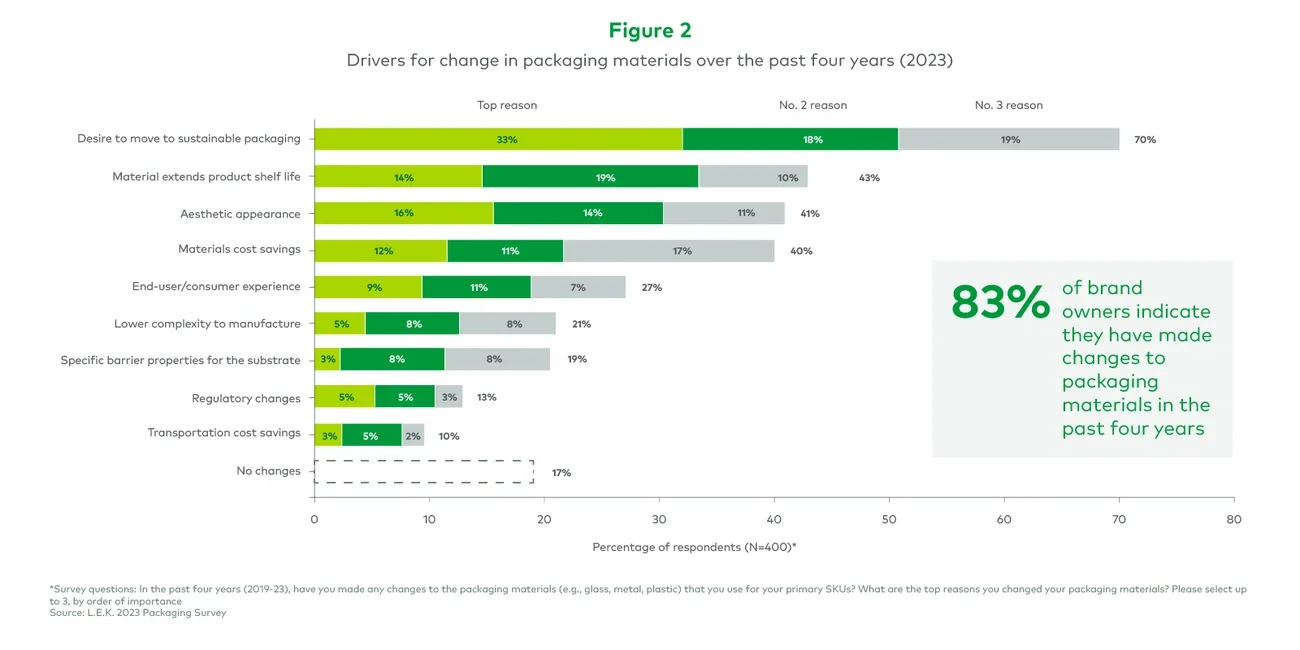

Brand owners, more than ever before, believe that packaging is imperative to selling their products and are willing to invest in their packaging as it represents just a small percentage of the value of the products they sell. In addition to their optimistic outlook for packaging and continued emphasis on the importance of packaging to a brand’s success, they’re increasingly focused on the sustainability of their packaging. They’re also still more than willing to change packaging materials to optimize the balance of cost-to-value and will likely continue to do so over the medium term as they believe they’re exhausting their ability to pass through incremental packaging cost increases to consumers, for whom prices have remained high despite the rate of inflation edging lower.

In the meantime, across end markets, brand owners largely expect finished goods inventory levels to normalize over the next year, back to pre-COVID-19 levels, as consumers trade back up to branded products and supply chain issues subside, which would bring an end to the “stocking” pressure felt by converters during 2023.

That’s according to L.E.K. Consulting’s sixth annual proprietary packaging study, which it conducted in the fourth quarter of 2023 and which makes clear how players up and down the packaging value chain can differentiate their offerings in order to best meet the needs of brand owners and, by extension, their investors and lenders.

About the study

L.E.K. surveyed 400 U.S. brand managers and packaging stakeholders across a variety of brand end and sub-markets, types, and sizes to understand their packaging needs and get their views on the trends driving demand.

Similar to prior years, the 2023 study looks at the impact of stock-keeping unit (SKU) dynamics on packaging, changes to packaging materials, the implementation of sustainable packaging initiatives, the implications of ecommerce on packaging, and how the macroeconomic environment has impacted companies’ packaging sourcing strategies and associated costs.

In addition to highlighting how brand owners’ views on these topics have shifted over the past few years, this year’s study also makes clear how inventory management has evolved across various end markets, how new SKU introductions/SKU rationalization programs are tied to product innovation and financial performance, and how brand owners view the adoption of digital tools by their packaging suppliers.

The study targeted brand managers and other packaging decision-makers at consumer packaged goods companies who were responsible (or directly involved in making decisions) for

- a consumer brand that is sold at least in the U.S. but may also be sold into international markets

- a brand within the food, beverage, beauty and personal care, household and healthcare, and/or consumer electronics end markets

The big issues in 2023

For this year’s study, we sought to dive deeper into the most pressing issues on the minds of brand owners with a range of questions:

- Packaging trends and associated spend – How important is packaging to a brand’s success, and how does relative spend on packaging vary by end market and customer segment? What level of packaging cost increases have brand owners passed on to consumers? What changes have brands made to their packaging, and what changes do they expect to implement over the next four years? What has been driving changes in packaging materials used over the past several years, and what changes do they expect to implement over the next several years?

- Megatrends’ impact on packaging – How do brand owners define sustainable packaging, what percentage of brand owners have a 2025 (or medium-term) sustainability goal and what level of progress has been made toward that goal? How do brand owners expect their sustainable material usage to trend over the next several years, and what primary actions do they expect to take? What percentage of brand owners use ecommerce-specific packaging formats, which features are they introducing and why?

- Impact of brand performance and SKU dynamics on packaging – What are the key drivers for any changes in the number of new SKU introductions? What aspects of product innovation, if any, are driving the introduction of new SKUs? How have SKU rationalization programs impacted the financial performance of brands?

- Brand owner packaging sourcing strategies – How has inventory carried by brand owners evolved over the past four years? When do brand owners expect a return to pre-COVID-19 stock levels of on-hand finished goods? What are brands’ geographic sourcing strategies?

Packaging trends and associated spend

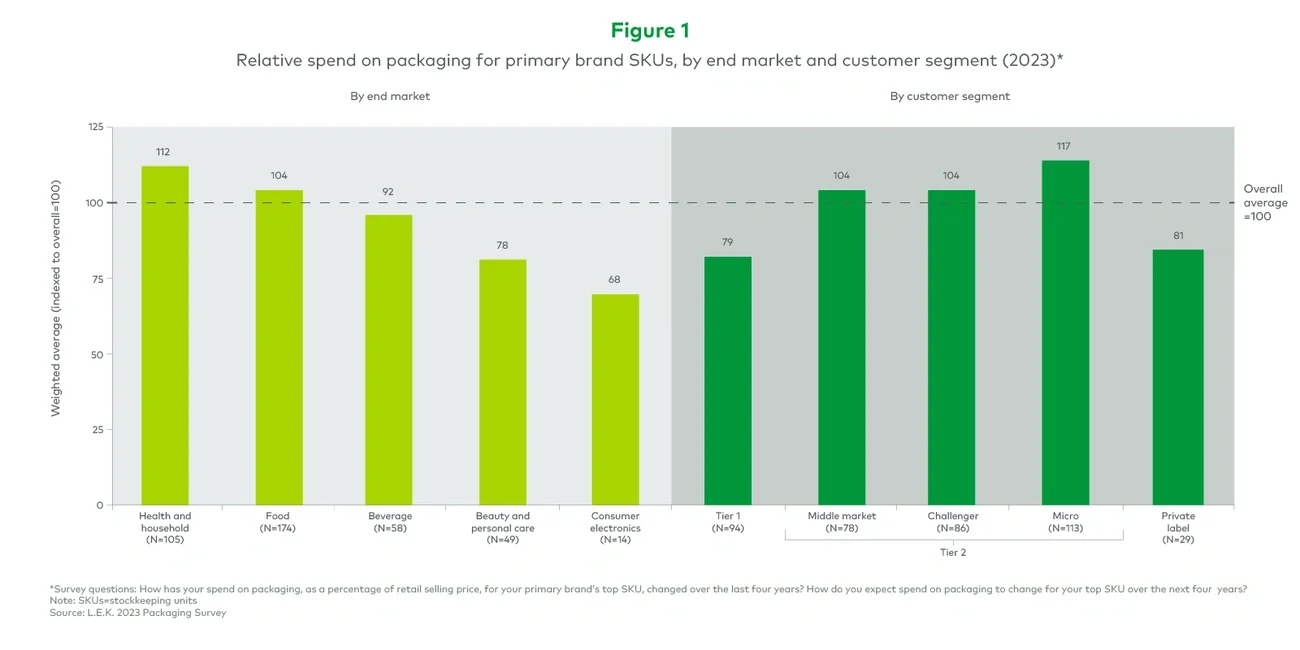

Similar to prior years’ findings, packaging is viewed as critical to the success of a brand; even in the face of challenging macroeconomic conditions, the percentage of brand owners who agree with that sentiment rose to 98% from 84% in 2022. Middle market ($750 million-$2.49 billion in annual revenue) and micro (less than $250 million in annual revenue) brands in particular emphasize the importance of packaging.

The reported importance of packaging on brand success, meanwhile, is relatively similar across end markets, with beauty and personal care brand owners indicating slightly higher importance relative to the others. Packaging spend as a percentage of retail selling price is highest for health and household products and lowest for consumer electronics. And Tier 1 ($2.5 billion or more in annual revenue) brands tend to spend less on packaging (as a percentage of the retail selling price) than do their smaller peers (see Figure 1).