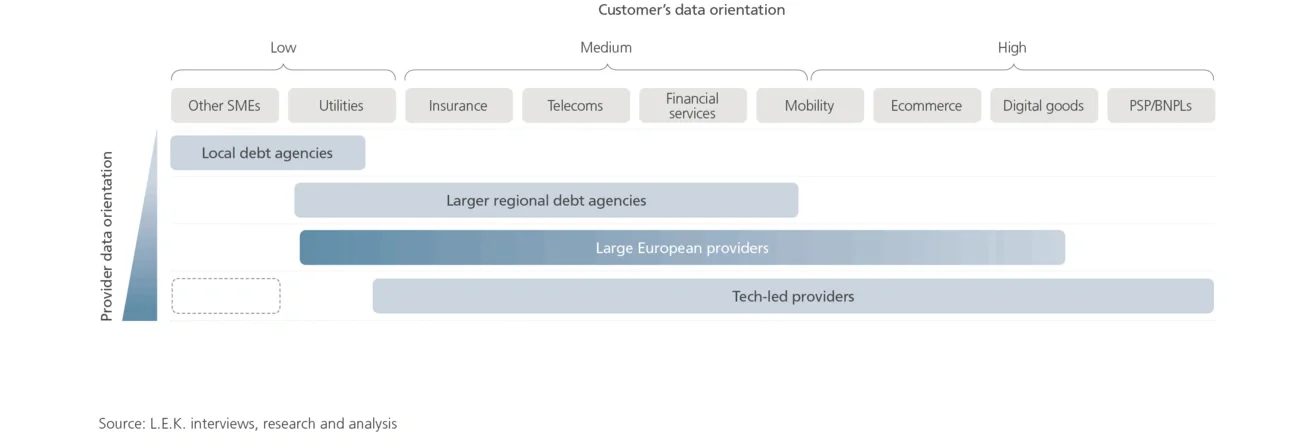

Outsourcing the collection of defaulted unsecured consumer debt from lending, insurance, utilities and telecoms is a well-established industry in Europe. In value terms, individual claims are typically for more than €500, and the debt agencies generate good rates of return based on collections models that have substantial manual components and include litigation, when appropriate.

But the industry is on the cusp of disruption. New tech-based collections firms have emerged in Europe in the last few years and built increasingly attractive, viable businesses off the back of the internet-based products and digital services explosion, e.g. streaming services. They have thrived because the individual consumer debts are too small (often less than €100) for the incumbent agencies’ collection methods to be economically viable. Following these successes, these new players are now turning their attention to how they can leverage their leading-edge tech capabilities to start taking market share in the incumbents’ core territory in more traditional industries. Early success in this area indicates that this disruption is no longer just a theoretical possibility.

It is now urgent for incumbents to develop a strategic response to these new, fast-moving competitors. Private equity firms and other investors, both those with debt management sector investment expertise and those focused on backing innovative tech-based companies, should be actively reviewing the market for opportunities as the new companies expand their services and geographic operations, upending the traditional industry.

L.E.K. Consulting has been advising the European debt management industry for nearly two decades. This Executive Insights sets out an overview of the current market and key considerations for the incumbent debt management firms and industry investors to think about as they appraise their strategies in response to the rise of the challenger brands.