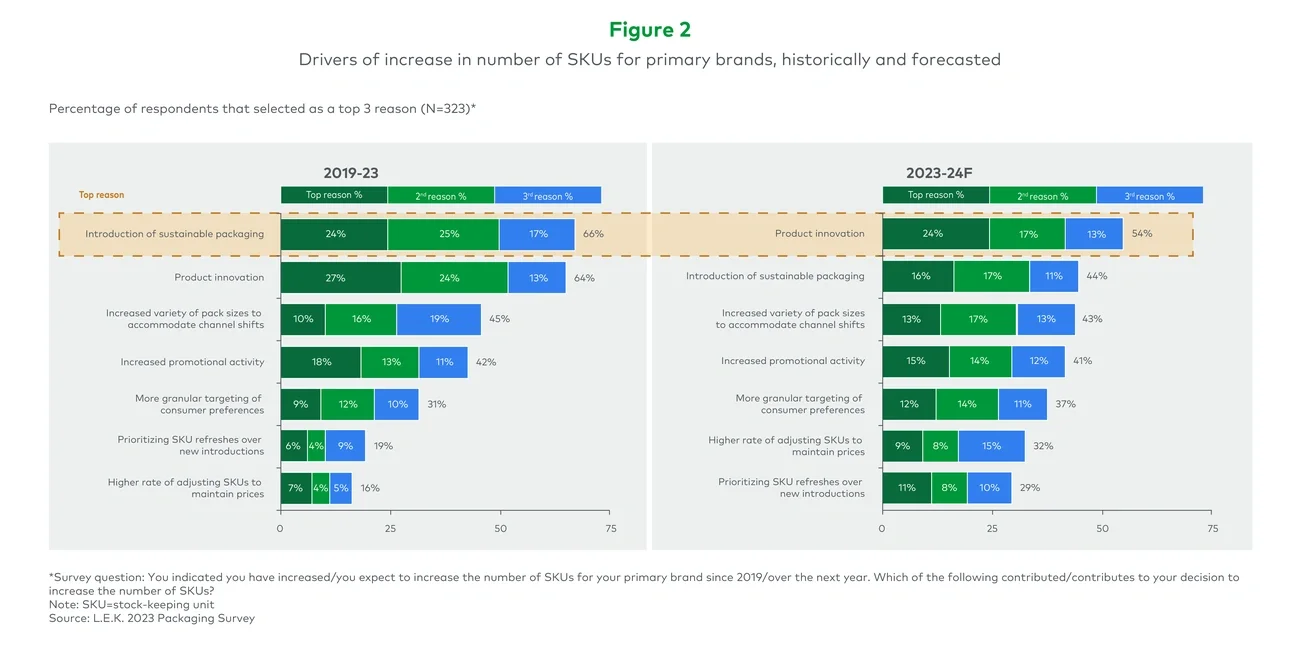

Many brand owners, who in a bid to increase margins and limit innovation costs had already begun reducing the number of stock-keeping units (SKUs) in their portfolios in 2019 shortly before COVID-19 hit, plan to continue with their SKU rationalization through at least 2024. However, some brand owners have continued to maintain a commitment to new product innovation and say they’ll continue to launch new branded product SKUs over the next year, citing product innovation and the introduction of sustainable packaging.

That’s according to L.E.K. Consulting’s sixth annual proprietary packaging study, which we conducted in the fourth quarter of 2023 and which makes clear how players in the packaging value chain can differentiate their offerings in order to best meet the needs of brand owners and, by extension, their investors.

Impact of brand performance and SKU dynamics on packaging

Whereas historically, brand owners emphasized broadening the range of SKUs they offered in order to attract new customers or react to new consumer behavior and trends, most — including some of the largest and most recognizable consumer brands, such as Unilever, Coca-Cola and Tyson, among others — have shifted their SKU portfolio strategies in recent years to focus on their most profitable products in order to boost margins and cap innovation costs. Indeed, COVID-19 and the supply chain disruptions it created only accelerated those brands’ SKU rationalization strategies as they focused on long-run “core” SKUs to meet market demand.

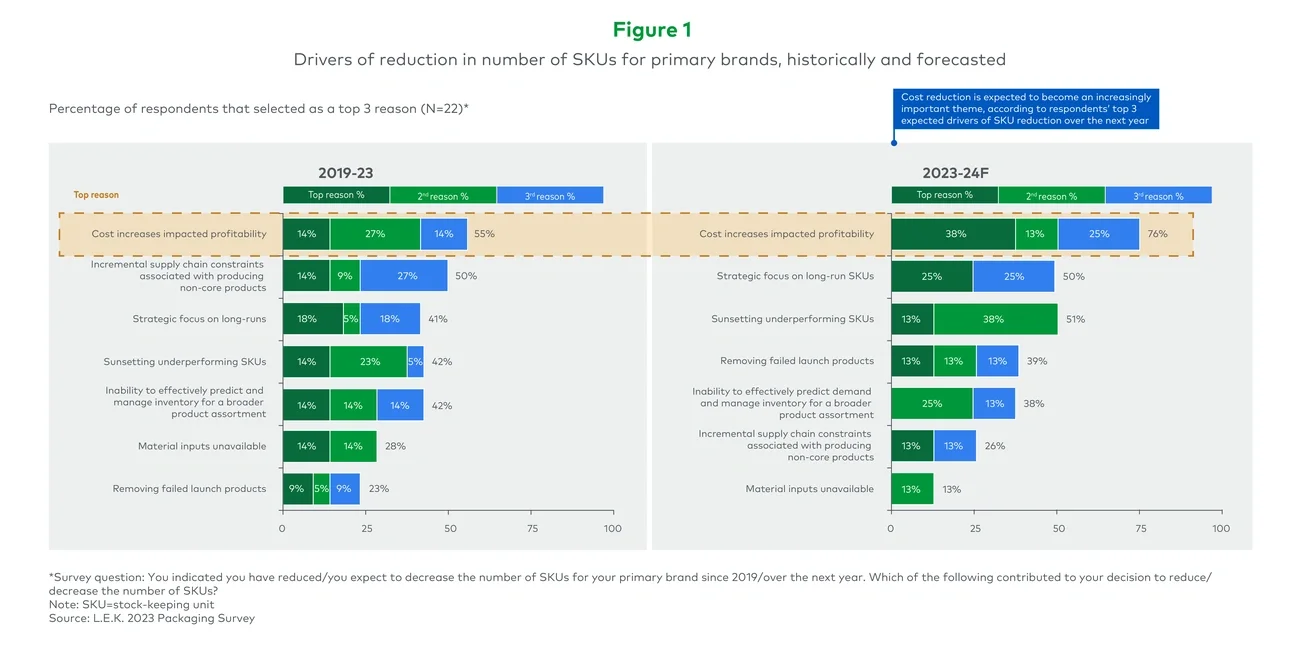

Going forward, cost mitigation associated with new SKUs and a strategic focus on core SKUs are expected to become increasingly important themes. In fact, heading into 2024, even more brand owners say minimizing the impact of cost increases on profitability is the top reason they will reduce their number of SKUs (see Figure 1).