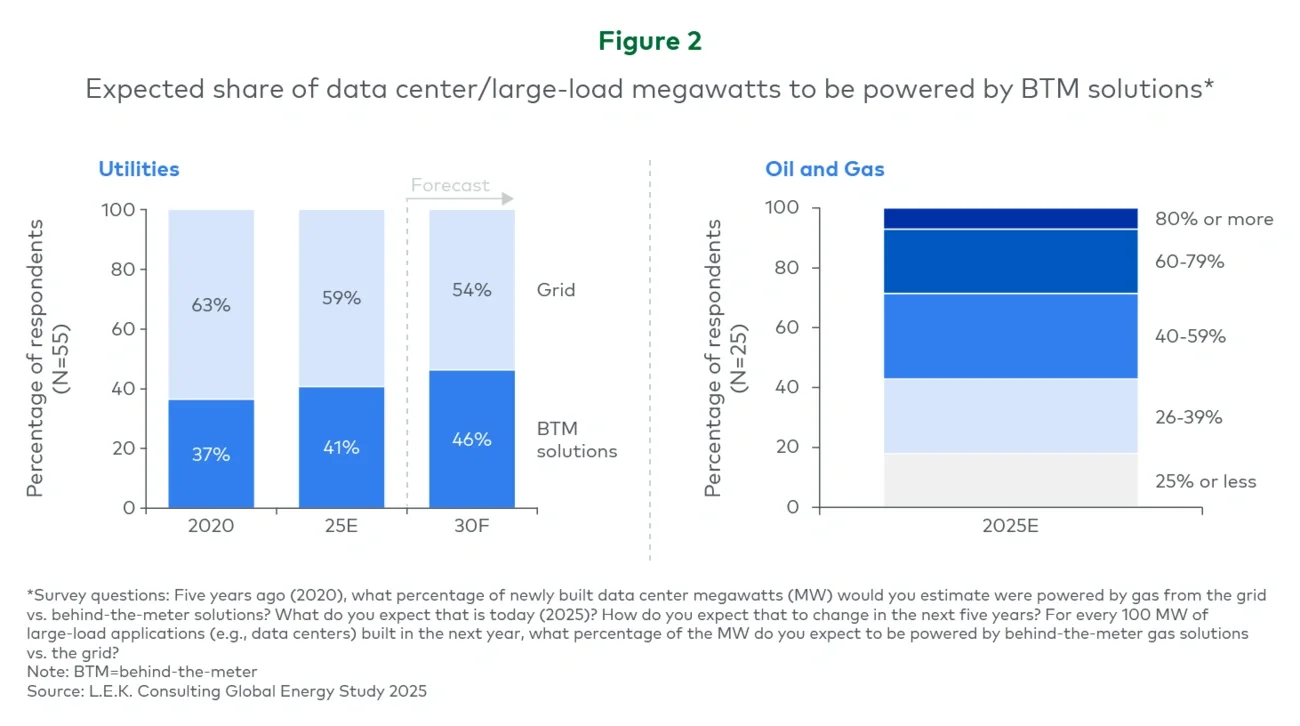

This creates a two-speed system: Grid upgrades take years; data centers scale in months. BTM generation provides a bridge for operators, but companies consider it a short-term workaround of less than two years rather than a structural solution. The long-term answer remains the same across the board: grid capacity, reinforced and modernized to handle both daily load and future growth.

A new reliability equation for renewables and gas

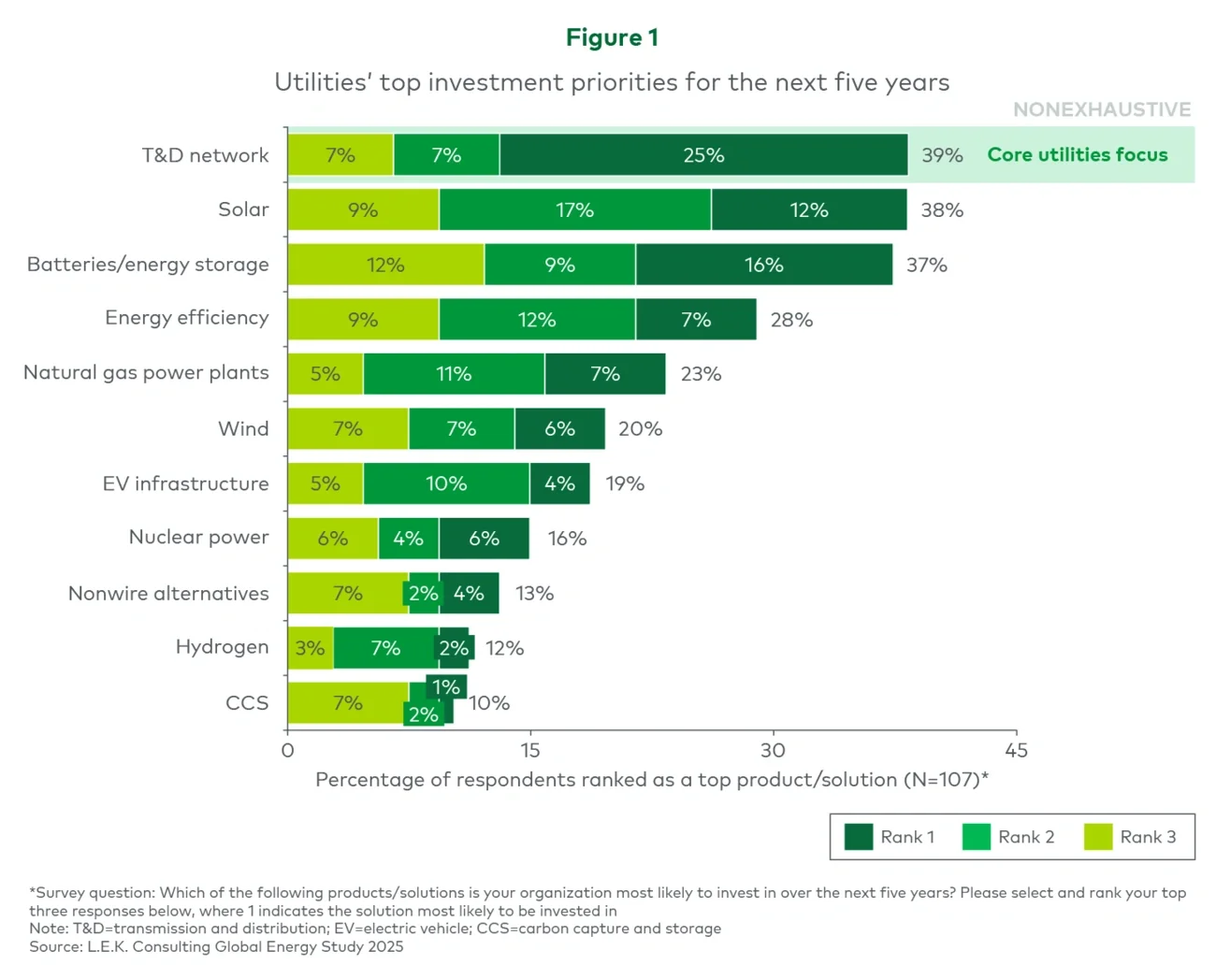

The growing share of renewables has brought valuable generation diversity, but it has also raised concerns about firm capacity. Our survey reveals that 59% of utilities believe renewable intermittency poses a risk to power reliability. In response, storage integration is becoming central to resilience planning. Battery systems are ranked in the top tier of five-year investment priorities, reflecting a shift from seeing storage as a supplementary asset to recognizing it as integral to network stability.

Utilities are also turning to flexible gas capacity to stabilize the system. When asked about expected baseload generation composition, respondents forecast natural gas to remain the largest share through 2030. However, only 22% are confident that new gas plants can meet near-term demand. This reflects a practical need for dispatchable power during a period of intense load growth and infrastructure strain. In a recent discussion, a leading U.S. investor-owned utility cited a major “shift of the center of gravity from what has been solar to natural gas-focused generation priorities.”

Regional dynamics: Different pressures, similar priorities

The pressures on grids vary by region, even as investment priorities converge.

The U.S. faces the steepest load increases, propelled by AI-driven data centers and industrial reshoring. Companies such as Duke Energy, Dominion Energy and Southern Co. have increased capital plans to expand and reinforce transmission and distribution networks, citing the need to connect large new loads while strengthening resilience against extreme weather.

European utilities face a different set of challenges. Demand growth is more moderate, but high renewable penetration and increasingly interconnected markets place a sustained strain on networks. Companies such as E.ON are directing the majority of capital toward network expansion and digitalisation to manage congestion, integrate renewables and maintain system stability.

Across regions, the objective is consistent. Whether driven by load growth or system complexity, utilities are investing to modernise networks, improve resilience and unlock additional capacity, reinforcing the grid’s role as a critical enabler of reliable power systems.

From bottleneck to enabler

Grid modernization is now the foundation of the energy transition. Investment logic has shifted from supply-side expansion to system-level resilience. Utilities are directing capital to the assets and technologies that guarantee reliability, create capacity for large-load customers and integrate renewables without compromising stability.

The pace of the transition will be determined by the strength and readiness of the networks that support it — and utilities are acting to ensure those networks are ready.

This article is part of our Powering Forward series:

How L.E.K. can help

Our teams advise energy leaders on where to invest, how to build resilient infrastructure and when to accelerate transition bets. Our 2025 Global Energy Study provides the data and insight; our consulting expertise helps clients translate these findings into decisions that create value today and secure a position for tomorrow.

For more details on the full study or to learn how these insights apply to your business, please contact our global energy team.

L.E.K. Consulting is a registered trademark of L.E.K. Consulting LLC. All other products and brands mentioned in this document are properties of their respective owners. © 2026 L.E.K. Consulting LLC