Brand owners, who since 2019 have been increasing their inventory levels in a bid to decrease risk, largely expect their inventory levels to return to pre-COVID-19 levels in 2024 as demand growth recalibrates and supply chain issues subside. And by 2027, after steadily increasing the share of packaging sourced from the U.S. over the past few years, they expect that share to hit 85%, driven by a desire for suppliers that can serve short-run needs at compelling lead times.

That’s according to L.E.K. Consulting’s sixth annual proprietary packaging study that we conducted in the fourth quarter of 2023, which makes clear how players in the packaging value chain can differentiate their offerings in order to best meet the needs of brand owners and, by extension, their investors.

Brand owner packaging sourcing strategies

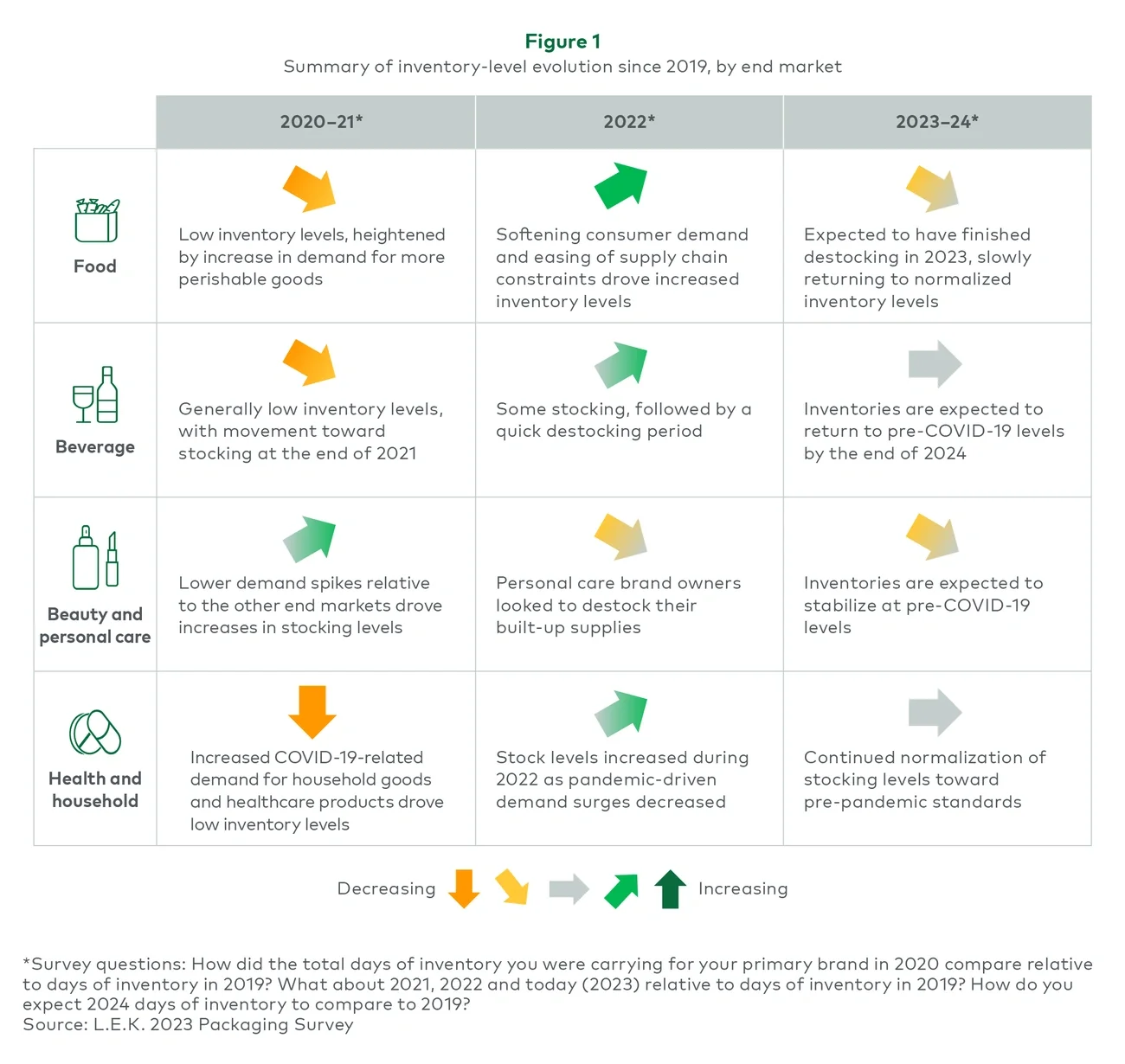

After low inventory levels in 2020-21 and mixed stocking/destocking trends in 2022, brand owners largely expect inventory levels to normalize across end markets — namely food, beverage, beauty and personal care, and health and household — by the end of 2024 (see Figure 1).