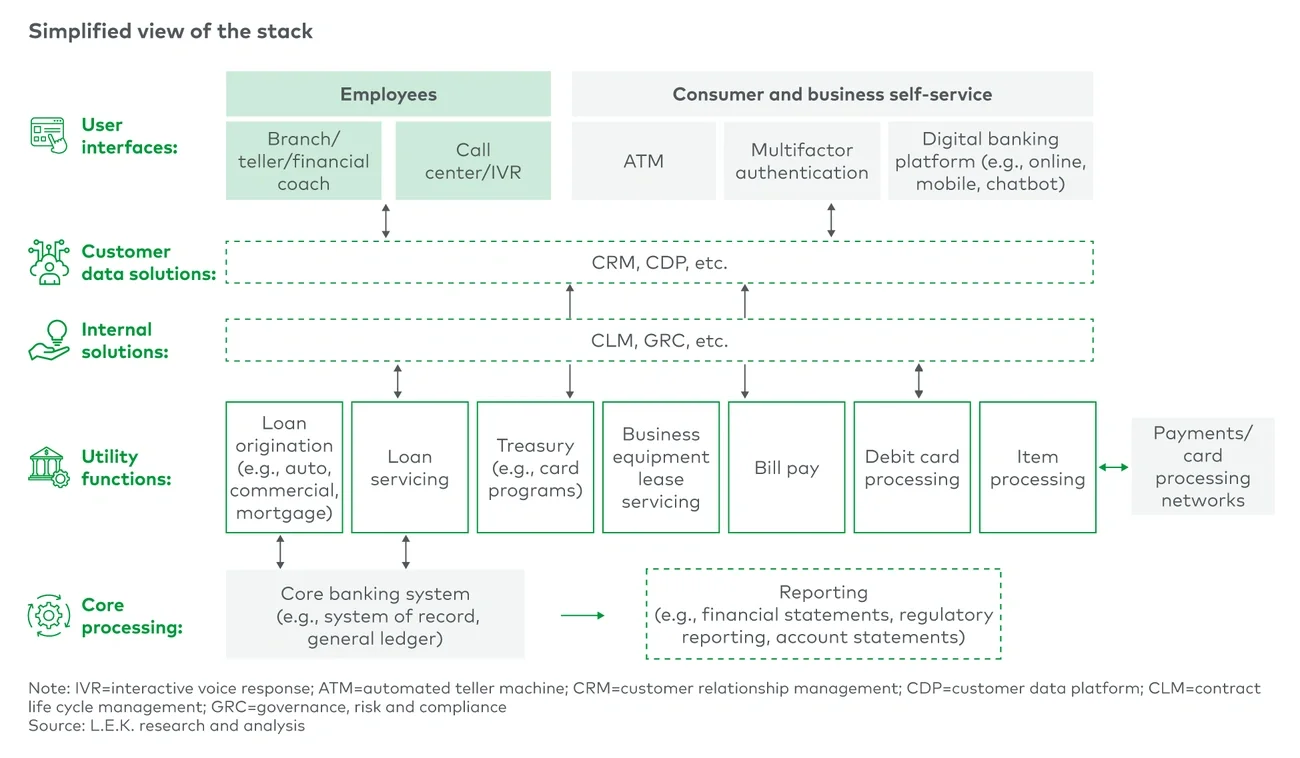

Three areas of the technology stack are drawing particular attention:

- Digital banking platforms: Credit union membership has grown steadily, and members increasingly expect the kind of digital experience larger banks have long offered, driving continued investment in digital banking solutions across the sector.

- Internal and utility solutions: Risk management, loan servicing and loan origination platforms have matured significantly, giving institutions better risk controls and the ability to lend more efficiently.

- Core processing platforms: Many institutions are beginning to evaluate the transition from legacy on-premises environments to cloud-native core platforms, a shift that remains in the early stages but is expected to accelerate significantly over the next decade.

Core modernization decisions are among the most technically and operationally demanding undertakings a bank or credit union can pursue, with industry participants projecting hundreds of conversions by 2035.

These are not initiatives that most internal teams encounter with enough regularity to develop genuine proficiency, and the contract-specific knowledge required to negotiate them well is difficult to build without continuous exposure across many engagements.

The scale of contracted IT spend raises the stakes

Global enterprise IT spending in the banking sector is forecast to exceed $1.1 trillion² by 2029, and a significant portion of that spend is committed through long-term vendor contracts. For a midsize bank or credit union, a single core banking contract alone may represent tens of millions of dollars over a five-to-10-year term, with payments processing and digital banking agreements adding considerably to that total.

The pricing structures in these agreements are complex, typically tiered by volume, adjusted for scope changes and layered with provisions governing upgrades, integrations, termination fees and renewals. What looks favorable at signing often erodes over time as volumes grow, features expand and scope creep accumulates. Unfavorable termination provisions can lock institutions into vendor relationships long after better alternatives have entered the market, and the cumulative cost of underperforming contracts across core, payments and digital banking systems can meaningfully compress operating margins and reduce capital available for lending.

Regulatory escalation is raising the cost of getting it wrong

The 75-plus systems that make up the average bank or credit union technology stack do not operate in isolation. A poorly selected or underperforming vendor can slow adjacent systems, introduce data quality problems and degrade solutions that would otherwise work well. The stakes of any single vendor decision extend well beyond that contract.

Regulatory expectations compound that risk further. Standards around cybersecurity, operational resilience, payments governance and third-party risk management have expanded steadily, with requirements that once applied primarily to the largest institutions now extending across the asset tier spectrum. Both the Office of the Comptroller of the Currency’s 2025 supervisory priorities and the National Credit Union Association’s 2026 supervisory priorities direct examiners to assess vendor risk management across the full life cycle of critical third-party relationships, from due diligence through termination.

For midsize institutions that typically rely on generalist staff to cover these functions, meeting that bar requires a level of process, documentation and vendor oversight infrastructure that few have historically needed to maintain.

Bank and credit union consolidation is compounding complexity

Smaller community banks and credit unions have been merging steadily for decades in pursuit of scale, improved financial health and the operational capacity to invest in competitive technology. The number of midsize regional institutions ($1 billion to $10 billion in assets) is projected to grow from approximately 1,330 to 1,615 between 2024 and 2029³ as smaller institutions consolidate upward into that tier. As a result, a growing cohort of institutions is navigating a level of organizational and technological complexity that their internal teams were not originally built to manage.

Postmerger integration typically requires vendor rationalization, contract resets, core conversions and system consolidation across multiple legacy technology stacks. The probability of navigating at least one of these events during a leadership team’s tenure is growing, and few institutions are well positioned to manage them internally, particularly on the compressed timelines of M&A activity.

Institutions crossing the $1 billion and $10 billion asset thresholds also face a step-change in regulatory expectations around third-party risk management, governance and operational resilience, adding another layer of complexity to an already demanding transition.

For a deeper look at how consolidation is reshaping the midsize banking landscape, see our analyses From Survival to Success: Scaling Strategies for Midsize Banks and Credit Unions’ Strategic Evolution: Navigating Growth Through M&A and Beyond.

From episodic engagement to default behavior

Taken together, these forces have driven a meaningful shift in how banks and credit unions approach major operational and technology decisions, moving from occasional reliance on outside help toward external advisory support as a standard part of how institutions manage complexity, vendor relationships and regulatory obligations.

The commercial model has supported this move toward more continuous advisory engagement. Success-fee arrangements tie adviser compensation to realized savings or favorable contract outcomes, allowing institutions to access specialty-area expertise without significant up-front commitment. For cost-constrained midsize institutions, this structure has meaningfully lowered the barrier to engaging such advisory support.

The market for vendor evaluation and advisory services for U.S. banks and credit unions remains underpenetrated. Much of the unserved opportunity is concentrated among institutions with $500 million to $10 billion in assets, where vendor complexity is significant but internal capacity to manage it is most constrained.

As this reliance becomes more structural, the question shifts from why banks and credit unions are turning to advisory firms to which firms are best positioned to serve them.

L.E.K. Consulting’s Financial Services practice advises investors and financial institutions on growth, competitive positioning and consolidation opportunities across banking advisory services. To discuss how these dynamics inform your investment process, contact us.

Endnotes

¹S&P Capital IQ, via L.E.K. research and analysis.

²Gartner, “Forecast: Enterprise IT Spending for the Banking and Investment Services Market Worldwide, 2023-2029, 2Q25 Update.” Chris Regan, Debbie Buckland, Inna Agamirzian. Aug. 6, 2025. https://www.gartner.com/en/documents/6812534

³S&P Global Market Intelligence, via L.E.K. research and analysis.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC